Product Description

In 2021, the global gynecological device market size is projected to reach $2.1 billion, with mechanical uterine tissue removal devices showing the fastest growth in demand. In spite of COVID19, the global market size is expected to increase over the forecast period and exceed $3.3 billion in 2027. Currently, the majority of the global market share is controlled by three main companies – Hologic, Cooper Surgical, and Boston Scientific.

One major trend in the global market for gynecological devices is the shift towards mechanical uterine tissue removal procedures and away from alternative and more dangerous treatments. The purpose of mechanical uterine tissue removal devices is to remove uterine growths or the uterine tissue, while protecting the uterus’ integrity to prevent consequent issues, such as infertility. The use of a wand instead of a blade avoids dangerous cuts to the uterine lining/tissue.

Concerns over the safety of pelvic organ prolapse devices are expected to hinder market growth over the forecast period. In Europe, transvaginal meshes are recommended to be used only in complex cases where there are no other alternative treatments. The lawsuits, regulatory scrutiny, and general poor publicity regarding the usage of meshes are likely to limit growth in the pelvic organ prolapse repair market and the overall market.

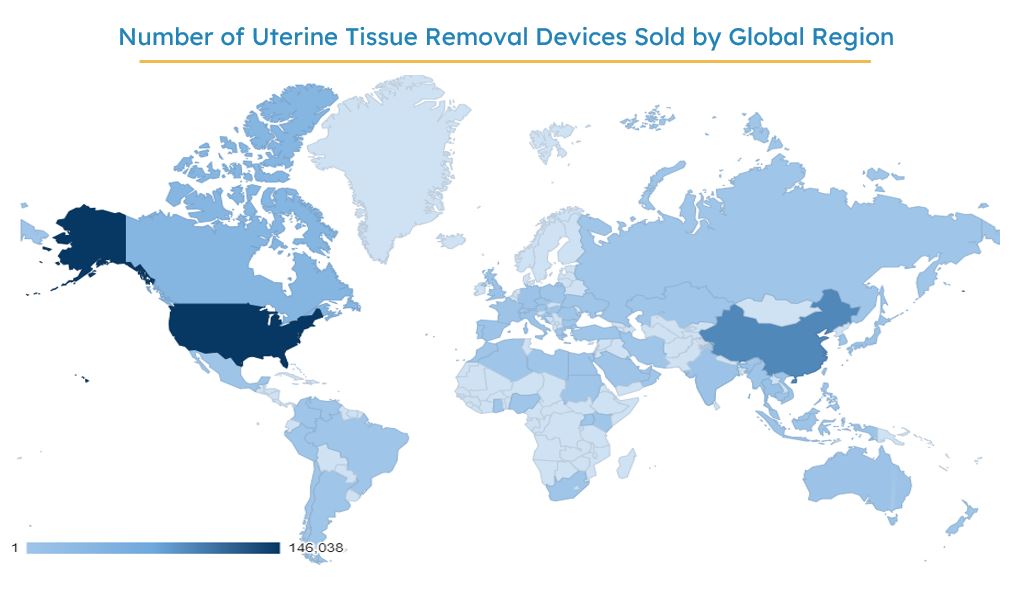

How Many Uterine Tissue Removal Devices are Sold Globally?

Globally, there are over 320,000 uterine tissue removal devices are sold every year, with the United States and China having the highest product demand. Over the next 6 years, the number of these devices sold will grow exponentially, reaching over 1 million devices sold in 2027. The popularity of mechanical uterine tissue removal devices is projected to continue growing due to the procedural time efficiency they provide. Thus, this market study analyzes how these devices are disrupting the global market, including the impact on the gynecological resection device market segment.

Over the next 6 years, the number of these devices sold will grow exponentially, reaching over 1 million devices sold in 2027. The popularity of mechanical uterine tissue removal devices is projected to continue growing due to the procedural time efficiency they provide. Thus, this market study analyzes how these devices are disrupting the global market, including the impact on the gynecological resection device market segment.

How’s COVID19 Impacting The Gynecological Device Market?

In 2020, the global market for gynecological devices declined by over 30% when compared to 2019 as a result of the COVID-19 pandemic. However, the global market is expected to recover rapidly and reach the pre-COVID levels by the end of 2021.

The gynecology market was severely impacted by COVID-19, as the majority of gynecological procedures are considered elective. For example, in the assisted reproductive technology (ART) market, the majority of countries stopped treatments with the exception of fertility preservation for oncology patients. Most countries restarted treatments following the easing of lockdown restrictions. Restarting ART treatments was seen as a priority in most countries due to the time-sensitive nature of infertility and the long-term impact this could have on population growth.

What Are the Top Gynecology Companies?

Over 40% of the global gynecological device market share is controlled by three main companies – Hologic, Cooper Surgical, and Boston Scientific.

Hologic is the clear leader of the total gynecological device market across the globe. The company has an extensive product portfolio, which secures its leading positions in the global endometrial ablation, mechanical uterine tissue removal device, hysteroscope, and fluid management device market segments. Its success within the global endometrial ablation market was largely derived from its radiofrequency ablation device, NovaSure™.

Cooper Surgical is the second-leading competitor in the global gynecology market, due to a diverse line of products involved in multiple markets, including endometrial ablation, colposcopes, and HSG catheters. Additionally, Cooper Surgical leads the highly profitable assisted reproduction technology market. In 2016, the company gained substantial shares in the oocyte retrieval needle and embryo transfer catheter market segments, due to its acquisition of Wallace Medical from Smiths Medical that year.

Boston Scientific is the third-leading competitor in the global gynecological device market. The company holds strong positions across a variety of global markets, including endometrial ablation, endometrial resection device, mechanical uterine tissue removal, uterine fibroid embolization, fluid management device, and pelvic organ prolapse repair device markets.

Top Global Gynecology Companies Analyzed |

||||

|---|---|---|---|---|

|

|

|||

Market Segmentation Summary

While this global report suite contains all global gynecological device market data, each of the market segments is also available as a stand-alone report, MedCore. This allows you to get access to only the gynecological device market research that you need.

- Assisted Reproduction Technology Device Market | Global | 2021-2027 | MedCore – The market analysis is further broken down into segments by:

- Device Type: Oocyte Retrieval Needles, Micropipette, Embryo Transfer Catheters, and Reproduction Media.

- Endometrial Ablation Market | Global | 2021-2027 | MedCore – The chapter contains the market analysis which is categorized by:

- Device Type: Thermal Ablation and Radiofrequency Ablation Devices.

- Gynecological Resection Device Market | Global | 2021-2027 | MedCore – The market is analyzed by:

- Device Type: Resectoscopes, Monopolar Loop Electrodes, and Bipolar Loop Electrodes.

- Mechanical Uterine Tissue Removal (UTR) Device Market | Global | 2021-2027 | MedCore – The research includes an in-depth analysis of the global mechanical UTR market;

- Uterine Fibroid Embolization Device Market | Global | 2021-2027 | MedCore – The market analysis is further broken down by:

- Device Type: Microspheres, and PVA Particles.

- Hysteroscope Market | Global | 2021-2027 | MedCore – The market analysis is further segmented by:

- Device Type: Flexible and Rigid Hysteroscopes.

- Colposcope Market | Global | 2021-2027 | MedCore – The research includes an in-depth analysis of the global colposcope market;

- Pelvic Organ Prolapse Repair Device Market | Global | 2021-2027 | MedCore – The chapter contains the market analysis which is categorized by:

- Device Type: Transvaginal and Sacrocolpopexy Meshes.

- Fluid Management Device Market | Global | 2021-2027 | MedCore – The market analysis is further broken down into segments by:

- Device Type: Fluid Management Capital Equipment and Tubing

- HSG Catheter Market | Global | 2021-2027 | MedCore – The research includes an in-depth analysis of the global HSG catheter market.

Global Research Scope Summary

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Brazil, Chile, Colombia, Mexico, Peru, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, U.K.) Central & Eastern Europe (Baltic States, Bulgaria, Croatia, Czech Republic, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Malaysia, Myanmar, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, Vietnam) Africa (Algeria, Egypt, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2020 |

| Forecast | 2021-2027 |

| Historical Data | 2017-2020 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | COVID19 Impact, Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.