Spine Companies such as Medtronic, DePuy Synthes, and Stryker are leading the global spine and VCF market in 2026 as new technologies and minimally invasive approaches reshape growth.

The global spinal implant and vertebral compression fracture (VCF) market is one of the most dynamic areas in healthcare. With new technologies, mergers, and clinical adoption patterns reshaping the space, both hospitals and device manufacturers are making big moves.

In this blog, we will look at the biggest players, the fastest-growing segments, and why the trends in spine and VCF technology matter for the future of healthcare.

Find growth niches in minutes, not months.

Explore quick, actionable insights from the select markets.

Table of Contents

➜ Who are the biggest players in the global spine and VCF market?

➜ Which spine market segments are growing the fastest?

➜ Is minimally invasive surgery changing the spine and VCF market?

➜ How are robotics, AR, and AI shaping spinal surgery?

➜ Where are spinal procedures being performed today?

➜ Why does this matter for hospitals, manufacturers, and investors?

Key Takeaways

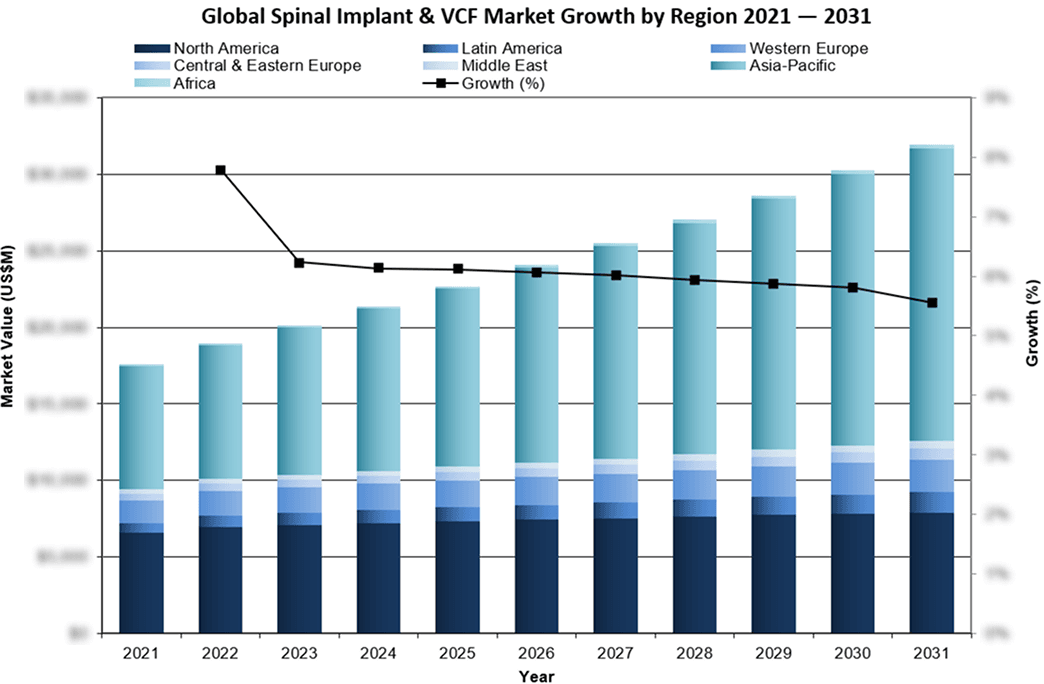

- The global spine and VCF market reached $21.4 billion in 2024 and is projected to grow to $32 billion in the next several years.

- Medtronic, DePuy Synthes, and Stryker lead the global market, with Medtronic dominating across most major spine segments.

- Thoracolumbar fixation, interbody devices, VCF, and surgical instrumentation are among the strongest growth drivers, supported by steady demand for fusion and fracture treatments.

- Minimally invasive surgery (MIS) is reshaping the market in developed regions, while robotics, augmented reality, and AI tools are improving surgical planning and precision.

- Procedure migration to outpatient settings such as ASCs, especially in North America, is changing purchasing behavior and driving demand for cost-effective, efficient implants and tools.

👉 Want to stay ahead in the Spinal Implants Market?

Unlock key insights with your Complimentary Executive Summary.

Who are the biggest players in the global spine and VCF market?

The biggest players in the global spine and VCF market in 2026 are Medtronic, DePuy Synthes, and Stryker.

Medtronic

![]()

In 2024, Medtronic held the leading position across most major segments, including cervical fixation, thoracolumbar fixation, interbody devices, and VCF treatments. Its leadership is built on a broad portfolio that covers both traditional fusion devices and motion preservation solutions. Medtronic also ranked fifth in the motion preservation segment, showing its reach across both established and emerging categories.

Depuy Synthes

![]()

DePuy Synthes, the second-largest competitor, held strong positions in interbody devices, cervical fixation, and thoracolumbar fixation, as well as a solid share in VCF solutions. Its product portfolio continues to support its growth globally, particularly in developed regions where MIS adoption is accelerating.

Stryker

![]()

Stryker ranked third overall in 2024, holding the second-leading position in the VCF segment while also maintaining meaningful shares in cervical fixation, thoracolumbar fixation, and interbody devices. The company has also been active in mergers and acquisitions, highlighted by its recent agreement to sell its spinal implant business to Viscogliosi Brothers in January 2025.

Which spine market segments are growing the fastest?

Thoracolumbar fixation is one of the largest and fastest-growing segments, expected to continue its mid-single-digit growth rate as spinal fusion procedures remain common across a wide range of pathologies.

Interbody devices also play a central role in market growth. Despite pressure from MIS and motion preservation techniques, interbody fusion procedures like TLIF (transforaminal lumbar interbody fusion), PLIF (posterior lumbar interbody fusion), and expandable devices remain in high demand.

The VCF market continues to expand thanks to increased awareness of osteoporotic fracture treatments and broader access to vertebroplasty and percutaneous vertebral augmentation (PVA). This segment is expected to grow at a mid-single-digit rate, reflecting the aging global population and rising incidence of osteoporosis-related fractures.

Finally, spinal instrumentation is emerging as one of the fastest-growing areas. Advances in robotics, navigation, and precision surgical tools are fueling demand. Hospitals and outpatient centers alike are investing in systems that improve accuracy and efficiency.

Is minimally invasive surgery changing the spine and VCF market?

Yes. Minimally invasive spinal (MISS) surgery is reshaping how procedures are performed and how products are used.

In developed regions like North America and Western Europe, MIS has quickly gained market share. Patients and providers see the value in faster recovery times, less blood loss, and shorter hospital stays. These benefits also translate to lower costs for hospitals and insurance providers.

In regions like Africa and the Middle East, MIS is still developing, but adoption is expected to accelerate as training and technology become more available. For manufacturers, this shift means designing implants and instruments that are optimized for MIS workflows. For healthcare providers, it means adapting to a future where patients increasingly expect less invasive solutions.

📌 Learn More About the Global Spinal Implants Market:

How are robotics, AR, and AI shaping spinal surgery?

Emerging technologies are transforming the way spine surgery is performed. Robotic-assisted surgery offers greater precision in implant placement, reducing complications and improving patient outcomes. Augmented reality (AR) navigation overlays digital guidance directly into the surgical field, while AI-enhanced planning tools help surgeons map procedures in advance.

Adoption of these tools is highest in the U.S. and advanced Asia-Pacific countries, where hospitals have the budget and infrastructure to support them. However, as costs decrease, more regions are expected to implement these platforms. For device makers, this means that product design increasingly needs to integrate seamlessly with digital technologies.

📌 Learn More About the Future of Spinal Implants:

Where are spinal procedures being performed today?

Traditionally, spinal surgeries have been concentrated in hospitals. However, a clear shift is happening. High-volume procedures like cervical interbody fusion and vertebral augmentation are moving into ambulatory surgery centers (ASCs), especially in North America.

This migration is changing purchasing behavior. Outpatient centers often prioritize cost-effective implants and efficient instrumentation that fit into shorter procedures and quicker recovery settings. Manufacturers that can tailor their offerings to meet the needs of ASCs will be better positioned for growth.

Turn market painpoints into opportunities

Explore how procedure trends and competitor positioning create clear openings for industry experts in the market.