Product Description

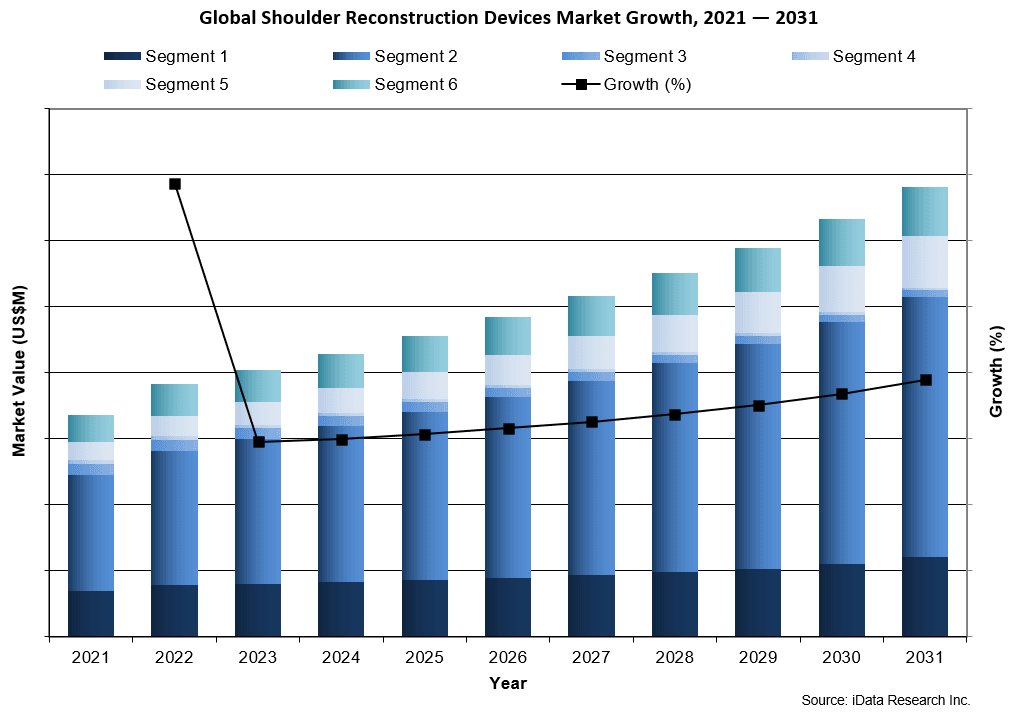

The global shoulder reconstruction device market was valued at over $2.1 billion in 2024. This is expected to increase over the forecast period at a CAGR of 6.8% to reach over $3.4 billion.

The full report suite on the global market for shoulder reconstruction devices includes total shoulder implants, reversed shoulder implants, hemi shoulder implants, resurfacing shoulder implants, revision shoulder implants and proximal humerus plates and screws.

MARKET DATA TYPES INCLUDED

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2024

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

GLOBAL SHOULDER RECONSTRUCTION DEVICE MARKET TRENDS

Surgeons are increasingly adopting stemless shoulder implants, especially for younger, more active patients. These designs preserve bone stock, simplify revision procedures and generally provide shorter recovery times with fewer intraoperative complications. This trend aligns with the global emphasis on preserving anatomical structures while delivering outcomes that are equal to or better than those of traditional stemmed systems.

GLOBAL SHOULDER RECONSTRUCTION DEVICE MARKET SHARE INSIGHTS

- Zimmer Biomet was the leading company in the shoulder reconstruction device market in 2024. Its leadership is driven by a comprehensive product offering that spans the full clinical spectrum, with strong solutions in both anatomic and reverse shoulder arthroplasty. The company’s portfolio, especially the Comprehensive® Shoulder System, demonstrates a long-standing commitment to modular designs that allow for intraoperative adaptability. Zimmer Biomet stands out for its sustained relevance in both primary and revision procedures. Its early entry into reverse shoulder systems and ongoing design improvements have helped maintain customer loyalty, despite the emergence of newer systems from competitors.

- Stryker held the second-leading position in the shoulder reconstruction device market in 2024. Stryker’s market position is a direct result of its focused innovation in the reverse shoulder segment. Rather than spreading across all sub-markets evenly, Stryker has doubled down on reverse arthroplasty, a strategy aligned with demographic shifts toward older, rotator-cuff-compromised patients. Its Tornier acquisition gave it access to a reverse system with strong European and U.S. adoption, and since then, Stryker has optimized these platforms with features like streamlined instrumentation and intraoperative flexibility. Its limited presence in hemi and revision procedures suggests a deliberate prioritization of high-growth, high-margin areas rather than a lack of capability.

- DePuy Synthes was the third-leading competitor in the shoulder reconstruction device market in 2024. DePuy’s strength lies in the trauma-adjacent shoulder market, especially proximal humerus plating. Rather than trying to dominate across all implant categories, it has embedded shoulder arthroplasty into its larger trauma ecosystem, leveraging orthopedic hardware platforms already widely used by trauma surgeons. This creates a pipeline from fracture care to shoulder arthroplasty that few others can replicate. However, its lower visibility in revision and resurfacing markets points to a narrower focus, which works well in trauma-heavy institutions but limits its ability to challenge Zimmer or Stryker in more comprehensive surgical centers.

MARKET SEGMENTATION SUMMARY

- Total Shoulder Implant Market – Further Segmented Into:

- Implant Design: Stemmed and stemless implants.

- Reversed Shoulder Implant Market

- Hemi Shoulder Implant Market – Further Segmented Into:

- Implant Design: Stemmed and stemless implants.

- Resurfacing Shoulder Implant Market

- Revision Shoulder Implant Market

- Proximal Humerus Plate and Screw Market

RESEARCH SCOPE SUMMARY

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, United Kingdom) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Malaysia, Mongolia, Myanmar, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2024 |

| Forecast | 2025-2031 |

| Historical Data | 2021-2023 |

| Quantitative Coverage | Procedure Numbers, Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.