Product Description

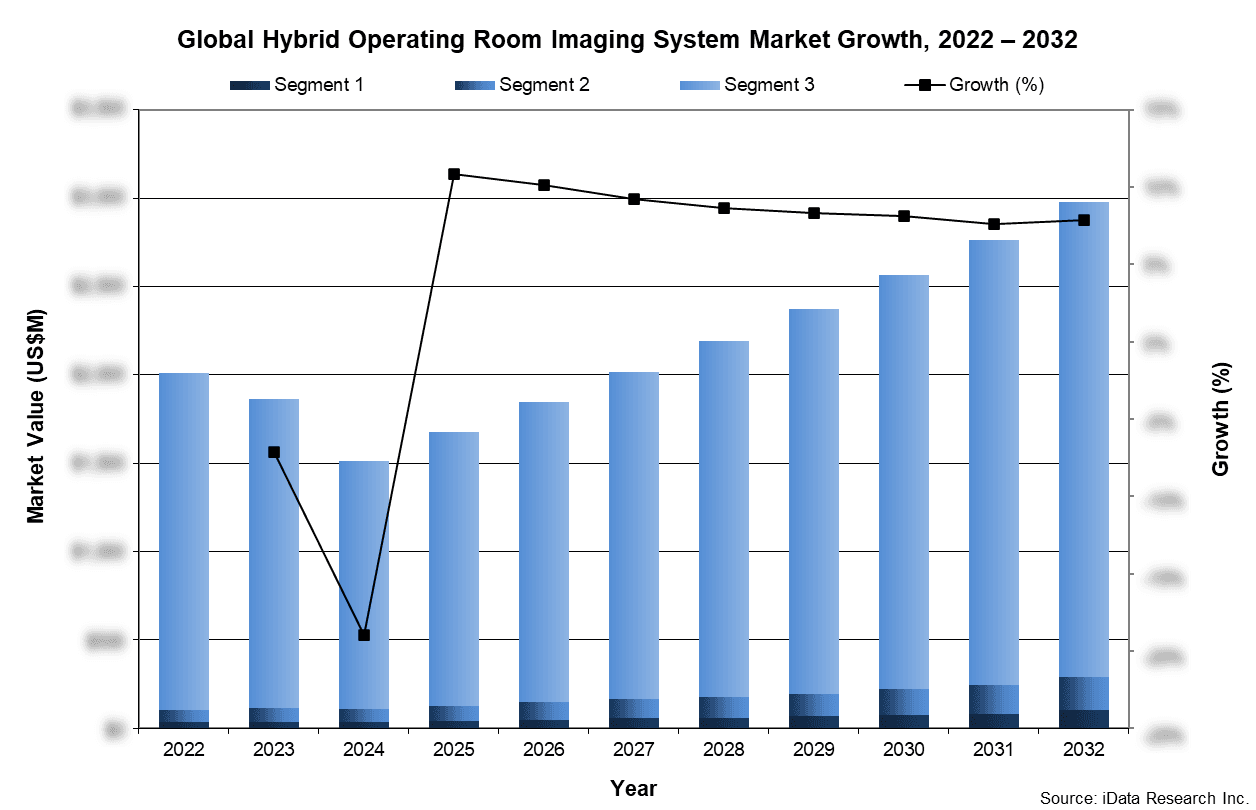

The global hybrid operating room imaging system market was valued at nearly $1.68 billion in 2025. This is expected to increase over the forecast period at a CAGR of 8.6% to reach $2.98 billion.

The full report suite on the global market for hybrid operating rooms (ORs) imaging system includes sales of imaging equipment.

The report includes data for 65 countries across 7 different regions which include North America, Latin America, Western Europe, Central & Eastern Europe, Middle East, Asia-Pacific, and Africa.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Market Drivers & Limiters

- Market Forecasts Until 2032, and Historical Data to 2022

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

Global Hybrid Operating Room Imaging System Market Trends

The hybrid imaging systems market is expected to experience significant growth in market value, driven primarily by increasing procedure volumes, while ASPs are anticipated to rise only at a minimal rate due to market maturity and competitive pressure among established vendors. North America represents the largest regional market, reflecting its high concentration of advanced care centers and early adoption of hybrid OR infrastructure, followed by Asia-Pacific and Western Europe. While North America maintains market leadership, Western Europe is expected to record the fastest growth over the forecast period, supported by hospital modernization initiatives and expanding cardiovascular and neurovascular programs. By segment, angiography systems account for the largest share of demand compared to CT and MRI in 2025 and will remain as the largest segment over the forecast period, as they are more widely applicable across cardiovascular, vascular and interventional procedures and offer greater procedural flexibility within hybrid operating room environments.

The hybrid imaging systems market is expected to experience significant growth in market value, driven primarily by increasing procedure volumes, while ASPs are anticipated to rise only at a minimal rate due to market maturity and competitive pressure among established vendors. North America represents the largest regional market, reflecting its high concentration of advanced care centers and early adoption of hybrid OR infrastructure, followed by Asia-Pacific and Western Europe. While North America maintains market leadership, Western Europe is expected to record the fastest growth over the forecast period, supported by hospital modernization initiatives and expanding cardiovascular and neurovascular programs. By segment, angiography systems account for the largest share of demand compared to CT and MRI in 2025 and will remain as the largest segment over the forecast period, as they are more widely applicable across cardiovascular, vascular and interventional procedures and offer greater procedural flexibility within hybrid operating room environments.

Global Hybrid Operating Room Imaging System Market Share Insights

- Siemens was the leading competitor in the hybrid OR imaging system market in 2025. The company offered the flagship Artis® line of interventional angiography systems, including Artis Q®, Artis Q.zen®, Artis zee®, Artis one® and, the newest and most advanced iteration, Artis pheno®. Artis pheno® differs in comparison with the other models in that the C-arm is mounted on a highly flexible robotic arm that allows for unprecedented levels of control and customization and is ideal for minimally invasive procedures. The Artis® product line offers multiple space and architecture configurations, including floor-mounted, ceiling and multipurpose flexible configurations for angiography and fluoroscopy. Other configurations include robotic imaging, X-ray imaging chain, silicon detectors and ultra-low-dose imaging. While Siemens specializes in high-end imaging systems, the fact that the company also offers lower-end alternatives has resulted in broad appeal across different-sized facilities and has helped bolster its market share. Siemens completed the acquisition of Advanced Accelerator Applications Molecular Imaging from Novartis in December 2024, strengthening its PET radiopharmaceutical manufacturing and distribution capabilities within Europe through its PETNET Solutions business. The acquisition expands Siemens Healthineers’ presence in molecular imaging supply and PET-based workflows, supporting hybrid imaging modalities such as PET/MR and PET/CT that are commonly used in advanced diagnostic and pre-procedural pathways linked to hybrid OR procedures. The company continues to strengthen its presence in the market for in 2025, the company introduced the MAGNETOM Free.XL MRI system to support interventional and procedure-oriented imaging environments. Siemens also launched AI-enabled CT solutions such as CT Coronary Cockpit to improve coronary CT angiography analysis and planning. Collectively, these developments reinforce the company’s positioning across CT, MRI, and angiography technologies that support hybrid OR and image-guided therapy workflows.

- Philips was the second-leading competitor in the hybrid operating room imaging system market in 2025. The company offered the Azurion® line of integrated image-guided imaging systems and the Allura® line of interventional angiography systems. The company’s Azurion® systems are becoming popular choices in the hybrid OR due to the large amount of workflow innovation built into the products’ robust systems, which come bundled with specialized software designed to improve ease of use. In 2024 and 2025, Philips advanced its hybrid and interventional imaging portfolio across MRI, CT and angiography through a series of system and software introductions. Key developments included continued expansion of its helium-free MRI portfolio, highlighted by the launch of the BlueSeal Horizon0T MRI platform and further adoption of BlueSeal 1.5T systems to improve sustainability and siting flexibility. In 2025, Philips introduced hybrid-OR-relevant innovations including a CT-to-Azurion integration called Follow C-arm to support CT-guided PCI workflows, expanded commercial availability of LumiGuide 3D navigation integrated with the Azurion image-guided therapy platform, and launched the BlueSeal Horizon 3.0 T MRI system. In 2024, Philips continued to advance its helium-free BlueSeal MRI portfolio to enhance imaging workflows that underpin hybrid and interventional procedures. Philips is committed to contribute more in this market as Philips agreed to acquire SpectraWAVE Inc. in December 2025, adding advanced intravascular imaging and physiological assessment technologies, including the HyperVue™ Enhanced Vascular Imaging system and X1-FFR, an AI-enabled, angiography-based fractional flow reserve tool. These capabilities are expected to integrate with Philips’ Azurion image-guided therapy platform, strengthening its position in advanced angiographic and interventional imaging workflows that support hybrid OR procedures.

- GE Healthcare was the third-leading competitor in the hybrid OR imaging system market in 2025. The company offered two imaging solutions for the hybrid OR, the Discovery® IGS 730 and 740. These angiographic systems for the hybrid OR provide high-end fluoroscopy image guidance, advanced applications and 3D image fusion and can be used in a wide range of endovascular, cardiac, hybrid and open surgical procedures. In addition to the Discovery® imaging systems, the Innova® IGS 540 angiography system for interventional radiology/vascular applications may also be used for hybrid ORs, although this option is not as popular compared with GE’s other hybrid offerings. In 2024, GE HealthCare advanced its CT offerings with the Revolution™ Apex and Revolution™ Ascend platforms, focusing on efficiency and advanced cardiac imaging relevant to hybrid OR planning. In 2025, the company introduced Freelium sealed magnet MRI technology and showcased the Revolution Vibe CT system at ECR 2025, alongside next-generation MRI scanners such as Signa Bolt and Signa Sprint with AI-enhanced workflow features. GE HealthCare also presented its photon-counting CT solution Photonova Spectra and advanced CT post-processing software for coronary and vascular interpretation. These developments, combined with expanded AI integration through a collaboration with NVIDIA, support enhanced imaging quality and workflow efficiency in hybrid OR and interventional imaging environments.

Global Hybrid Operating Room Imaging System Market Segmentation Summary

- MRI Imaging System Market

- CT Imaging System Market

- Angiography Imaging System Market

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, United Kingdom) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Malaysia, Mongolia, Myanmar, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2025 |

| Forecast | 2026-2032 |

| Historical Data | 2022-2024 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.