Product Description

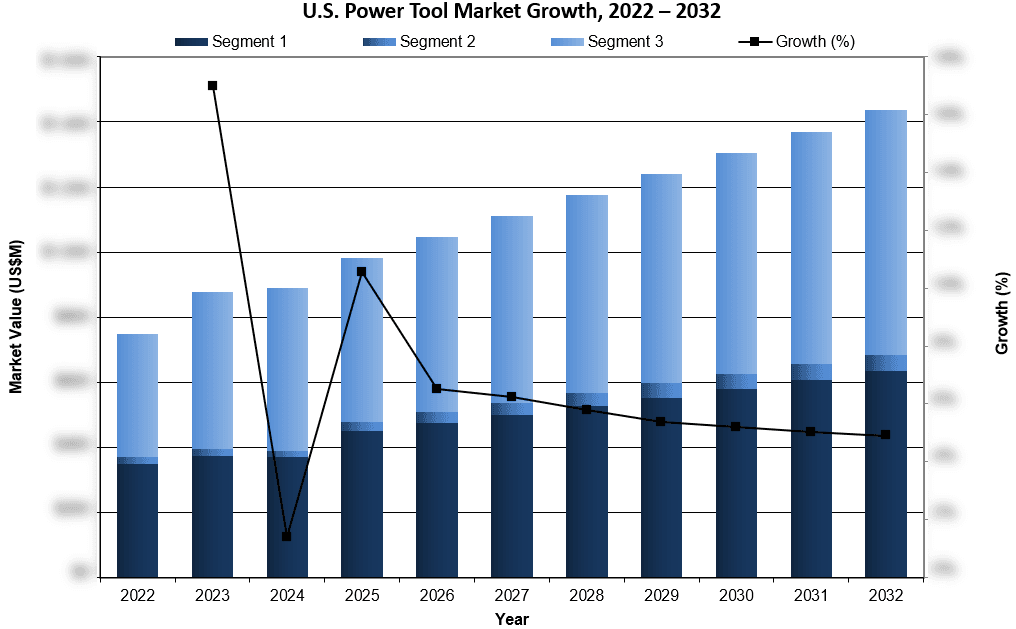

Overall, the U.S. power tool market was valued at approximately $980 million in 2025. This is expected to increase over the forecast period at a CAGR of 5.6% to reach approximately $1.44 billion.

The full report suite on the U.S. market for power tools includes detailed analysis of capital handpieces, attachments and accessories across joint, trauma and small bone power tool segments. Each section provides market size, unit volumes, ASP trends, replacement cycles, installed base dynamics and competitive positioning through 2032.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2024

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

U.S. Power Tool Market Trends

A major market driver is the steady growth in orthopedic procedure volumes, particularly joint arthroplasty and complex fracture fixation. The growing prevalence of osteoarthritis, osteoporosis and other degenerative musculoskeletal conditions continues to expand the addressable patient population. As the population ages and life expectancy rises, procedure volumes for hip, knee and shoulder reconstruction are increasing steadily. Because many joint and large bone procedures require powered resection, drilling and reaming, procedural growth directly translates into recurring demand for attachments and accessories, while also supporting long-term handpiece replacement.

U.S. Power Tool Market Share Insights

- Stryker was the overall share leader in the combined U.S. power tool market in 2025, maintaining dominant positions across both joint and trauma segments. In joint power tools, the company held near-total share in small and medium bone applications and a commanding majority in large bone, supported by broad adoption of its System 8 and System 9 platforms. In trauma, Stryker led the large bone segment and maintained a strong position in medium bone, reinforcing its scale advantage across hospital-based orthopedic programs. In high-speed drills, Stryker competes through its πDrive (Pi Drive) platform, used in neuro, spine and ENT applications requiring high rotational speed and precision. Although its high-speed drill share is smaller than the segment leader, πDrive complements Stryker’s broader powered instrumentation portfolio. The company’s leadership is underpinned by installed base penetration, platform standardization across service lines and long-standing hospital procurement relationships that support recurring attachment revenue and capital replacement cycles.

- Medtronic was the leading competitor in the U.S. high-speed drill market in 2025, driven primarily by its Midas Rex™ platform. Midas Rex maintains deep penetration in neurosurgery, spine and ENT procedures where precision drilling is critical, securing Medtronic the largest share of the high-speed segment and a substantial position in the overall powered instrumentation landscape. While the company has limited exposure in joint arthroplasty power tools and traditional large bone trauma systems, its dominance in specialty surgical applications is highly defensible. Integration with Medtronic’s spine and neurosurgery portfolios supports procedural bundling, strong physician loyalty and sustained capital utilization within specialty service lines.

- CONMED held a smaller but established position across multiple U.S. power tool segments in 2025. In joint power tools, the company maintained modest share in medium and large bone applications with limited participation in small bone. Across trauma and high-speed drill categories, CONMED competes through its Hall® line of products, which carries longstanding brand recognition in orthopedic and trauma settings. Although its total market share remains limited relative to Stryker and Medtronic, CONMED benefits from its broader orthopedic and sports medicine portfolio, enabling selective penetration in accounts that favor alternative suppliers or dual-vendor strategies and allowing continued participation in capital replacement and attachment-driven revenue cycles.

U.S. Power Tool Market Segmentation Summary

- Joint Power Tool Market – Further Segmented Into:

- Device type: Small, Medium, and Large Bone Joint Power Tool.

- Trauma Power Tool Market – Further Segmented Into:

- Device type: Small Bone Trauma Power Tool Accessory & Attachments, Medium, and Large Bone Trauma Power Tool.

- Small Bone Power Tool Market – Further Segmented Into:

- Device type: Power Console System, Small Bone Power Tool, and High-Speed Drill.

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Region | United States |

| Base Year | 2025 |

| Forecast | 2026-2032 |

| Historical Data | 2022-2024 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.