Product Description

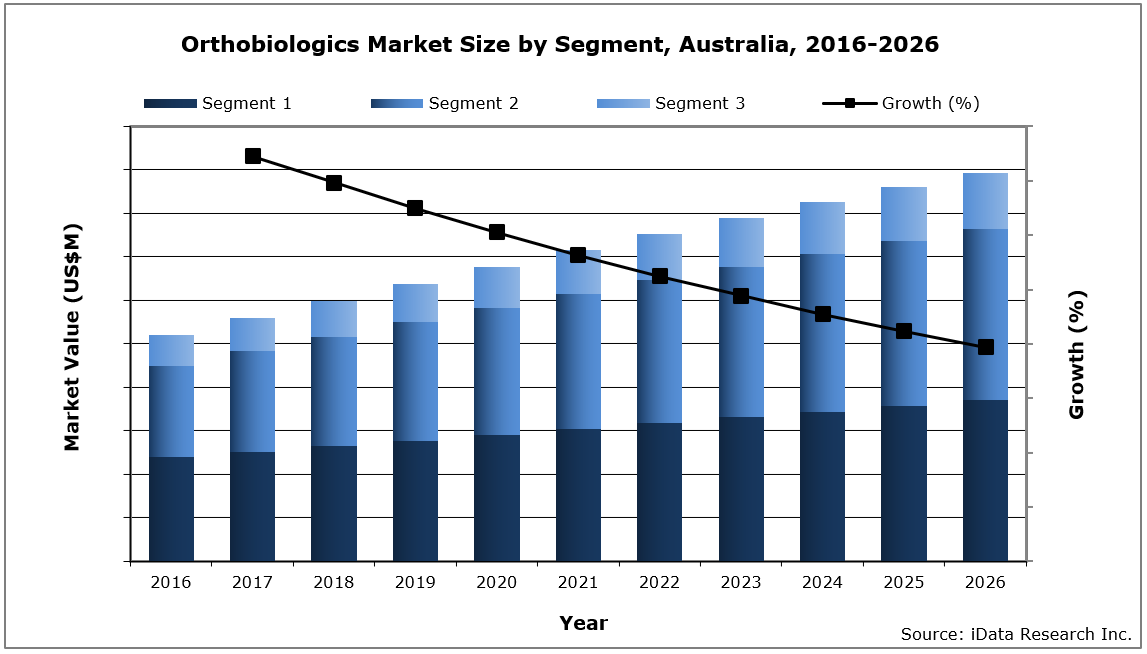

In 2020, the Australian orthobiologics market size was valued at $63.8 million, with over 29,000 bone grafting procedures performed every year. The market size is expected to increase at a compound annual growth rate (CAGR) of 4.9% to reach $89.4 million in 2026.

Throughout this medical market research, we analyzed 48 orthobiologics companies across Australia and used our comprehensive methodology to understand the market sizes, unit sales, company market shares, and to create accurate forecasts.

While this MedSuite report contains all of the Australian Orthopedic Biomaterials market data and analysis, each of the market segments is also available as stand-alone MedCore reports. This allows you to get access to only the market research that you need.

DATA TYPES INCLUDED

- Unit Sales, Average Selling Prices, Market Value & Growth Trends

- Forecasts Until 2026, and Historical Data to 2016

- Market Drivers & Limiters for Each Orthopedic Biomaterials Device market

- Competitive Analysis with Market Shares for Each Segment

- Recent Mergers & Acquisitions

- Orthobiologics Procedure Volumes

- Disease Overviews and Demographic Information

- Company Profiles, Product Portfolios and SWOT for Top Competitors

- Related Press Releases from Top Competitors

Market Value and Industry Trends

With some exceptions, tissue supply for allografts and DBM allografts is constrained by the number of available donors. Furthermore, allografts are primarily sold by bone banks in Australia, which is attributed to a relatively high barrier to entry to the market for international companies. As the population ages, there will be a lower supply of eligible bone graft donors.

Surgical procedures that require the use of orthopedic biomaterials are generally associated with diseases and indications that become more prevalent in the population with an increase in age, such as osteoarthritis of the spine and knee. In 2019, over 15% of Australians were aged 65 and over; this proportion is projected to grow steadily over the forecast period, as further cohorts of baby boomers turn 65.

Single-injection HA viscosupplementation products are relatively new to the Australian market. In 2019, there were three single-injection products available: Sanofi’s Synvisc-One®, Bioventus’ Durolane® and Anika Therapeutics’ MONOVISC®. Although three-injection products were available in Australia before single-injection products, the benefits of the latter are typically perceived to outweigh the favorable cost of the former. As a result, single-injection products are expected to> continue to cannibalize three-injection products over the forecast period.

Competitive Analysis

By 2020, the leading competitor in the Australian orthopedic biomaterials market was Medtronic. The company has established this role through strong performance of its growth factor product line, INFUSE®, which first entered the market in 2006. Medtronic also held a notable position in the DBM allograft and synthetic markets.

DePuy Synthes was the second-leading competitor in the Australian market, which was solely attributed to its leading position in the orthopedic bone graft substitute market. The company was particularly strong in the DBM allograft market, which continues to be the fastest-growing bone graft substitute segment.

Other notable competitors included, but were not limited to, Stryker, bone banks, Wright Medical, Cerapedics, Sanofi, Bioventus and Anika Therapeutics. Unlike the bone graft substitute market, which is heavily fragmented, the orthopedic graft factor and HA viscosupplementation markets are controlled by a smaller number of companies.

Segments Covered

Click on each title to view more detailed market segmentation.

- Procedure Volumes for Orthopedic Biomaterials Devices – MedPro – The Complete procedural analysis for each segment of the Australian Orthopedic Biomaterials market.

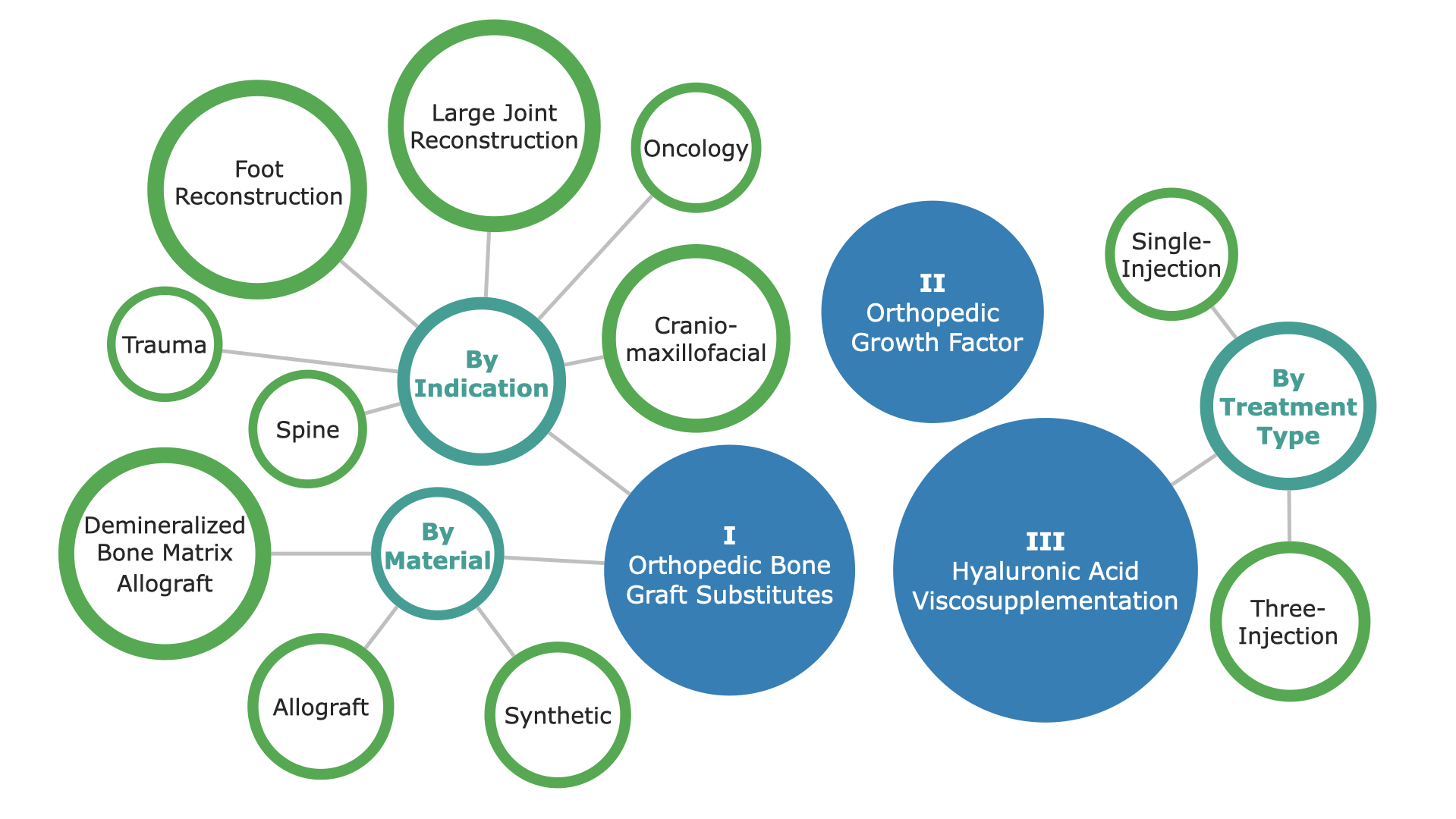

- Orthopedic Bone Graft Substitute Market – MedCore – This market is further segmented by Material Type, including Allograft, Demineralized Bone Matrix Allograft, and Synthetic. Each of these Material Types are segmented by Spine, Trauma, Large Joint Reconstruction, Craniomaxillofacial, and Oncology.

- Orthopedic Growth Factor Market – MedCore – In-depth analysis of the Orthopedic Growth Factor market.

- Hyaluronic Acid Viscosupplementation Market – MedCore – This market is categorized by Treatment Type, including Single-Injection and Three-Injection.

Detailed Market Segmentation

DON’T SEE THE SEGMENT OR DATA YOU NEED?

Feel free to contact us or send a request by pressing one of the buttons below.

FREE Sample Report

Table of Contents

TABLE OF CONTENTS I

LIST OF FIGURES VIII

LIST OF CHARTS XV

EXECUTIVE SUMMARY 1

AUSTRALIAN ORTHOPEDIC BIOMATERIALS MARKET OVERVIEW 1

COMPETITIVE ANALYSIS 3

MARKET TRENDS 5

MARKET DEVELOPMENTS 6

PROCEDURE NUMBERS 7

MARKETS INCLUDED 8

KEY REPORT UPDATES 10

VERSION HISTORY 10

RESEARCH METHODOLOGY 11

Step 1: Project Initiation & Team Selection 11

Step 2: Prepare Data Systems and Perform Secondary Research 14

Step 3: Preparation for Interviews & Questionnaire Design 16

Step 4: Performing Primary Research 17

Step 5: Research Analysis: Establishing Baseline Estimates 19

Step 6: Market Forecast and Analysis 20

Step 7: Identify Strategic Opportunities 22

Step 8: Final Review and Market Release 23

Step 9: Customer Feedback and Market Monitoring 24

PRODUCT ASSESSMENT 25

2.1 INTRODUCTION 25

2.2 PRODUCT PORTFOLIOS 25

2.2.1 Bone Graft Substitutes 26

2.2.2 Growth Factors 32

2.2.2.1 Other Products 35

2.2.3 Hyaluronic Acid Viscosupplementation (HAV) 37

2.3 REGULATORY ISSUES AND RECALLS 40

2.3.1 Bone Graft Substitutes 40

2.3.1.1 Allografts 40

2.3.1.1.1 MTF 40

2.3.1.2 DBM 40

2.3.1.2.1 AlloSource 40

2.3.1.2.2 SeaSpine 41

2.3.1.2.3 RTI Surgical 41

2.3.1.3 Synthetics 41

2.3.1.3.1 Abyrx 41

2.3.1.3.2 Zimmer Biomet 42

2.3.2 Growth Factors 42

2.3.2.1.1 Medtronic 42

2.3.3 Hyaluronic Acid Viscosupplementation 43

2.3.3.1 Three-injection 43

2.3.3.1.1 Ferring Pharmaceuticals 43

2.4 CLINICAL TRIALS 44

2.4.1 Bone Graft Substitutes 44

2.4.1.1 Allografts 44

2.4.1.1.1 Providence Medical Technology 44

2.4.1.1.2 The University of Texas Health Science 44

2.4.1.1.3 University of Winchester 45

2.4.1.2 BDM 45

2.4.1.2.1 K2M 45

2.4.1.2.2 Zimmer Biomet 46

2.4.1.3 Synthetics 46

2.4.1.3.1 Baxter 46

2.4.1.3.2 Bonesupport 47

2.4.1.3.3 DePuy Synthes 47

2.4.1.3.4 NuVasive 49

2.4.1.3.5 RTI surgical 49

2.4.1.3.6 Sunstar GUIDOR 50

2.4.1.4 Other materials and comparison 51

2.4.1.4.1 Seoul National University Hospital. 51

2.4.1.4.2 Sewon Cellontech 51

2.4.1.4.3 SurgaColl Technologies Limited 52

2.4.1.4.4 University of Colorado 52

2.4.1.4.5 University of Padova 53

2.4.2 Growth Factors 53

2.4.2.1.1 Bioventus 53

2.4.2.1.2 Cerapedics 54

2.4.2.1.3 CGBio 54

2.4.2.1.4 Isto 55

2.4.2.1.5 Medtronic 55

2.4.2.1.6 NuVasive 57

2.4.2.1.7 Wright 57

2.4.2.1.8 Others 58

2.4.3 Hyaluronic Acid Viscosupplementation 59

2.4.3.1.1 Anika Therapeutics 59

2.4.3.1.2 Bioventus 60

2.4.3.1.3 Cairo University 61

2.4.3.1.4 Ferring Pharmaceuticals 61

2.4.3.1.5 Federal University of Minas Gerais 62

2.4.3.1.6 Fidia Pharma USA Inc. 62

2.4.3.1.7 Istituto Ortopedico Rizzoli 63

2.4.3.1.8 University Hospital 63

2.4.3.1.9 Universidade Nova de Lisboa 64

AUSTRALIAN ORTHOPEDIC BIOMATERIALS MARKET OVERVIEW 65

3.1 INTRODUCTION 65

3.1.1 Bone Graft Substitutes 65

3.1.2 Growth Factors 65

3.1.3 Hyaluronic Acid (HA) Viscosupplementation 66

3.2 CURRENCY EXCHANGE RATE 67

3.3 MARKET OVERVIEW AND TREND ANALYSIS 68

3.4 DRIVERS AND LIMITERS 76

3.4.1 Market Drivers 76

3.4.2 Market Limiters 76

3.5 COMPETITIVE MARKET SHARE ANALYSIS 78

3.6 MERGERS AND ACQUISITIONS 84

3.7 COMPANY PROFILES 86

3.7.1 Anika Therapeutics 86

3.7.2 Bioventus 87

3.7.3 DePuy Synthes 88

3.7.4 Ferring Pharmaceuticals 89

3.7.5 Fidia Pharmaceuticals 90

3.7.6 Genzyme (Sanofi Group) 91

3.7.7 Harvest Technologies (Terumo BCT) 92

3.7.8 Integra LifeSciences 93

3.7.9 Medtronic 94

3.7.10 Musculoskeletal Transplant Foundation (MTF) 96

3.7.11 NuVasive 97

3.7.12 Orthofix 98

3.7.13 RTI Surgical 99

3.7.14 Stryker 100

3.7.15 Vericel Corporation (formerly Aastrom Bioscience) 101

3.7.16 Zimmer Biomet 102

3.8 SWOT ANALYSIS 104

3.8.1 Anika Therapeutics 104

3.8.2 Bioventus 106

3.8.3 DePuy Synthes 108

3.8.4 Ferring Pharmaceuticals 109

3.8.5 Fidia Pharmaceuticals 110

3.8.7 Harvest Technologies (Terumo BCT) 112

3.8.8 Integra LifeSciences 113

3.8.9 Medtronic 114

3.8.10 Musculoskeletal Transplant Foundation (MTF) 115

3.8.11 NuVasive 116

3.8.12 Orthofix 117

3.8.14 Stryker 119

3.8.15 Vericel Corporation (formerly Aastrom Bioscience) 120

3.8.16 Zimmer Biomet 121

PROCEDURE NUMBERS 123

4.1 INTRODUCTION 123

4.2 PROCEDURES 124

4.2.1 Orthopedic Biomaterial Procedures by Segment 124

4.2.2 Orthopedic Bone Grafting Procedures 126

4.2.2.1 Units per Procedure by Indication 126

4.2.2.2 Orthopedic Bone Grafting Procedures by Material 127

4.2.2.2.1 Autograft Procedures by Indication 129

4.2.2.2.2 Allograft Procedures by Indication 132

4.2.2.2.3 DBM Allograft Procedures by Indication 135

4.2.2.2.4 Synthetic Procedures by Indication 138

4.2.2.3 Orthopedic Bone Grafting Procedures by Indication 141

4.2.3 Orthopedic Growth Factor Procedures 144

4.2.4 Hyaluronic Acid Supplementation Procedures 146

4.2.4.1 Hyaluronic Acid Supplementation Procedures by Injection Cycle 146

ORTHOPEDIC BONE GRAFT SUBSTITUTE MARKET 148

5.1 INTRODUCTION 148

5.2 MARKET OVERVIEW 149

5.2.1 Orthopedic Bone Graft Substitute Market by Material 149

5.2.2 Orthopedic Bone Graft Substitute Market by Indication 154

5.3 MARKET ANALYSIS AND FORECAST 160

5.3.1 Total Orthopedic Bone Graft Substitute Market 160

5.3.2 Orthopedic Bone Graft Substitute Market by Material 162

5.3.2.1 Allograft Bone Graft Substitute Market 162

5.3.2.1.1 Allograft Bone Graft Substitute Market by Indication 164

5.3.2.2 Demineralized Bone Matrix Allograft Bone Graft Substitute Market 178

5.3.2.2.1 Demineralized Bone Matrix Allograft Bone Graft Substitute Market by Indication 180

5.3.2.3 Synthetic Bone Graft Substitute Market 194

5.3.2.3.1 Synthetic Bone Graft Substitute Market by Indication 196

5.3.3 Orthopedic Bone Graft Substitute Market by Indication 210

5.3.3.1 Spine Bone Graft Substitute Market 210

5.3.3.2 Cervical Spine Bone Graft Substitute Market 212

5.3.3.3 Thoracolumbar Spine Bone Graft Substitute Market 214

5.3.3.4 Trauma Bone Graft Substitute Market 216

5.3.3.5 Non-Union Trauma Bone Graft Substitute Market 218

5.3.3.6 Fresh Fracture Trauma Bone Graft Substitute Market 220

5.3.3.7 Large Joint Reconstruction Bone Graft Substitute Market 222

5.3.3.8 Hip Reconstruction Bone Graft Substitute Market 224

5.3.3.9 Knee Reconstruction Bone Graft Substitute Market 226

5.3.3.10 Foot Reconstruction Bone Graft Substitute Market 228

5.3.3.11 Craniomaxillofacial Bone Graft Substitute Market 230

5.3.3.12 Oncology Bone Graft Substitute Market 232

5.4 DRIVERS AND LIMITERS 234

5.4.1 Market Drivers 234

5.4.2 Market Limiters 234

5.5 COMPETITIVE MARKET SHARE ANALYSIS 236

ORTHOPEDIC GROWTH FACTOR MARKET 240

6.1 INTRODUCTION 240

6.1.1 BMP-2 (Medtronic) 241

6.1.2 PDGF-BB (Wright Medical) 241

6.1.3 P-15 Synthetic Small Peptide (Cerapedics) 241

6.1.4 P-15 Synthetic Small Peptide (Biocomposites) 241

6.2 MARKET ANALYSIS AND FORECAST 242

6.3 DRIVERS AND LIMITERS 244

6.3.1 Market Drivers 244

6.3.2 Market Limiters 244

6.4 COMPETITIVE MARKET SHARE ANALYSIS 246

HYALURONIC ACID VISCOSUPPLEMENTATION MARKET 249

7.1 INTRODUCTION 249

7.1.1 Benefits of Viscosupplementation 250

7.1.2 Synovial Fluid 250

7.2 MARKET OVERVIEW 251

7.3 MARKET ANALYSIS AND FORECAST 257

7.3.1 Total Hyaluronic Acid Viscosupplementation Market 257

7.3.2 Single-Injection Hyaluronic Acid Viscosupplementation Market 259

7.3.3 Three-Injection Hyaluronic Acid Viscosupplementation Market 261

7.4 DRIVERS AND LIMITERS 263

7.4.1 Market Drivers 263

7.4.2 Market Limiters 263

7.5 COMPETITIVE MARKET SHARE ANALYSIS 265

ABBREVIATIONS 268

Companies Included

The

Orthobiologics Market Report Suite | Australia | 2020-2026 | MedSuite includes analysis on the following companies currently active in this market:

- Alphatec

- Anika Therapeutics

- Arthrex

- Australian Biotechnologies

- Australian Tissue Donation Network

- B. Braun

- Barwon Health Bone Bank

- Baxter

- Biocomposites

- Bioventus

- Cerapedics

- Corin

- DePuy Synthes

- Donor Tissue Bank of Victoria

- Finceramica

- Globus Medical

- Hunter New England and Local Health District

- Hunter New England Bone Bank

- Institute of Medical & Veterinary Science

- Joy Surgical

- JRI Orthopaedics

- Kasios

- LifeHealthcare

- LMT Surgical

|

- Alphatec

- Anika Therapeutics

- Arthrex

- Australian Biotechnologies

- Australian Tissue Donation Network

- B. Braun

- Barwon Health Bone Bank

- Baxter

- Biocomposites

- Bioventus

- Cerapedics

- Corin

- DePuy Synthes

- Donor Tissue Bank of Victoria

- Finceramica

- Globus Medical

- Hunter New England and Local Health District

- Hunter New England Bone Bank

- Institute of Medical & Veterinary Science

- Joy Surgical

- JRI Orthopaedics

- Kasios

- LifeHealthcare

- LMT Surgical

|

Chart List

LIST OF CHARTS

Chart 1 1: Orthopedic Biomaterials Market by Segment, Australia, 2016 – 2026 2

Chart 1 2: Orthopedic Biomaterials Market Overview, Australia, 2019 & 2026 2

Chart 3 1: Orthopedic Biomaterials Market by Segment, Australia, 2016 – 2026 71

Chart 3 2: Orthopedic Biomaterials Market Breakdown, Australia, 2019 72

Chart 3 3: Orthopedic Biomaterials Market Breakdown, Australia, 2026 73

Chart 3 4: Growth Rates by Segment, Orthopedic Biomaterials Market, Australia, 2017 – 2026 75

Chart 3 5: Leading Competitors, Orthopedic Biomaterials Market, Australia, 2019 83

Chart 4 1: Orthopedic Biomaterials Market by Segment, Australia, 2016 – 2026 125

Chart 4 2: Orthopedic Bone Grafting Procedures by Material, Australia, 2016 – 2026 128

Chart 4 3: Autograft Procedures by Indication, Australia, 2016 – 2026 131

Chart 4 4: Allograft Procedures by Indication, Australia, 2016 – 2026 134

Chart 4 5: DBM Allograft Procedures by Indication, Australia, 2016 – 2026 137

Chart 4 6: Synthetic Procedures by Indication, Australia, 2016 – 2026 140

Chart 4 7: Orthopedic Bone Grafting Procedures by Indication, Australia, 2016 – 2026 143

Chart 4 8: Orthopedic Growth Factor Procedures, Australia, 2016 – 2026 145

Chart 4 9: Hyaluronic Acid Viscosupplementation Procedures by Injection Cycle, Australia, 2016 – 2026 147

Chart 5 1: Orthopedic Bone Graft Substitute Market by Material, Australia, 2016 – 2026 151

Chart 5 2: Orthopedic Bone Graft Substitute Market Breakdown by Material, Australia, 2019 152

Chart 5 3: Orthopedic Bone Graft Substitute Market Breakdown by Material, Australia, 2026 153

Chart 5 4: Orthopedic Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 157

Chart 5 5: Orthopedic Bone Graft Substitute Market Breakdown by Indication, Australia, 2019 158

Chart 5 6: Orthopedic Bone Graft Substitute Market Breakdown by Indication, Australia, 2026 159

Chart 5 7: Total Orthopedic Bone Graft Substitute Market, Australia, 2016 – 2026 161

Chart 5 8: Allograft Bone Graft Substitute Market, Australia, 2016 – 2026 163

Chart 5 9: Allograft Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 165

Chart 5 10: Demineralized Bone Matrix Allograft Bone Graft Substitute Market, Australia, 2016 – 2026 179

Chart 5 11: Demineralized Bone Matrix Allograft Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 181

Chart 5 12: Synthetic Bone Graft Substitute Market, Australia, 2016 – 2026 195

Chart 5 13: Synthetic Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 197

Chart 5 14: Spine Bone Graft Substitute Market, Australia, 2016 – 2026 211

Chart 5 15: Cervical Spine Bone Graft Substitute Market, Australia, 2016 – 2026 213

Chart 5 16: Thoracolumbar Spine Bone Graft Substitute Market, Australia, 2016 – 2026 215

Chart 5 17: Trauma Bone Graft Substitute Market, Australia, 2016 – 2026 217

Chart 5 18: Non-Union Trauma Bone Graft Substitute Market, Australia, 2016 – 2026 219

Chart 5 19: Fresh Fracture Trauma Bone Graft Substitute Market, Australia, 2016 – 2026 221

Chart 5 20: Large Joint Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 223

Chart 5 21: Hip Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 225

Chart 5 22: Knee Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 227

Chart 5 23: Foot Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 229

Chart 5 24: Craniomaxillofacial Bone Graft Substitute Market, Australia, 2016 – 2026 231

Chart 5 25: Oncology Bone Graft Substitute Market, Australia, 2016 – 2026 233

Chart 5 26: Leading Competitors, Orthopedic Bone Graft Substitute Market, Australia, 2019 239

Chart 6 1: Orthopedic Growth Factor Market, Australia, 2016 – 2026 243

Chart 6 2: Leading Competitors, Orthopedic Growth Factor Market, Australia, 2019 248

Chart 7 1: Hyaluronic Acid Viscosupplementation Market by Segment, Australia, 2016 – 2026 254

Chart 7 2: Hyaluronic Acid Viscosupplementation Market Breakdown, Australia, 2019 255

Chart 7 3: Hyaluronic Acid Viscosupplementation Market Breakdown, Australia, 2026 256

Chart 7 4: Total Hyaluronic Acid Viscosupplementation Market, Australia, 2016 – 2026 258

Chart 7 5: Single-Injection Hyaluronic Acid Viscosupplementation Market, Australia, 2016 – 2026 260

Chart 7 6: Three-Injection Hyaluronic Acid Viscosupplementation Market, Australia, 2016 – 2026 262

Chart 7 7: Leading Competitors, Hyaluronic Acid Viscosupplementation Market, Australia, 2019 267

Figure List

LIST OF FIGURES

Figure 1 1: Orthopedic Biomaterials Market Share Ranking by Segment, Australia, 2019 3

Figure 1 2: Companies Researched in this Report 4

Figure 1 3: Factors Impacting the Orthopedic Biomaterials Market by Segment, Australia 5

Figure 1 4: Recent Events in the Orthopedic Biomaterials Market, Australia, 2017 – 2019 6

Figure 1 5: Orthopedic Biomaterials Procedures Covered, Australia 7

Figure 1 6: Orthopedic Biomaterials Markets Covered (1 of 2) 8

Figure 1 7: Orthopedic Biomaterials Markets Covered (2 of 2) 9

Figure 1 8: Key Report Updates 10

Figure 1 9: Version History 10

Figure 2 1: Bone Graft Substitutes Products by Company (1 of 4) 28

Figure 2 2: Bone Graft Substitutes Products by Company (2 of 4) 29

Figure 2 3: Bone Graft Substitutes Products by Company (3 of 4) 30

Figure 2 4: Bone Graft Substitutes Products by Company (4 of 4) 31

Figure 2 5: Growth Factor Products by Company 36

Figure 2 6: Hyaluronic Acid Viscosupplementation by Products by Company 39

Figure 2 7: Class 2 Device Recall Musculoskeletal Transplant Foundation Allofix Insertion Kit 40

Figure 2 8: Class 2 Device Recall AlloFuse DBM Putty 5cc 40

Figure 2 9: Class 2 Device Recall Accell Evo3c Demineralized Bone Matrix Putty 41

Figure 2 10: Class 2 Device Recall RTI Biologics BioSet IC RT Paste 2 cc 41

Figure 2 11: Class 2 Device Recall Hemostatic Bone Putty 41

Figure 2 12: Class 2 Device Recall Endobon Xenograft Granules 42

Figure 2 13: Class 2 Device Recall Endobon Xenograft Granules 42

Figure 2 14: Class 2 Device Recall INFUSE Bone Graft X SMALL KIT 42

Figure 2 15: Class 3 Device Recall Euflexxa (1 sodium hyaluronate) 43

Figure 2 16: Evaluation of DTRAX Graft in Patients with Cervical Degenerative Disc Disease 44

Figure 2 17: Ridge Preservation Using FDBA and a Collagen Wound Dressing in Molar Sites. 44

Figure 2 18: Assessing Physical Activity Levels of Patients Following HTO. 45

Figure 2 19: Evaluation of Fusion Rate Using K2M VESUVIUS® Demineralized Fibers with K2M EVEREST® Spinal System 45

Figure 2 20: Evaluation of Zimmer Puros® Allograft vs. Creos™ Allograft for Alveolar Ridge Preservation 46

Figure 2 21: Synthetic Bone Graft Substitute vs. Autologous Spongiosa in Revision Anterior Cruciate Ligament Reconstruction 46

Figure 2 22: Cerament Treatment of Fracture Defects (CERTiFy) 47

Figure 2 23: Comparison of Bioactive Glass and Beta-Tricalcium Phosphate as Bone Graft Substitute (BAGvsTCP) 47

Figure 2 24: Evaluation of Fusion Rate of Anterior Cervical Discectomy and Fusion (ACDF) Using Cervios ChronOs™ and Bonion™ 48

Figure 2 25: AttraX® Putty vs. Autograft in XLIF® 49

Figure 2 26: Comparison of nanOss Bioactive with Autograft and Bone Marrow Aspirate to Autograft in the Posterolateral Spine 49

Figure 2 27: Assessment of nanOss Bioactive 3D in the Posterolateral Spine 50

Figure 2 28: Assessment of Ridge Preservation Using Moldable Beta-tricalcium Phosphate Bone Grafting System 50

Figure 2 29: Outcome Comparison of Allograft and Synthetic Bone Substitute in High Tibial Osteotomy 51

Figure 2 30: Efficacy and Safety of SurgiFill™ on Spinal Fusion 51

Figure 2 31: Assessment of HydroxyColl Bone Graft Substitute in High Tibial Osteotomy Wedge Grafting. (HColl_HTO) 52

Figure 2 32: Outcomes of the Evans Calcaneal Lengthening Based on Bone Grafting Material 52

Figure 2 33: Deproteinized Bovine Bone in Alveolar Bone Critical Size Defect (>2cm) Secondary to Cyst Removal 53

Figure 2 34: A Prospective Study of Instrumented, Posterolateral Lumbar Fusions (PLF) With OsteoAMP® 53

Figure 2 35: The Clinical Effect of i-FACTOR® Versus Allograft in Non-instrumented Posterolateral Spondylodesis Operation 54

Figure 2 36: Clinical Study of Injectable Ceramics Bone Graft Substitute Containing rhBMP-2 54

Figure 2 37: Prospective Study of Safety and Efficacy of InQu® Bone Graft Extender in Lumbar Interbody Fusion Surgery (Intebody) 55

Figure 2 38: A Study of INFUSE Bone Graft (BMP-2) in the Treatment of Tibial Pseudarthrosis in Neurofibromatosis Type 1 55

Figure 2 39: Clinical Study of INFUSE® Bone Graft Compared to Autogenous Bone Graft for Vertical Ridge Augmentation 56

Figure 2 40: Parallel Study Between BMP-2 and Autologous Bone Graft After Ilizarow Treatment 56

Figure 2 41: RCT of AttraX® Putty vs. Autograft in Instrumented Posterolateral Spinal Fusion (AxA) 57

Figure 2 42: Long-term Safety and Effectiveness of AUGMENT® Bone Graft Compared to Autologous Bone Graft 57

Figure 2 43: rhBMP-2 vs Autologous Bone Grafting for the Treatment of Non-union of the Docking Site in Tibial Bone Transport 58

Figure 2 44: Evaluation of Radiculitis Following Use of Bone Morphogenetic Protein-2 for Interbody Arthrodesis in Spinal Surgery 58

Figure 2 45: Study of Cingal™ for the Relief of Knee Osteoarthritis Compared to Triamcinolone Hexacetonide at 39 Weeks Follow-Up (Cingal17-02) 59

Figure 2 46: HyaloFAST Trial for Repair of Articular Cartilage in the Knee (FastTRACK) 59

Figure 2 47: Effectiveness of Two Hyaluronic Acids in Osteoarthritis of the Knee 60

Figure 2 48: The Effect of Topical Application of Hyaluronic Acid on Immediate Dental Implant 61

Figure 2 49: To Look at the Characteristics of Synovial Fluid and Cartilage Matrix in Osteoarthritic Knees After Hyaluronic Acid Injection 61

Figure 2 50: Use of Hyaluronic Acid as a Therapeutic Strategy for Bone Repair in Humans 62

Figure 2 51: Two Weekly Intra-articular Hyaluronan Knee Injections, Given One Week Apart, of HYMOVIS Combined With a Physical Exercise Program (PEP) Compared to PEP Alone, in a Relatively Young, Active Population of Subjects With Patellofemoral Osteoarthritis (PFOA) and/or Tibiofemoral Osteoarthritis (TFOA) 62

Figure 2 52: Comparative Assessment of Viscosupplementation With Polynucleotides and Hyaluronic Acid (PNHA1401) 63

Figure 2 53: Trial Comparing Botulin Toxin Versus Hyaluronic Acid by Intra-articular Injection (GOTOX) 63

Figure 2 54: Trial to Assess the Structural Effect and Long-term Symptomatic Relief of Intra-articular Injections of HA (ViscOA) 64

Figure 3 1: Currency Exchange Rate, 2019 67

Figure 3 2: Orthopedic Biomaterials Market by Segment, Australia, 2016 – 2026 (US$M) 69

Figure 3 3: Orthopedic Biomaterials Market by Segment, Australia, 2016 – 2026 (AU$M) 70

Figure 3 4: Orthopedic Biomaterials Market Growth by Segment, Australia, 2016 – 2026 74

Figure 3 5: Drivers and Limiters, Orthopedic Biomaterials Market, Australia, 2019 77

Figure 3 6: Leading Competitors, Orthopedic Biomaterials Market, Australia, 2019 82

Figure 3 7: SWOT Analysis, Anika Therapeutics (1 of 2) 104

Figure 3 8: SWOT Analysis, Anika Therapeutics (2 of 2) 105

Figure 3 9: SWOT Analysis, Bioventus (1 of 2) 106

Figure 3 10: SWOT Analysis, Bioventus (2 of 2) 107

Figure 3 11: SWOT Analysis, DePuy Synthes 108

Figure 3 12: SWOT Analysis, Ferring Pharmaceuticals 109

Figure 3 13: SWOT Analysis, Fidia Pharmaceuticals 110

Figure 3 14: SWOT Analysis, Genzyme (Sanofi) 111

Figure 3 15: SWOT Analysis, Harvest Technologies 112

Figure 3 16: SWOT Analysis, Integra LifeSciences 113

Figure 3 17: SWOT Analysis, Medtronic 114

Figure 3 18: SWOT Analysis, MTF 115

Figure 3 19: SWOT Analysis, NuVasive 116

Figure 3 20: SWOT Analysis, Orthofix 117

Figure 3 21: SWOT Analysis, RTI Surgical 118

Figure 3 22: SWOT Analysis, Stryker 119

Figure 3 23: SWOT Analysis, Vericel Corporation 120

Figure 3 24: SWOT Analysis, Zimmer Biomet (1 of 2) 121

Figure 3 25: SWOT Analysis, Zimmer Biomet (2 of 2) 122

Figure 4 1: Orthopedic Biomaterials Procedures by Segment, Australia, 2016 – 2026 124

Figure 4 2: Units per Procedure by Indication, Bone Graft Substitute Market, Australia, 2016– 2026 126

Figure 4 3: Orthopedic Bone Grafting Procedures by Material, Australia, 2016 – 2026 127

Figure 4 4: Autograft Procedures by Indication, Australia, 2016 – 2026 (1 of 2) 129

Figure 4 5: Autograft Procedures by Indication, Australia, 2016 – 2026 (2 of 2) 130

Figure 4 6: Allograft Procedures by Indication, Australia, 2016 – 2026 (1 of 2) 132

Figure 4 7: Allograft Procedures by Indication, Australia, 2016 – 2026 (2 of 2) 133

Figure 4 8: DBM Allograft Procedures by Indication, Australia, 2016 – 2026 (1 of 2) 135

Figure 4 9: DBM Allograft Procedures by Indication, Australia, 2016 – 2026 (2 of 2) 136

Figure 4 10: Synthetic Procedures by Indication, Australia, 2016 – 2026 (1 of 2) 138

Figure 4 11: Synthetic Procedures by Indication, Australia, 2016 – 2026 (2 of 2) 139

Figure 4 12: Orthopedic Bone Grafting Procedures by Indication, Australia, 2016 – 2026 (1 of 2) 141

Figure 4 13: Orthopedic Bone Grafting Procedures by Indication, Australia, 2016 – 2026 (2 of 2) 142

Figure 4 14: Orthopedic Growth Factor Procedures, Australia, 2016 – 2026 144

Figure 4 15: Hyaluronic Acid Viscosupplementation Procedures by Injection Cycle, Australia, 2016 – 2026 146

Figure 5 1: Orthopedic Bone Graft Substitute Market by Material, Australia, 2016 – 2026 (US$M) 149

Figure 5 2: Orthopedic Bone Graft Substitute Market by Material, Australia, 2016 – 2026 (AU$M) 150

Figure 5 3: Orthopedic Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 (US$M) 155

Figure 5 4: Orthopedic Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 (AU$M) 156

Figure 5 5: Total Orthopedic Bone Graft Substitute Market, Australia, 2016 – 2026 160

Figure 5 6: Allograft Bone Graft Substitute Market, Australia, 2016 – 2026 162

Figure 5 7: Allograft Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 (US$M) 164

Figure 5 8: Spine Allograft Market, Australia, 2016 – 2026 166

Figure 5 9: Cervical Spine Allograft Market, Australia, 2016 – 2026 167

Figure 5 10: Thoracolumbar Spine Allograft Market, Australia, 2016 – 2026 168

Figure 5 11: Trauma Allograft Market, Australia, 2016 – 2026 169

Figure 5 12: Non-Union Trauma Allograft Market, Australia, 2016 – 2026 170

Figure 5 13: Fresh Fracture Trauma Allograft Market, Australia, 2016 – 2026 171

Figure 5 14: Large Joint Reconstruction Allograft Market, Australia, 2016 – 2026 172

Figure 5 15: Hip Reconstruction Allograft Market, Australia, 2016 – 2026 173

Figure 5 16: Knee Reconstruction Allograft Market, Australia, 2016 – 2026 174

Figure 5 17: Foot Reconstruction Allograft Market, Australia, 2016 – 2026 175

Figure 5 18: Craniomaxillofacial Allograft Market, Australia, 2016 – 2026 176

Figure 5 19: Oncology Allograft Market, Australia, 2016 – 2026 177

Figure 5 20: Demineralized Bone Matrix Allograft Bone Graft Substitute Market, Australia, 2016 – 2026 178

Figure 5 21: Demineralized Bone Matrix Allograft Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 (US$M) 180

Figure 5 22: Spine DBM Allograft Market, Australia, 2016 – 2026 182

Figure 5 23: Cervical Spine DBM Allograft Market, Australia, 2016 – 2026 183

Figure 5 24: Thoracolumbar Spine DBM Allograft Market, Australia, 2016 – 2026 184

Figure 5 25: Trauma DBM Allograft Market, Australia, 2016 – 2026 185

Figure 5 26: Non-Union Trauma DBM Allograft Market, Australia, 2016 – 2026 186

Figure 5 27: Fresh Fracture Trauma DBM Allograft Market, Australia, 2016 – 2026 187

Figure 5 28: Large Joint Reconstruction DBM Allograft Market, Australia, 2016 – 2026 188

Figure 5 29: Hip Reconstruction DBM Allograft Market, Australia, 2016 – 2026 189

Figure 5 30: Knee Reconstruction DBM Allograft Market, Australia, 2016 – 2026 190

Figure 5 31: Foot Reconstruction DBM Allograft Market, Australia, 2016 – 2026 191

Figure 5 32: Craniomaxillofacial DBM Allograft Market, Australia, 2016 – 2026 192

Figure 5 33: Oncology DBM Allograft Market, Australia, 2016 – 2026 193

Figure 5 34: Synthetic Bone Graft Substitute Market, Australia, 2016 – 2026 194

Figure 5 35: Synthetic Bone Graft Substitute Market by Indication, Australia, 2016 – 2026 (US$M) 196

Figure 5 36: Spine Synthetic Market, Australia, 2016 – 2026 198

Figure 5 37: Cervical Spine Synthetic Market, Australia, 2016 – 2026 199

Figure 5 38: Thoracolumbar Spine Synthetic Market, Australia, 2016 – 2026 200

Figure 5 39: Trauma Synthetic Market, Australia, 2016 – 2026 201

Figure 5 40: Non-Union Trauma Synthetic Market, Australia, 2016 – 2026 202

Figure 5 41: Fresh Fracture Trauma Synthetic Market, Australia, 2016 – 2026 203

Figure 5 42: Large Joint Reconstruction Synthetic Market, Australia, 2016 – 2026 204

Figure 5 43: Hip Reconstruction Synthetic Market, Australia, 2016 – 2026 205

Figure 5 44: Knee Reconstruction Synthetic Market, Australia, 2016 – 2026 206

Figure 5 45: Foot Reconstruction Synthetic Market, Australia, 2016 – 2026 207

Figure 5 46: Craniomaxillofacial Synthetic Market, Australia, 2016 – 2026 208

Figure 5 47: Oncology Synthetic Market, Australia, 2016 – 2026 209

Figure 5 48: Spine Bone Graft Substitute Market, Australia, 2016 – 2026 210

Figure 5 49: Cervical Spine Bone Graft Substitute Market, Australia, 2016 – 2026 212

Figure 5 50: Thoracolumbar Spine Bone Graft Substitute Market, Australia, 2016 – 2026 214

Figure 5 51: Trauma Bone Graft Substitute Market, Australia, 2016 – 2026 216

Figure 5 52: Non-Union Trauma Bone Graft Substitute Market, Australia, 2016 – 2026 218

Figure 5 53: Fresh Fracture Trauma Bone Graft Substitute Market, Australia, 2016 – 2026 220

Figure 5 54: Large Joint Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 222

Figure 5 55: Hip Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 224

Figure 5 56: Knee Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 226

Figure 5 57: Foot Reconstruction Bone Graft Substitute Market, Australia, 2016 – 2026 228

Figure 5 58: Craniomaxillofacial Bone Graft Substitute Market, Australia, 2016 – 2026 230

Figure 5 59: Oncology Bone Graft Substitute Market, Australia, 2016 – 2026 232

Figure 5 60: Drivers and Limiters, Orthopedic Bone Graft Substitute Market, Australia, 2019 235

Figure 5 61: Leading Competitors, Orthopedic Bone Graft Substitute Market, Australia, 2019 238

Figure 6 1: Orthopedic Growth Factor Market, Australia, 2016 – 2026 242

Figure 6 2: Drivers and Limiters, Orthopedic Growth Factor Market, Australia, 2019 245

Figure 6 3: Leading Competitors, Orthopedic Growth Factor Market, Australia, 2019 247

Figure 7 1: Hyaluronic Acid Viscosupplementation Market by Segment, Australia, 2016 – 2026 (US$M) 252

Figure 7 2: Hyaluronic Acid Viscosupplementation Market by Segment, Australia, 2016 – 2026 (AU$M) 253

Figure 7 3: Total Hyaluronic Acid Viscosupplementation Market, Australia, 2016 – 2026 257

Figure 7 4: Single-Injection Hyaluronic Acid Viscosupplementation Market, Australia, 2016 – 2026 259

Figure 7 5: Three-Injection Hyaluronic Acid Viscosupplementation Market, Australia, 2016 – 2026 261

Figure 7 6: Drivers and Limiters, Hyaluronic Acid Viscosupplementation Market, Australia, 2019 264

Figure 7 7: Leading Competitors, Hyaluronic Acid Viscosupplementation Market, Australia, 2019 266

iData’s 9-Step Research Methodology

Our reports follow an in-depth 9-step methodology which focuses on the following research systems:

- Original primary research that consists of the most up-to-date market data

- Strong foundation of quantitative and qualitative research

- Focused on the needs and strategic challenges of the industry participants

Step 1: Project Initiation & Team Selection During this preliminary investigation, all staff members involved in the industry discusses the topic in detail.

Step 2: Prepare Data Systems and Perform Secondary Research The first task of the research team is to prepare for the data collection process: Filing systems and relational databases are developed as needed.

Step 3: Preparation for Interviews & Questionnaire Design The core of all iData research reports is primary market research. Interviews with industry insiders represent the single most reliable way to obtain accurate, current data about market conditions, trends, threats and opportunities.

Step 4: Performing Primary Research At this stage, interviews are performed using contacts and information acquired in the secondary research phase.

Step 5: Research Analysis: Establishing Baseline Estimates Following the completion of the primary research phase, the collected information must be synthesized into an accurate view of the market status. The most important question is the current state of the market.

Step 6: Market Forecast and Analysis iData Research uses a proprietary method to combine statistical data and opinions of industry experts to forecast future market values.

Step 7: Identify Strategic Opportunities iData analysts identify in broad terms why some companies are gaining or losing share within a given market segment.

Step 8: Final Review and Market Release An integral part of the iData research methodology is a built-in philosophy of quality control and continuing improvement is integral to the iData philosophy.

Step 9: Customer Feedback and Market Monitoring iData philosophy of continuous improvement requires that reports and consulting projects be monitored after release for customer feedback and market accuracy.

Click Here to Read More About Our Methodology