| List of Figures |

| Figure 1‑1: Infusion Therapy Device Market Share Ranking by Segment, U.S., 2022 |

5 |

| Figure 1‑2: Companies Researched in This Report |

6 |

| Figure 1‑3: Factors Impacting the Infusion Therapy Device Market by Segment, U.S. |

7 |

| Figure 1‑4: Recent Events in the Infusion Therapy Device Market, U.S., 2019 – 2023 |

8 |

| Figure 1‑5: Infusion Therapy Device Markets Covered (1 of 5) |

9 |

| Figure 1‑6: Infusion Therapy Device Markets Covered (2 of 5) |

10 |

| Figure 1‑7: Infusion Therapy Device Markets Covered (3 of 5) |

11 |

| Figure 1‑8: Infusion Therapy Device Markets Covered (4 of 5) |

12 |

| Figure 1‑9: Infusion Therapy Device Markets Covered (5 of 5) |

13 |

| Figure 1‑10: Key Report Updates |

14 |

| Figure 1‑11: Version History |

15 |

| Figure 2‑1: Infusion Therapy Device Market by Segment, Worst Case Scenario, U.S., 2019 – 2029 (US$M) |

32 |

| Figure 2‑2: Infusion Therapy Device Market by Segment, Base Case Scenario, U.S., 2019 – 2029 (US$M) |

33 |

| Figure 2‑3: Infusion Therapy Device Market by Segment, Best Case Scenario, U.S., 2019 – 2029 (US$M) |

34 |

| Figure 4‑1: Large-Volume Infusion Pumps by Company |

51 |

| Figure 4‑2: Intravenous Sets by Company (1 of 2) |

53 |

| Figure 4‑3: Intravenous Sets by Company (2 of 2) |

54 |

| Figure 4‑4: Needleless Connectors by Company |

57 |

| Figure 4‑5: Stopcocks by Company |

59 |

| Figure 4‑6: Intravenous Filters by Company |

60 |

| Figure 4‑7: Blood Transfusion Sets by Company |

61 |

| Figure 4‑8: Class 1 Device Recall Baxter Spectrum IQ |

62 |

| Figure 4‑9: Class 1 Device Recall Baxter SIGMA Spectrum |

62 |

| Figure 4‑10: Class 1 Device Recall Spectrum IQ Infusion System with Dose IQ Safety Software |

62 |

| Figure 4‑11: Class 2 Device Recall Spectrum IQInfusion Pump |

63 |

| Figure 4‑12: Class 2 Device Recall SIGMA Spectrum Infusion Pump |

63 |

| Figure 4‑13: Class 1 Device Recall Spectrum IQ |

63 |

| Figure 4‑14: Class 1 Device Recall Baxter SIGMA Spectrum Infusion Pump |

63 |

| Figure 4‑15: Class 2 Device Recall Baxter SIGMA Spectrum Infusion Pump |

64 |

| Figure 4‑16: Class 2 Device Recall B. Braun |

64 |

| Figure 4‑17: Class 2 Device Recall Infusomat Space Volumetric Pump Administration Set |

64 |

| Figure 4‑18: Class 1 Device Recall Infusomat Space Volumetric Infusion Pump Administration Set |

65 |

| Figure 4‑19: Class 2 Device Recall Alaris PC Unit |

65 |

| Figure 4‑20: Class 1 Device Recall Alaris Infusion Pump Module |

65 |

| Figure 4‑21: Class 1 Device Recall Alaris Pump Module |

65 |

| Figure 4‑22: Class 1 Device Recall Alaris Pump Module |

66 |

| Figure 4‑23: Class 1 Device Recall Alaris Pump |

66 |

| Figure 4‑24: Class 1 Device Recall BD Alaris Pump Module |

66 |

| Figure 4‑25: Class 1 Device Recall BD Alaris System PC Unit |

67 |

| Figure 4‑26: Class 1 Device Recall Alaris System PC Unit |

67 |

| Figure 4‑27: Class 1 Device Recall Alaris Infusion Pump System |

67 |

| Figure 4‑28: Class 2 Device Recall BD Alaris" System |

67 |

| Figure 4‑29: Class 2 Device Recall Alaris Pump Module |

68 |

| Figure 4‑30: Class 2 Device Recall Alaris Syringe Module |

68 |

| Figure 4‑31: Class 2 Device Recall Alaris PCA Module |

68 |

| Figure 4‑32: Class 1 Device Recall CareFusion Alaris Pump |

69 |

| Figure 4‑33: Class 2 Device Recall Plum 360 Infusion System with MedNet/Smart Card Plug n Play Module |

69 |

| Figure 4‑34: Class 1 Device Recall Medfusion Model 4000 Pump |

69 |

| Figure 4‑35: Class 2 Device Recall Medfusion Model 4000 Syringe Infusion Pump |

70 |

| Figure 4‑36: Class 2 Device Recall Clearlink System ContinuFlo Administration Sets |

71 |

| Figure 4‑37: Class 2 Device Recall Infusomat Space Volumetric Pump Administration Set |

71 |

| Figure 4‑38: Class 1 Device Recall Infusomat Space Volumetric Infusion Pump Administration Set |

71 |

| Figure 4‑39: Class 2 Device Recall BD Extension Set SMALLBORE Tubing with 2 SmartSite VALVES |

72 |

| Figure 4‑40: Class 2 Device Recall BD SmartSite 'Y' Extension Set 2 NeedleFree Valves |

72 |

| Figure 4‑41: Class 2 Device Recall BD Extension Set SMALLBORE Tubing SmartSite VALVE |

72 |

| Figure 4‑42: Class 2 Device Recall BD Gravity IV Set 3port Closed Manifold Back Check Valve 3 NeedleFree Ysites |

73 |

| Figure 4‑43: Class 2 Device Recall MaxPlus Bi Fuse Extension Set with 2 Clear Needleless Connectors |

73 |

| Figure 4‑44: Class 2 Device Recall BD Alaris PCEA Administration Set |

73 |

| Figure 4‑45: Class 2 Device Recall MaxZero |

74 |

| Figure 4‑46: Class 1 Device Recall SmartSite Syringe Administration Set |

74 |

| Figure 4‑47: Class 2 Device Recall Plum 360 Infusion System |

74 |

| Figure 4‑48: Class 2 Device Recall Sapphire Primary 1.2 Micron Filter Set Microbore Plum Microbore Infusion Sets with Inline Filter |

74 |

| Figure 4‑49: Class 2 Device Recall ONELINK Needlefree IV Connector |

75 |

| Figure 4‑50: Class 2 Device Recall MicroClave Clear Neutral Connector |

75 |

| Figure 4‑51: Class 2 Device Recall BD SmartSite |

75 |

| Figure 4‑52: Class 2 Device Recall ONELINK Needlefree IV Connector |

76 |

| Figure 4‑53: Class 2 Device Recall Argon Medical Devices Stopcocks |

77 |

| Figure 4‑54: Class 2 Device Recall BD Connecta Stopcocks |

77 |

| Figure 4‑55: Class 2 Device Recall IV Administration Set |

78 |

| Figure 4‑56: Class 2 Device Recall NAMIC Stopcocks |

78 |

| Figure 4‑57: Class 2 Device Recall Infusion Stopcock |

78 |

| Figure 4‑58: Class 2 Device Recall Medex stopcocks and manifolds |

78 |

| Figure 4‑59: Class 1 Device Recall Fresh Whole Blood Transfusion Set |

79 |

| Figure 4‑60: Class 1 Device Recall Low Titer Type O FWB Transfusion Set |

79 |

| Figure 4‑61: Hepatic Artery Infusion Pump Chemotherapy with Floxuridine and Dexamethasone in Combination with Systemic Chemotherapy for Patients with Colorectal Cancer Metastatic to the Liver |

81 |

| Figure 4‑62: Patient Outcomes After Hepatic Artery Infusion Pump Placement |

81 |

| Figure 4‑63: Evaluate Real-World Use of Next Generation Infusion Pumps to Administer Remodulin (EVOLVE) |

82 |

| Figure 4‑64: ElastoMeric Infusion Pumps for Hospital AntibioTICs (EMPHATIC) |

82 |

| Figure 4‑65: Prometra Post-Approval Study |

82 |

| Figure 4‑66: Hepatic Arterial Infusion Pump Chemotherapy Combined with Systemic Chemotherapy (PUMP-IT) |

83 |

| Figure 4‑67: Treatment of (IDA) by (FPC) Delivered via Infusion Pump in Patients Receiving Home Infusion Therapy |

83 |

| Figure 4‑68: An Observational Study to Evaluate BD PureHub™ Disinfecting Cap Use on Needle-Free Connectors |

84 |

| Figure 4‑69: Blood Transfusion in Patients with Lung Cancer |

85 |

| Figure 4‑70: Effect of Indication Based Blood Product Transfusion in Patients Undergoing Major Oncological Surgery |

85 |

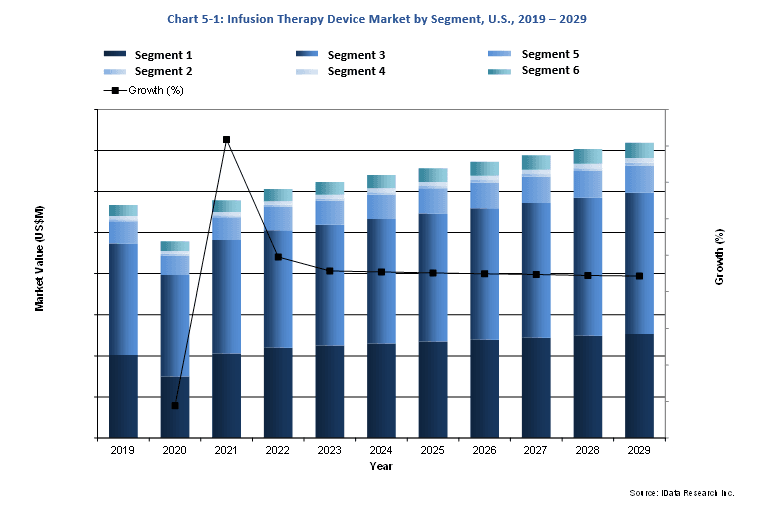

| Figure 5‑1: Infusion Therapy Device Market by Segment, U.S., 2019 – 2029 (US$M) |

90 |

| Figure 5‑2: Leading Competitors, Infusion Therapy Device Market, U.S., 2022 |

101 |

| Figure 5‑3: SWOT Analysis, Avanos Medical |

117 |

| Figure 5‑4: SWOT Analysis, B. Braun |

118 |

| Figure 5‑5: SWOT Analysis, Baxter |

119 |

| Figure 5‑6: SWOT Analysis, Becton Dickinson |

120 |

| Figure 5‑7: SWOT Analysis, Belmont Medical |

121 |

| Figure 5‑8: SWOT Analysis, CODAN |

122 |

| Figure 5‑9: SWOT Analysis, Fresenius |

123 |

| Figure 5‑10: SWOT Analysis, GVS Group |

124 |

| Figure 5‑11: SWOT Analysis, ICU Medical |

125 |

| Figure 5‑12: SWOT Analysis, Vygon |

126 |

| Figure 6‑1: Infusion Pump Market by Segment, U.S., 2019 – 2029 (US$M) |

130 |

| Figure 6‑2: Total Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

133 |

| Figure 6‑3: Large-Volume Infusion Pump Market by Care Setting, U.S., 2019 – 2029 (US$M) |

135 |

| Figure 6‑4: Hospital Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

137 |

| Figure 6‑5: Specialty Clinics Care Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

138 |

| Figure 6‑6: Ambulatory Surgical Center Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

139 |

| Figure 6‑7: Home Care Setting Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

140 |

| Figure 6‑8: Large-Volume Infusion Pump Market by Modularity, U.S., 2019 – 2029 (US$M) |

142 |

| Figure 6‑9: Modular Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

143 |

| Figure 6‑10: Non-Modular Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

144 |

| Figure 6‑11: Large-Volume Infusion Pump Market by MRI Compatibility, U.S., 2019 – 2029 (US$M) |

146 |

| Figure 6‑12: MRI-Compatible Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

147 |

| Figure 6‑13: Non-MRI-Compatible Large-Volume Infusion Pump Market, U.S., 2019 – 2029 |

148 |

| Figure 6‑14: Total Syringe Infusion Pump Market, U.S., 2019 – 2029 |

150 |

| Figure 6‑15: Syringe Infusion Pump Market by Care Setting, U.S., 2019 – 2029 (US$M) |

152 |

| Figure 6‑16: Hospital Syringe Infusion Pump Market, U.S., 2019 – 2029 |

153 |

| Figure 6‑17: Specialty Clinics Care Syringe Infusion Pump Market, U.S., 2019 – 2029 |

154 |

| Figure 6‑18: Ambulatory Surgical Center Syringe Infusion Pump Market, U.S., 2019 – 2029 |

155 |

| Figure 6‑19: Home Care Setting Syringe Infusion Pump Market, U.S., 2019 – 2029 |

156 |

| Figure 6‑20: Syringe Infusion Pump Market by Modularity, U.S., 2019 – 2029 (US$M) |

158 |

| Figure 6‑21: Modular Syringe Infusion Pump Market, U.S., 2019 – 2029 |

159 |

| Figure 6‑22: Non-Modular Syringe Infusion Pump Market, U.S., 2019 – 2029 |

160 |

| Figure 6‑23: Total Patient-Controlled Analgesia Infusion Pump Market, U.S., 2019 – 2029 |

162 |

| Figure 6‑24: Patient-Controlled Analgesia Infusion Pump Market by Care Setting, U.S., 2019 – 2029 (US$M) |

164 |

| Figure 6‑25: Hospital Patient-Controlled Analgesia Infusion Pump Market, U.S., 2019 – 2029 |

165 |

| Figure 6‑26: Specialty Clinics Patient-Controlled Analgesia Infusion Pump Market, U.S., 2019 – 2029 |

166 |

| Figure 6‑27: Ambulatory Surgical Center Patient-Controlled Analgesia Infusion Pump Market, U.S., 2019 – 2029 |

167 |

| Figure 6‑28: Home Care Setting Patient-Controlled Analgesia Infusion Pump Market, U.S., 2019 – 2029 |

168 |

| Figure 6‑29: Total Electronic Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

169 |

| Figure 6‑30: Electronic Ambulatory Infusion Pump Market by Care Setting, U.S., 2019 – 2029 (US$M) |

171 |

| Figure 6‑31: Hospital Electronic Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

172 |

| Figure 6‑32: Specialty Clinics Electronic Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

173 |

| Figure 6‑33: Ambulatory Surgical Center Electronic Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

174 |

| Figure 6‑34: Home Care Setting Electronic Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

175 |

| Figure 6‑35: Total Disposable Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

176 |

| Figure 6‑36: Disposable Ambulatory Infusion Pump Market by Type, U.S., 2019 – 2029 (US$M) |

177 |

| Figure 6‑37: Disposable Ambulatory Non-Pain Infusion Pump Market, U.S., 2019 – 2029 |

178 |

| Figure 6‑38: Disposable Ambulatory Pain Infusion Pump Market by Type, U.S., 2019 – 2029 (US$M) |

179 |

| Figure 6‑39: Total Disposable Ambulatory Pain Infusion Pump Market, U.S., 2019 – 2029 |

180 |

| Figure 6‑40: Surgical Post-Operative Disposable Ambulatory Pain Infusion Pump Market, U.S., 2019 – 2029 |

181 |

| Figure 6‑41: Peripheral Nerve Block Disposable Ambulatory Pain Infusion Pump Market, U.S., 2019 – 2029 |

182 |

| Figure 6‑42: Disposable Ambulatory Infusion Pump Market by Care Setting, U.S., 2019 – 2029 (US$M) |

184 |

| Figure 6‑43: Hospital Disposable Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

185 |

| Figure 6‑44: Specialty Clinics Disposable Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

186 |

| Figure 6‑45: Ambulatory Surgical Center Disposable Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

187 |

| Figure 6‑46: Home Care Setting Disposable Ambulatory Infusion Pump Market, U.S., 2019 – 2029 |

188 |

| Figure 6‑47: Leading Competitors, Infusion Pump Market, U.S., 2022 |

199 |

| Figure 7‑1: Intravenous Set Market by Device Type, U.S., 2019 – 2029 (US$M) |

203 |

| Figure 7‑2: Intravenous Set Market by Material, U.S., 2019 – 2029 (US$M) |

205 |

| Figure 7‑3: Total Pump Set Market, U.S., 2019 – 2029 |

208 |

| Figure 7‑4: Pump Set Market by Device Type, U.S., 2019 – 2029 (US$M) |

209 |

| Figure 7‑5: Dedicated Pump Set Market by Application, U.S., 2019 – 2029 (US$M) |

211 |

| Figure 7‑6: Total Dedicated Pump Set Market, U.S., 2019 – 2029 |

211 |

| Figure 7‑7: General Ward Dedicated Pump Set Market, U.S., 2019 – 2029 |

212 |

| Figure 7‑8: Burette Dedicated Pump Set Market, U.S., 2019 – 2029 |

213 |

| Figure 7‑9: Oncology Dedicated Pump Set Market, U.S., 2019 – 2029 |

214 |

| Figure 7‑10: Total Parenteral Nutrition Dedicated Pump Set Market, U.S., 2019 – 2029 |

215 |

| Figure 7‑11: Non-Dedicated Pump Set Market, U.S., 2019 – 2029 |

216 |

| Figure 7‑12: Pump Set Market by Light Protection, U.S., 2019 – 2029 (US$M) |

217 |

| Figure 7‑13: Light-Protected Pump Set Market, U.S., 2019 – 2029 |

218 |

| Figure 7‑14: Non-Light-Protected Pump Set Market, U.S., 2019 – 2029 |

219 |

| Figure 7‑15: Pump Set Market by Patient Age, U.S., 2019 – 2029 (US$M) |

220 |

| Figure 7‑16: Pediatric and Neonatal Pump Set Market, U.S., 2019 – 2029 |

221 |

| Figure 7‑17: Adult Pump Set Market, U.S., 2019 – 2029 |

222 |

| Figure 7‑18: Pump Set Market by Care Setting, U.S., 2019 – 2029 (US$M) |

223 |

| Figure 7‑19: Hospital Pump Set Market, U.S., 2019 – 2029 |

224 |

| Figure 7‑20: Specialty Clinics Pump Set Market, U.S., 2019 – 2029 |

225 |

| Figure 7‑21: Ambulatory Surgical Center Pump Set Market, U.S., 2019 – 2029 |

226 |

| Figure 7‑22: Home Care Setting Pump Set Market, U.S., 2019 – 2029 |

227 |

| Figure 7‑23: Total Gravity Set Market, U.S., 2019 – 2029 |

228 |

| Figure 7‑24: Gravity Set Market by Application, U.S., 2019 – 2029 (US$M) |

229 |

| Figure 7‑25: General Ward Gravity Set Market, U.S., 2019 – 2029 |

230 |

| Figure 7‑26: General Ward Set Market by Y-Site, U.S., 2019 – 2029 (US$M) |

231 |

| Figure 7‑27: General Ward Gravity Set Market by Needle-Free Access Port, U.S., 2019 – 2029 (US$M) |

232 |

| Figure 7‑28: General Ward Gravity Set with Y-Site Market, U.S., 2019 – 2029 |

233 |

| Figure 7‑29: General Ward Gravity Set with Y-Site with Needle-Free Access Port Market, U.S., 2019 – 2029 |

234 |

| Figure 7‑30: General Ward Gravity Set with Y-Site without Needle-Free Access Port Market, U.S., 2019 – 2029 |

235 |

| Figure 7‑31: General Ward Gravity Set without Y-Site Market, U.S., 2019 – 2029 |

236 |

| Figure 7‑32: General Ward Gravity Set Market by Filter, U.S., 2019 – 2029 (US$M) |

237 |

| Figure 7‑33: General Ward Gravity Set with Filter Market, U.S., 2019 – 2029 |

238 |

| Figure 7‑34: General Ward Gravity Set without Filter Market, U.S., 2019 – 2029 |

239 |

| Figure 7‑35: General Ward Gravity Set Market by Stopcock, U.S., 2019 – 2029 (US$M) |

240 |

| Figure 7‑36: General Ward Gravity Set with Stopcock Market, U.S., 2019 – 2029 |

241 |

| Figure 7‑37: General Ward Gravity Set without Stopcock Market, U.S., 2019 – 2029 |

242 |

| Figure 7‑38: General Ward Gravity Set Market by Flow Control, U.S., 2019 – 2029 (US$M) |

243 |

| Figure 7‑39: General Ward Gravity Set with Flow Control Market, U.S., 2019 – 2029 |

244 |

| Figure 7‑40: General Ward Gravity Set without Flow Control Market, U.S., 2019 – 2029 |

245 |

| Figure 7‑41: Burette Gravity Set Market, U.S., 2019 – 2029 |

246 |

| Figure 7‑42: Oncology Gravity Set Market, U.S., 2019 – 2029 |

247 |

| Figure 7‑43: Gravity Set Market by Care Setting, U.S., 2019 – 2029 (US$M) |

248 |

| Figure 7‑44: Hospital Gravity Set Market, U.S., 2019 – 2029 |

249 |

| Figure 7‑45: Specialty Clinics Gravity Set Market, U.S., 2019 – 2029 |

250 |

| Figure 7‑46: Ambulatory Surgical Center Gravity Set Market, U.S., 2019 – 2029 |

251 |

| Figure 7‑47: Home Care Setting Gravity Set Market, U.S., 2019 – 2029 |

252 |

| Figure 7‑48: Total Secondary Set Market, U.S., 2019 – 2029 |

253 |

| Figure 7‑49: Secondary Set Market by Care Setting, U.S., 2019 – 2029 |

254 |

| Figure 7‑50: Hospital Secondary Set Market, U.S., 2019 – 2029 |

255 |

| Figure 7‑51: Specialty Clinics Secondary Set Market, U.S., 2019 – 2029 |

256 |

| Figure 7‑52: Ambulatory Surgical Center Secondary Set Market, U.S., 2019 – 2029 |

257 |

| Figure 7‑53: Home Care Setting Secondary Set Market, U.S., 2019 – 2029 |

258 |

| Figure 7‑54: Total Extension Set Market, U.S., 2019 – 2029 |

260 |

| Figure 7‑55: Extension Set Market by Configuration, U.S., 2019 – 2029 (US$M) |

261 |

| Figure 7‑56: Standard Extension Set Market, U.S., 2019 – 2029 |

262 |

| Figure 7‑57: Multi-Way Extension Set Market, U.S., 2019 – 2029 |

263 |

| Figure 7‑58: Extension Set Market by IV Filter, U.S., 2019 – 2029 (US$M) |

265 |

| Figure 7‑59: Extension Set with Built-in IV Filter Market, U.S., 2019 – 2029 |

266 |

| Figure 7‑60: Extension Set without Built-in IV Filter Market, U.S., 2019 – 2029 |

267 |

| Figure 7‑61: Extension Set Market by Stopcock, U.S., 2019 – 2029 (US$M) |

268 |

| Figure 7‑62: Extension Set with Built-in Stopcock Market, U.S., 2019 – 2029 |

269 |

| Figure 7‑63: Extension Set without Built-in Stopcock Market, U.S., 2019 – 2029 |

270 |

| Figure 7‑64: Extension Set Market by Flow Control, U.S., 2019 – 2029 (US$M) |

272 |

| Figure 7‑65: Extension Set with Flow Control Market, U.S., 2019 – 2029 |

273 |

| Figure 7‑66: Extension Set without Flow Control Market, U.S., 2019 – 2029 |

274 |

| Figure 7‑67: Extension Set Market by Care Setting, U.S., 2019 – 2029 (US$M) |

275 |

| Figure 7‑68: Hospital Extension Set Market, U.S., 2019 – 2029 |

276 |

| Figure 7‑69: Specialty Clinics Extension Set Market, U.S., 2019 – 2029 |

277 |

| Figure 7‑70: Ambulatory Surgical Center Extension Set Market, U.S., 2019 – 2029 |

278 |

| Figure 7‑71: Home Care Setting Extension Set Market, U.S., 2019 – 2029 |

279 |

| Figure 7‑72: DEHP IV Set Market, U.S., 2019 – 2029 |

280 |

| Figure 7‑73: Non-DEHP IV Set Market, U.S., 2019 – 2029 |

281 |

| Figure 7‑74: Leading Competitors, Intravenous Set Market, U.S., 2022 |

287 |

| Figure 8‑1: Needleless Connector Market by Valve Type, U.S., 2019 – 2029 (US$M) |

291 |

| Figure 8‑2: Needleless Connector Market by Device Type, U.S., 2019 – 2029 (US$M) |

293 |

| Figure 8‑3: Needleless Connector Market by Antimicrobial Coating, U.S., 2019 – 2029 (US$M) |

295 |

| Figure 8‑4: Needleless Connector Market by Care Setting, U.S., 2019 – 2029 (US$M) |

297 |

| Figure 8‑5: Total Needleless Connector Market, U.S., 2019 – 2029 |

299 |

| Figure 8‑6: Split Septum & Blunt Cannula Needleless Connector Market, U.S., 2019 – 2029 |

301 |

| Figure 8‑7: Mechanical Valve Needleless Connector Market by Device Type, U.S., 2019 – 2029 (US$M) |

303 |

| Figure 8‑8: Total Mechanical Valve Needleless Connector Market, U.S., 2019 – 2029 |

304 |

| Figure 8‑9: Negative Displacement Mechanical Valve Needleless Connector Market, U.S., 2019 – 2029 |

305 |

| Figure 8‑10: Positive Displacement Mechanical Valve Needleless Connector Market, U.S., 2019 – 2029 |

306 |

| Figure 8‑11: Neutral Displacement Mechanical Valve Needleless Connector Market, U.S., 2019 – 2029 |

307 |

| Figure 8‑12: Anti-Reflux Neutral Displacement Mechanical Valve Needleless Connector Market, U.S., 2019 – 2029 |

308 |

| Figure 8‑13: Standalone Needleless Connector Market, U.S., 2019 – 2029 |

310 |

| Figure 8‑14: Integrated Needleless Connector Market, U.S., 2019 – 2029 |

311 |

| Figure 8‑15: Needleless Connector Market by Antimicrobial Coating, U.S., 2019 – 2029 (US$M) |

313 |

| Figure 8‑16: Antimicrobial Needleless Connector Market, U.S., 2019 – 2029 |

314 |

| Figure 8‑17: Conventional Needleless Connector Market, U.S., 2019 – 2029 |

315 |

| Figure 8‑18: Needleless Connector Market by Care Setting, U.S., 2019 – 2029 (US$M) |

316 |

| Figure 8‑19: Hospital Needleless Connector Market, U.S., 2019 – 2029 |

317 |

| Figure 8‑20: Specialty Clinics Needleless Connector Market, U.S., 2019 – 2029 |

318 |

| Figure 8‑21: Ambulatory Surgical Center Needleless Connector Market, U.S., 2019 – 2029 |

320 |

| Figure 8‑22: Home Care Setting Needleless Connector Market, U.S., 2019 – 2029 |

321 |

| Figure 8‑23: Leading Competitors, Needleless Connector Market, U.S., 2022 |

326 |

| Figure 9‑1: Stopcock Market by Flow Type, U.S., 2019 – 2029 (US$M) |

330 |

| Figure 9‑2: Stopcock Market by Care Setting, U.S., 2019 – 2029 (US$M) |

332 |

| Figure 9‑3: Total Stopcock Market, U.S., 2019 – 2029 |

334 |

| Figure 9‑4: One-Way Stopcock Market, U.S., 2019 – 2029 |

336 |

| Figure 9‑5: Two-Way Stopcock Market, U.S., 2019 – 2029 |

337 |

| Figure 9‑6: Three-Way Stopcock Market, U.S., 2019 – 2029 |

338 |

| Figure 9‑7: Four-Way Stopcock Market, U.S., 2019 – 2029 |

339 |

| Figure 9‑8: Stopcock Market by Care Setting, U.S., 2019 – 2029 (US$M) |

341 |

| Figure 9‑9: Hospital Stopcock Market, U.S., 2019 – 2029 |

342 |

| Figure 9‑10: Specialty Clinics Stopcock Market, U.S., 2019 – 2029 |

343 |

| Figure 9‑11: Ambulatory Surgical Center Stopcock Market, U.S., 2019 – 2029 |

344 |

| Figure 9‑12: Home Care Setting Stopcock Market, U.S., 2019 – 2029 |

345 |

| Figure 9‑13: Leading Competitors, Stopcock Market, U.S., 2022 |

350 |

| Figure 10‑1: Intravenous Filter Market by Care Setting, U.S., 2019 – 2029 (US$M) |

354 |

| Figure 10‑2: Total Intravenous Filter Market, U.S., 2019 – 2029 |

357 |

| Figure 10‑3: Hospital Intravenous Filter Market, U.S., 2019 – 2029 |

360 |

| Figure 10‑4: Specialty Clinics Intravenous Filter Market, U.S., 2019 – 2029 |

362 |

| Figure 10‑5: Ambulatory Surgical Center Intravenous Filter Market, U.S., 2019 – 2029 |

364 |

| Figure 10‑6: Home Care Setting Intravenous Filter Market, U.S., 2019 – 2029 |

366 |

| Figure 10‑7: Leading Competitors, Intravenous Filter Market, U.S., 2022 |

370 |

| Figure 11‑1: Blood Transfusion Device Market by Chamber Type, U.S., 2019 – 2029 (US$M) |

374 |

| Figure 11‑2: Blood Transfusion Device Market by Care Setting, U.S., 2019 – 2029 (US$M) |

376 |

| Figure 11‑3: Total Blood Transfusion Device Market, U.S., 2019 – 2029 |

378 |

| Figure 11‑4: Single-Chamber Blood Transfusion Device Market, U.S., 2019 – 2029 |

380 |

| Figure 11‑5: Dual-Chamber Blood Transfusion Device Market, U.S., 2019 – 2029 |

381 |

| Figure 11‑6: Hospital Blood Transfusion Device Market, U.S., 2019 – 2029 |

384 |

| Figure 11‑7: Specialty Clinics Blood Transfusion Device Market, U.S., 2019 – 2029 |

386 |

| Figure 11‑8 Other Blood Transfusion Device Market, U.S., 2019 – 2029 |

388 |

| Figure 11‑9: Leading Competitors, Blood Transfusion Device Market, U.S., 2022 |

392 |