Product Description

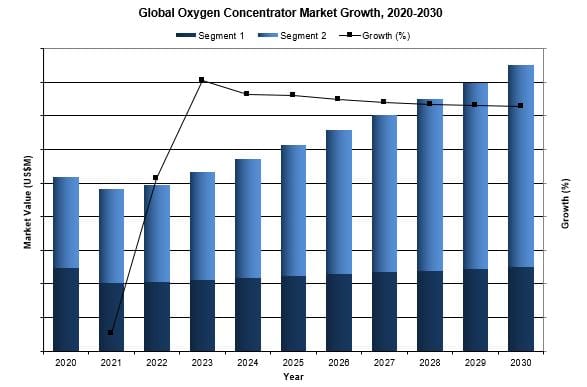

Overall, the global oxygen concentrator market was valued at nearly $1.1 billion in 2023. This is expected to increase over the forecast period to reach $1.7 billion.

The majority of the global oxygen concentrator market share was controlled by CAIRE, Philips Healthcare, and Inogen.

Oxygen therapy devices are used to treat patients who are no longer able to receive adequate volumes of oxygen through the breathing of natural air and who require higher concentrations of oxygen. This global market research spans over 70 countries and includes stationary oxygen concentrators and portable oxygen concentrators.

MARKET DATA INCLUDED

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- COVID-19 Impact Analysis

- Market Drivers & Limiters

- Market Forecasts Until 2030, and Historical Data to 2020

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

GLOBAL OXYGEN CONCENTRATOR MARKET INSIGHTS

GLOBAL OXYGEN CONCENTRATOR MARKET SHARE INSIGHTS

CAIRE, a global leader in medical oxygen equipment, is renowned for its AirSep™ portable concentrators and FAA-approved units. Its product range includes the NewLife® and VisionAire™ 5 stationary concentrators, Freestyle®Comfort® and Eclipse 5® portable units, and SeQual™ transportable concentrators. CAIRE is also noted for its military-grade oxygen solutions and AirSep™ stationary units.

Philips Healthcare stands out for its lightweight SimplyGo™ concentrator, capable of both continuous and pulse flow, and the EverFlo™ and Millennium M10™ systems, emphasizing mobility and high-capacity oxygen delivery. However, in January 2024, Philips announced it would discontinue these lines to focus on consumables.

Inogen specializes in portable oxygen concentrators, notably the Rove 6™ System and Inogen One G4®, part of the lightweight One G® series. Despite competition from established brands, Inogen’s cost-effective, energy-efficient products position it strongly in the oxygen therapy market.

Market Segmentation Summary

- Stationary Oxygen Concentrators

- Portable Oxygen Concentrators

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, U.K.) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Mongolia, Malaysia, Myanmar, New Zealand, Philippines, Pakistan, Singapore, South Korea, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2023 |

| Forecast | 2024-2030 |

| Historical Data | 2020-2023 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | COVID19 Impact, Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |