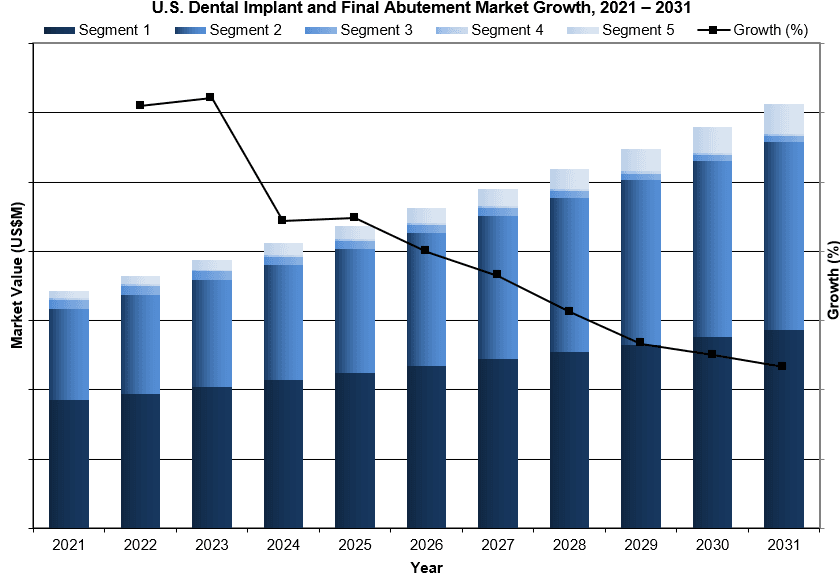

The dental implant and final abutment market in the US reached approximately $2.1 billion in 2024 and is expected to grow and reach nearly $3.1 billion in 2031.

Market drivers include the aging population, demand for high-precision solutions, and tools like CBCT scanners, surgical guides, and CAD/CAM abutments that improve outcomes. However, recession pressures and downward pricing in the value segment may limit growth.

Let’s break down who’s leading the pack, and why.

Find growth niches in minutes, not months.

Explore quick, actionable insights from the select markets.

Table of Contents

➜ Why Are Dental Implants Booming in the US?

➜ Who Are the Top US Dental Implant Market Leaders?

↳ Straumann: Innovation Across Premium & Value

↳ Envista: Dual-Brand Strategy

↳ Dentsply Sirona: Premium Tools & Surgical Guides

↳ Henry Schein/BioHorizons: Value-Focused Growth

↳ ZimVie: Premium Portfolio Remains Strong

↳ Osstem Implant (HIOSSEN): Asia’s Challenger

↳ MegaGen: South Korea to US Expansion

➜ What Makes These Dental Implant Companies Stand Out?

➜ Dental Implant Market Overview & Future Outlook

➜ Get a Complimentary US Dental Implant & Final Abutment Market Report Summary

Key Takeaways

- US dental implant & abutment market: $2.1B in 2024, projected to $3.1B by 2031 (5.9% CAGR).

- Straumann leads at ~35% market share, leveraging Neodent and iEXCEL digital solutions.

- Envista’s dual-brand model targets both premium and value segments via Nobel Biocare and Implant Direct.

- Dentsply Sirona excels in surgical guide integration and CAD/CAM abutments.

- Henry Schein, ZimVie, HIOSSEN, and MegaGen round out the top 7, each with unique strengths.

- Key innovations: CBCT, guided surgery, CAD/CAM, and regenerative materials are fueling market evolution.

- Economic uncertainty and price competition may moderate growth, but digital solutions and training will continue to drive adoption.

Why Are Dental Implants Booming in the US?

(Note: to see the full graph, download our 2025 – 2031 Dental Implant and Final Abutment Market Report)

The U.S. dental implant market is surging, propelled by precision tech like CAD/CAM and CBCT that enhance fit, aesthetics, and clinical outcomes. One-stage protocols promoted by major players are streamlining workflows and reducing patient visits.

- Integration of CAD/CAM Technology: The widespread adoption of computer-aided design and manufacturing (CAD/CAM) is enabling highly customized abutments that offer superior fit, function, and aesthetics, driving clinical adoption across general and specialist practices.

- Rise of One-Stage Procedures: Straumann and other leaders are promoting one-stage or transgingival healing protocols, which reduce patient visits and streamline surgical workflows, making implant placement more efficient and attractive to both providers and patients.

- Precision Technology: CBCT imaging, surgical guides, and CAD/CAM customization help optimize implant alignment, fit, aesthetics, and clinical success.

- Economic Forces: Despite price sensitivity and value brand penetration, willingness to invest in reliable implants persists, unless broader economic fears take hold.

Despite growing value-brand competition, demand remains strong as clinicians and patients continue to prioritize quality and predictability.

Who Are the Top US Dental Implant Market Leaders?

Straumann: Innovation Across Premium & Value

![]()

Straumann leads U.S. market share by offering a robust ecosystem that spans both premium and value implant segments, anchored by its flagship brand and Neodent.

Its recently launched iEXCEL implant system enhances compatibility with a single connection platform across all designs, simplifying treatment planning for clinicians.

Straumann also pioneered transgingival healing implants, enabling one-stage procedures that reduce chair time. With a broad portfolio of CAD/CAM solutions, biomaterials, and regenerative products, the company continues to position itself as a “one-stop shop” for implant dentistry.

Envista: Dual‑Brand Strategy with Nobel Biocare & Implant Direct

![]()

Envista ranks second in the U.S. dental implant market, leveraging a dual-brand strategy that serves both ends of the market: Nobel Biocare for premium and Implant Direct for value.

NobelActive® and TiUltra™ implants are favored by specialists for complex cases, backed by Nobel’s longstanding clinical reputation.

Meanwhile, Implant Direct appeals to cost-conscious GPs with pre-packaged kits like Simply Iconic™, offering efficiency without sacrificing clinical quality—strengthening Envista’s cross-segment market hold.

Dentsply Sirona: Strength in Guides & Abutments

![]()

Dentsply Sirona, the third-largest player, stands out for its CAD/CAM-milled abutments, surgical guides, and broad implant systems like Astra Tech, MIS Implants, and DS OmniTaper®.

These systems are supported by software-driven workflows, empowering clinicians with more accurate planning and placement.

The integration of digital dentistry tools and continued investment in prosthetic compatibility makes Dentsply a go-to for practices seeking precision and flexibility.

Henry Schein/BioHorizons: Value Brand with Premium Reach

![]()

Henry Schein, through BioHorizons, has carved out a dominant share in the value segment while maintaining strong revenue through higher-priced offerings.

Its hybrid pricing model is supported by regenerative materials, Medtronic INFUSE® grafts, and surgical guide systems, broadening its appeal in both general and specialist practices.

Heavy investment in training and clinician education strengthens loyalty and helps grow adoption across all practice sizes.

ZimVie: Premium Products, Competitive Market

![]()

A spin-off from Zimmer Biomet, ZimVie maintains a premium-focused lineup including T3®, OSSEOTITE®, and Trabecular Metal™ implants.

The launch of TSX® implants, Azure™ abutments, and the GenTek® restorative line reflect efforts to modernize and streamline its portfolio.

Despite solid offerings, ZimVie faces stiff competition in the crowded premium segment and is working to differentiate through expanded restorative workflows.

Osstem Implant (HIOSSEN): Asia’s Growing US Influence

![]()

HIOSSEN, the North American arm of Osstem Implant, continues to gain traction in the value segment by offering tapered implants, guided surgery kits, and CAD/CAM services tailored for general dentists.

Its U.S. manufacturing hub in Pennsylvania boosts domestic production and strengthens its operational agility.

By combining affordable pricing with strong clinical outcomes, HIOSSEN is fast becoming a formidable force among value implant providers.

MegaGen: South Korea’s US Challenger

![]()

South Korean manufacturer MegaGen is building U.S. presence through innovative products like AnyRidge®, MiNi™, and Ari®, distributed via Integrated Dental Systems (IDS).

With an emphasis on advanced surface treatments, narrow-diameter implants, and continued clinician education, MegaGen is carving out a unique space among forward-looking providers.

Its growth strategy is focused on innovation access and partnerships, particularly with younger or digitally enabled practices.

What Makes These Dental Implant Companies Stand Out?

| Competitor | What Sets Them Apart |

| Straumann | Premium-to-value spectrum, iEXCEL, global scale |

| Envista | Twin approach: Nobel Biocare (high-end) and Implant Direct (value) |

| Dentsply Sirona | Full digital workflow—CAD/CAM abutments, guides, software |

| Henry Schein | Value brand + training support and bone graft integration |

| ZimVie | Custom abutment solutions, premium-material focus |

| HIOSSEN | U.S. production, Asia-backed R&D |

| MegaGen | Educational growth, niche innovation |

Dental Implant Market Overview & Future Outlook

- U.S. market revaluation: ~$2.1bn in 2024 ➝ ~$3.1bn by 2031 (5.9% CAGR).

- Wider industry: U.S. dental implants alone hit ~$1.4bn in 2023, with strong growth potential (~11.4% CAGR through 2032).

- Global trends: Digital workflows and CAD/CAM are reshaping implant delivery across markets.

Outlook: As digital planning, imaging, and materials evolve, premium providers will diversify into value segments. Partnerships, acquisitions, and global integration will drive competition. Economic conditions and reimbursement changes may impact procedure volume, but technological progress will continue to improve success rates and clinic profitability.

Turn market painpoints into opportunities

Explore how procedure trends and competitor positioning create clear openings for industry experts in the market.