Product Description

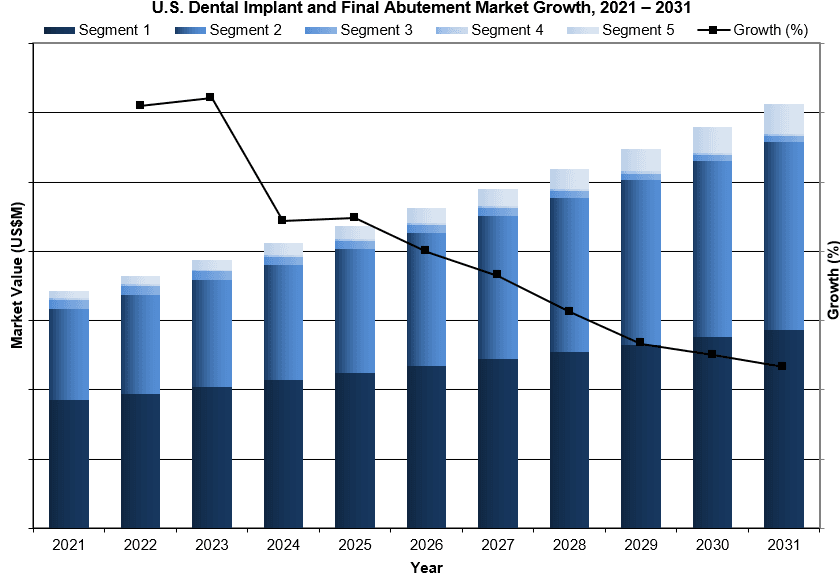

The U.S. dental implant and final abutment market was valued at nearly $2.1 billion in 2024. This is expected to increase over the forecast period at a CAGR of 5.9% to reach nearly $3.1 billion in 2031.

The full report suite on the U.S. market for dental implants and final abutments includes dental implants, final abutments, instrument kits, treatment planning software and surgical guides.

The dental implant and final abutment market has experienced significant growth, driven by technological advancements that enhance the precision and efficiency of dental procedures. Innovations in advanced imaging tools, such as cone beam computed tomography (CBCT) scanners, allow for more accurate assessments of the patient’s jaw, helping dentists evaluate bone density and structure to plan successful implant surgeries. Computer-guided surgery software further advanced implant placement techniques by enabling the precise placement of implants with the aid of surgical guides. Furthermore, the integration of computer-aided design/manufacturing (CAD/CAM) technology has led to the production of customized final abutments, offering more stable and aesthetically pleasing restorations. As these technologies continue to evolve, the surgical guide market is expected to experience significant growth, driving the overall market.

DATA TYPES INCLUDED IN THIS REPORT

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2021

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

U.S. DENTAL IMPLANT MARKET TRENDS

Complete edentulism (tooth loss) is much more prevalent among people over 65 years of age; therefore, as the population ages, the need for dental implants and final abutments will increase. According to the Population Reference Bureau (PRB) aging report, the U.S. population is experiencing rapid aging. The number of individuals aged 65 and older is projected to increase from 58 million in 2022 to 82 million in 2050. On a global scale, nearly 23% of those over 60 experience complete tooth loss compared to only 7% in individuals aged 20 years or older. The aging population is set to impact the dental implant and final abutment market significantly, driving demand for implant and abutment procedures.

U.S. DENTAL IMPLANT MARKET SHARE INSIGHTS

- Straumann Group was the strongest competitor in the dental implant and final abutment market in 2024, sustaining benefits from its brand name recognition and a proven track record of developing best-in-class dental implants. A key pillar of the Group’s market leadership is its multi-brand strategy. Its portfolio includes Anthogyr, Medentika, Neodent, NUVO and Straumann. Straumann has traditionally led the premium implant market, with its success driven by a comprehensive range of dental implant products that consistently perform well across various applications. Straumann’s subsidiary, Neodent, holds the top position in the value implant segment, reinforcing the Group’s dominant position in the dental implant market. This strong foundation ensures that the Group remains well placed to maintain its leadership in the dental implant industry. A continuous emphasis on mergers and acquisitions has greatly strengthened the company profile.

- Envista secured the second-leading position in the dental implant and final abutment market due to its subsidiaries, Nobel Biocare and Implant Direct. Nobel Biocare, the pioneer of the All-on-4® digital workflow, was in close competition to Straumann in the premium implant segment. One of Nobel Biocare’s many strengths is the breadth of its product offerings for every patient type. The company’s position in the market is largely reflective of its success within dental implant fixtures. Implant Direct was a direct competitor to Neodent in the value implant segment, using medical-grade titanium alloy to manufacture implants solely in the United States. In 2024, Implant Direct announced the launch of the Simply IconicTM implant system, offering a wide range of implant diameters and two prosthetic platforms. The company’s implant systems are marketed as an all-in-one packaging deal, containing the implant, abutment, transfer, cover screw and other related products. Envista’s diverse portfolio of all segments of the dental implant and final abutment market will continue to accelerate the company’s growth.

- Dentsply Sirona was the third-leading competitor in the dental implant and final abutment market, offering a comprehensive line of premium implants and materials, including its own CAD/CAM milled abutments. The company is also the leader in the surgical guide and treatment planning software segments. Dentsply Sirona’s product portfolio is heavily diversified and is well prepared to capture growth across all segments in the dental implant and final abutment markets, with the company recently launching the DS OmniTaper® Implant System in May 2023. Dentsply Sirona’s subsidiary, MIS Implants, has further enabled the company to capture the demand of price-sensitive consumers in the value segment

MARKET SEGMENTATION SUMMARY

- Dental Implants Market – Further Segmented Into:

- Type: Premium, Value, Discount, and Minis.

- Final Abutment Market – Further Segmented Into:

- Fabrication Type: Stock, custom cast, and CAD/CAM abutments.

- Dental Implant Instrument Kit Market

- Treatment Planning Software – Further Segmented Into:

- Market Type: Treatment Planning Software and Treatment Planning Software Maintenance Fees.

- Surgical Guide Market

- Type: Traditional, Third-Party, and In-Houses.

RESEARCH SCOPE SUMMARY

| Report Attribute | Details |

|---|---|

| Regions | United States |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Historical Data | 2021-2023 |

| Quantitative Data | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Data | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |