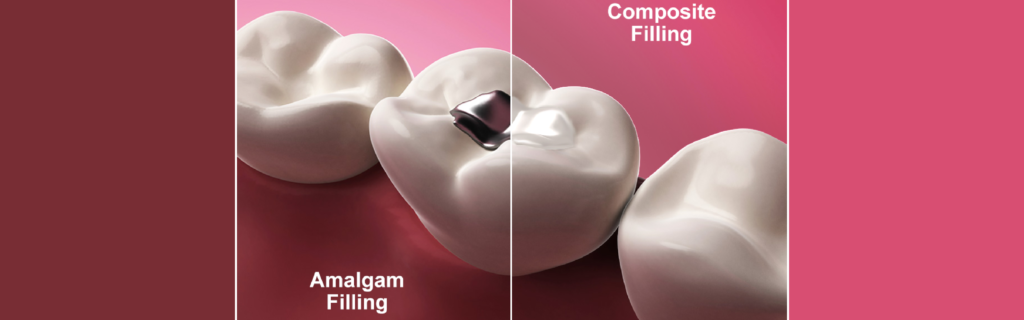

According to the latest market study by iData Research, the US dental amalgam market size was valued at over $89 million by 2020. Amalgam was the first filling material ever used in dentistry and is essentially an alloy of different metals, primarily mercury (~50%) and silver (~22-32%).

Amalgam material was the predominant restorative material up until the 1970s when composites began their rise in the direct restorative material market within the dental industry. Amalgam is fairly affordable and easy-to-use for the dentists and has been tested and proven durable through history.

However, the popularity of amalgam fillings has been challenged by the increasing efficacy of alternative materials, mercury toxicity, and aesthetic concerns. Thus, the amalgam market is expected to continue to decline over the following years, in spite of the procedural fluctuations brought by COVID19.

Dental Amalgam Market Insights

The level of mercury contained in amalgam initially raised significant concerns about the negative health effects of these restorations, inflicting a notable decline in sales, to the point where countries such as Sweden, Denmark, and Norway banned the use of this material in dental fillings in 2008. However, the FDA in the U.S. concluded in 2009 that there was no evidence supporting any negative health effects that can be associated with dental amalgams.

More recently, the United Nations Minamata convention, effective in 2017, which aims to protect human and environmental health from mercury exposure, also exerts downward pressure on the amalgam market. However, despite the availability of superior products, and the mercury concerns, amalgam is the direct restorative material of choice for uninsured and low-income groups, because of its low cost and durability.

In recent years, the use of amalgam has partially recovered from controversial claims regarding the potential health hazards posed by mercury. However, the measurable aesthetic advantage of teeth-colored composites has been sufficient for this segment to decline over the last few years. In addition, composites have stolen much of the appeal from amalgam, as those fillings require less natural tooth removal.

The recent procedural analysis also indicates that amalgam procedures remained at a relatively high volume in 2019. This was largely due to the fact that amalgam was considerably less expensive and lasts longer than its alternatives. Aside from the less costly nature of the material, usage of amalgam restoratives is simplified by their self-sealing tendencies, whereas alternative materials typically require the recruitment of some bonding agent. The decline in procedures will persist as the aging population of dentists is displaced by younger graduates who have become accustomed to using alternative materials.

Dental Amalgam Market Share Analysis

By 2020, over 70% of the dental amalgam market in the US was dominated by three major players: Kerr, Dentsply Sirona, and Ivoclar Vivadent. The rest of the amalgam market share was highly segmented and controlled by multiple established market players, including SDI Limited and DenMat Holdings, LLC.

Kerr secured its top position in the US dental amalgam market through the sales of its amalgam products, such as Tytin® and Contour™. Tytin® was the first single composition spherical product in the American market and used a ternary system composed of silver, tin, and copper. The product contains more silver and less copper than Contour™, making it more durable as a result.

Dentsply Sirona secured the second leading position in the US amalgam market with three product lines: Dispersalloy®, Megalloy®, and Unison®. Dispersalloy® has been used for over 30 years in American dental offices, and it is the workhorse of the company in the alloy restoratives category. Megalloy® is a spherical amalgam that has high copper content allowing for high strength. Unison® is a similar product that demonstrates earlier-than-average compressive strength, lowering the likelihood of marginal failure.

Impact of COVID19 on the US Market

As the dental market is on its path to recovery, the amalgam fillings will be one of the primary choices for the lower-income groups across the United States. Household income remains the best predictor of dental market recovery because the households in the US are the primary payers of dental procedures.

Therefore, the dental amalgam market is expected to gain some traction during COVID-19 due to a decrease in household incomes, job loss, and subsequent loss of insurance coverage. However, the US market is expected to reach its pre-COVID19 levels in late 2020 and will continue declining as the popularity of alternative restorative products continues to rise.

Dental Amalgam Market Growth and Forecast

The amalgam direct restoratives market is expected to continue declining as a result of market pressure coming from the composite, glass ionomer, and resin-modified glass ionomer markets. In spite of the availability of these superior products, the amalgam restorative material will continue to be favored for its low cost and longevity among the uninsured and low-income groups.

Register to receive a free Dental Materials Market Report Suite for US 2020-2026 synopsis

A recent market study indicates that the US dental amalgam market size will reach a valuation of around $74.4 million in 2026 while decreasing steadily at a cumulative rate of -2.8% over the years. Overall, it is expected that this decline won’t be a major limiter of the total Dental Materials market in the US.