| Figure 1‑1: Vascular Access Devices and Accessories Market Share Ranking by Segment, U.S., 2024 (1 of 4) |

| Figure 1‑2: Vascular Access Devices and Accessories Market Share Ranking by Segment, U.S., 2024 (2 of 4) |

| Figure 1‑3: Vascular Access Devices and Accessories Market Share Ranking by Segment, U.S., 2024 (3 of 4) |

| Figure 1‑4: Vascular Access Devices and Accessories Market Share Ranking by Segment, U.S., 2024 (4 of 4) |

| Figure 1‑5: Companies Researched in This Report (1 of 2) |

| Figure 1‑6: Companies Researched in This Report (2 of 2) |

| Figure 1‑7: Factors Impacting the Vascular Access Devices and Accessories Market by Segment, U.S. (1 of 4) |

| Figure 1‑8: Factors Impacting the Vascular Access Devices and Accessories Market by Segment, U.S. (2 of 4) |

| Figure 1‑9: Factors Impacting the Vascular Access Devices and Accessories Market by Segment, U.S. (3 of 4) |

| Figure 1‑10: Factors Impacting the Vascular Access Devices and Accessories Market by Segment, U.S. (4 of 4) |

| Figure 1‑11: Recent Events in the Vascular Access Devices and Accessories Market, U.S., 2021 – 2025 (1 of 2) |

| Figure 1‑12: Recent Events in the Vascular Access Devices and Accessories Market, U.S., 2021 – 2025 (2 of 2) |

| Figure 1‑13: Vascular Access Devices and Accessories Procedure Segmentation (1 of 4) |

| Figure 1‑14: Vascular Access Devices and Accessories Procedure Segmentation (2 of 4) |

| Figure 1‑15: Vascular Access Devices and Accessories Procedure Segmentation (3 of 4) |

| Figure 1‑16: Vascular Access Devices and Accessories Procedure Segmentation (4 of 4) |

| Figure 1‑17: Procedure Codes Investigated |

| Figure 1‑18: Vascular Access Devices and Accessories Market Segmentation (1 of 8) |

| Figure 1‑19: Vascular Access Devices and Accessories Market Segmentation (2 of 8) |

| Figure 1‑20: Vascular Access Devices and Accessories Market Segmentation (3 of 8) |

| Figure 1‑21: Vascular Access Devices and Accessories Market Segmentation (4 of 8) |

| Figure 1‑22: Vascular Access Devices and Accessories Market Segmentation (5 of 8) |

| Figure 1‑23: Vascular Access Devices and Accessories Market Segmentation (6 of 8) |

| Figure 1‑24: Vascular Access Devices and Accessories Market Segmentation (7 of 8) |

| Figure 1‑25: Vascular Access Devices and Accessories Market Segmentation (8 of 8) |

| Figure 1‑26: Key Report Updates (1 of 2) |

| Figure 1‑27: Key Report Updates (2 of 2) |

| Figure 1‑28: Version History |

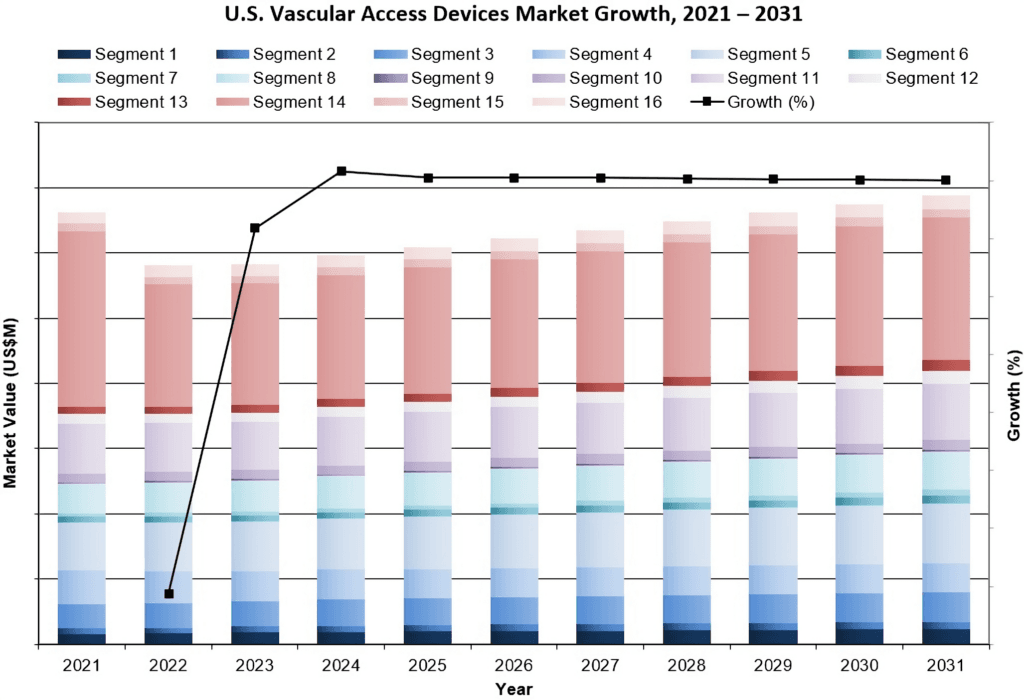

| Figure 3‑1: Vascular Access Devices and Accessories Market by Segment, U.S., 2021 – 2031 (US$M) (1 of 3) |

| Figure 3‑2: Vascular Access Devices and Accessories Market by Segment, U.S., 2021 – 2031 (US$M) (2 of 3) |

| Figure 3‑3: Vascular Access Devices and Accessories Market by Segment, U.S., 2021 – 2031 (US$M) (3 of 3) |

| Figure 3‑4: Leading Competitors, Vascular Access Devices and Accessories Market, U.S., 2024 (1 of 2) |

| Figure 3‑5: Leading Competitors, Vascular Access Devices and Accessories Market, U.S., 2024 (2 of 2) |

| Figure 4‑1: Procedure Codes Investigated, U.S., 2024 |

| Figure 4‑2: Vascular Access Procedure Numbers, U.S., 2021 – 2031 (1 of 2) |

| Figure 4‑3: Vascular Access Procedure Numbers, U.S., 2021 – 2031 (2 of 2) |

| Figure 4‑4: Implantable Port Insertion Procedures by Material, U.S., 2021 – 2031 |

| Figure 4‑5: Implantable Port Insertion Procedures by Valve Type, U.S., 2021 – 2031 |

| Figure 4‑6: Implantable Port Insertion Procedures by Power-Injectability, U.S., 2021 – 2031 |

| Figure 4‑7: Implantable Port Insertion Procedures by Location, U.S., 2021 – 2031 |

| Figure 4‑8: Implantable Port Insertion Procedures by Setting, U.S., 2021 – 2031 |

| Figure 4‑9: Implantable Port Insertion Procedures by Patient Age Group, U.S., 2021 – 2031 |

| Figure 4‑10: Implantable Port Insertion Procedures by Operator, U.S., 2021 – 2031 |

| Figure 4‑11: Port Needle Insertion Procedures by Setting, U.S., 2021 – 2031 |

| Figure 4‑12: Central Venous Catheter Insertion Procedures by Device Type, U.S., 2021 – 2031 |

| Figure 4‑13: Central Venous Catheter Insertion Procedures by Insertion Site U.S., 2021 – 2031 |

| Figure 4‑14: CVC Insertion Procedures by Imaging Technique, U.S., 2021 – 2031 |

| Figure 4‑15: Central Venous Catheter Insertion Procedures by Patient Type, U.S., 2021 – 2031 |

| Figure 4‑16: Peripherally Inserted Central Catheter Insertion Procedures by Power-Injectability, U.S., 2021 – 2031 |

| Figure 4‑17: Peripherally Inserted Central Catheter Insertion Procedures by Patient Age Group, U.S., 2021 – 2031 |

| Figure 4‑18: Peripherally Inserted Central Catheter Insertion Procedures by Operator, U.S., 2021 – 2031 |

| Figure 4‑19: Peripherally Inserted Central Catheter Insertion Procedures by Setting, U.S., 2021 – 2031 |

| Figure 4‑20: Mean Peripheral Intravenous Catheters Used per Procedure, U.S., 2021 – 2031 |

| Figure 4‑21: Peripheral Intravenous Catheter Insertion Procedures by Setting, U.S., 2021 – 2031 |

| Figure 4‑22: Peripheral Intravenous Catheter Insertion Procedures by Device Type, U.S., 2021 – 2031 |

| Figure 4‑23: Peripheral Intravenous Catheter Insertion Procedures by Insertion Site, U.S., 2021 – 2031 |

| Figure 4‑24: Peripheral Intravenous Catheter Insertion Procedures by Visualization Method, U.S., 2021 – 2031 |

| Figure 4‑25: Midline Placement Procedures by Device Type, U.S., 2021 – 2031 |

| Figure 4‑26: Midline Placement Procedures by Power-Injectability, U.S., 2021 – 2031 |

| Figure 4‑27: Extended Dwell Placement Procedures, U.S., 2021 – 2031 |

| Figure 4‑28: Dialysis Catheter Placement Procedures by Device Type, U.S., 2021 – 2031 |

| Figure 4‑29: Vascular Access Catheters Placed Using Ultrasound Guidance, U.S., 2021 – 2031 |

| Figure 4‑30: Vascular Access Catheters Placed Using Ultrasound Guidance by Operator, U.S., 2021 – 2031 |

| Figure 4‑31: PIVCs Placed Using Vein Visualization, U.S., 2021 – 2031 |

| Figure 4‑32: Vascular Access Catheters Placed Using Tip-Placement Devices by Catheter Type, U.S., 2021 – 2031 |

| Figure 4‑33: Vascular Access Catheters Placed Using Tip-Placement Device by Operator, U.S., 2021 – 2031 |

| Figure 5‑1: Implantable Port Market by Material, U.S., 2021 – 2031 (US$M) |

| Figure 5‑2: Implantable Port Market by Valve Type, U.S., 2021 – 2031 (US$M) |

| Figure 5‑3: Implantable Port Market by Device Properties, U.S., 2021 – 2031 (US$M) |

| Figure 5‑4: Total Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑5: Total Full Plastic Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑6: Full Plastic Implantable Port Market by Lumen Number, U.S., 2021 – 2031 (US$M) |

| Figure 5‑7: Single-Lumen Full Plastic Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑8: Double-Lumen Full Plastic Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑9: Full Plastic Implantable Port Market by Power-Injectability, U.S., 2021 – 2031 (US$M) |

| Figure 5‑10: Power-Injectable Full Plastic Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑11: Non-Power-Injectable Full Plastic Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑12: Total Full Titanium Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑13: Full Titanium Implantable Port Market by Lumen Number, U.S., 2021 – 2031 (US$M) |

| Figure 5‑14: Single-Lumen Full Titanium Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑15: Double-Lumen Full Titanium Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑16: Full Titanium Implantable Port Market by Power-Injectability, U.S., 2021 – 2031 (US$M) |

| Figure 5‑17: Power-Injectable Full Titanium Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑18: Non-Power-Injectable Full Titanium Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑19: Total Hybrid Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑20: Hybrid Implantable Port Market by Lumen Number, U.S., 2021 – 2031 (US$M) |

| Figure 5‑21: Single-Lumen Hybrid Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑22: Double-Lumen Hybrid Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑23: Hybrid Implantable Port Market by Power-Injectability, U.S., 2021 – 2031 (US$M) |

| Figure 5‑24: Power-Injectable Hybrid Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑25: Non-Power-Injectable Hybrid Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑26: Valved Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑27: Non-Valved Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑28: Antithrombogenic Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑29: Conventional Implantable Port Market, U.S., 2021 – 2031 |

| Figure 5‑30: Leading Competitors, Implantable Port Market, U.S., 2024 |

| Figure 6‑1: Port Needle Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 6‑2: Total Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑3: Acute Care Port Needle Market by Device Type, U.S., 2021 – 2031 |

| Figure 6‑4: Acute Care Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑5: Acute Care Conventional Port Needle Market by Y-Site, U.S., 2021 – 2031 |

| Figure 6‑6: Acute Care Conventional Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑7: Acute Care Conventional Port Needle with Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑8: Acute Care Conventional Port Needle without Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑9: Acute Care Safety Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑10: Acute Care Safety Port Needle Market by Power-Injectability, U.S., 2021 – 2031 |

| Figure 6‑11: Acute Care Safety Power-Injectable Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑12: Acute Care Safety Non-Power-Injectable Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑13: Acute Care Safety Port Needle Market by Y-Site, U.S., 2021 – 2031 |

| Figure 6‑14: Acute Care Safety Port Needle with Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑15: Acute Care Safety Port Needle without Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑16: Acute Care Safety Port Needle Market by Needleless Connector, U.S., 2021 – 2031 |

| Figure 6‑17: Acute Care Safety Port Needle with Needleless Connector Market, U.S., 2021 – 2031 |

| Figure 6‑18: Acute Care Safety Port Needle without Needleless Connector Market, U.S., 2021 – 2031 |

| Figure 6‑19: Alternate Care Port Needle Market by Device Type, U.S., 2021 – 2031 |

| Figure 6‑20: Alternate Care Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑21: Alternate Care Conventional Port Needle Market by Y-Site, U.S., 2021 – 2031 |

| Figure 6‑22: Alternate Care Conventional Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑23: Alternate Care Conventional Port Needle with Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑24: Alternate Care Conventional Port Needle without Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑25: Alternate Care Safety Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑26: Alternate Care Safety Port Needle Market by Power-Injectability, U.S., 2021 – 2031 |

| Figure 6‑27: Alternate Care Safety Power-Injectable Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑28: Alternate Care Safety Non-Power-Injectable Port Needle Market, U.S., 2021 – 2031 |

| Figure 6‑29: Alternate Care Safety Port Needle Market by Y-Site, U.S., 2021 – 2031 |

| Figure 6‑30: Alternate Care Safety Port Needle with Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑31: Alternate Care Safety Port Needle without Y-Site Market, U.S., 2021 – 2031 |

| Figure 6‑32: Alternate Care Safety Port Needle Market by Needleless Connector, U.S., 2021 – 2031 |

| Figure 6‑33: Alternate Care Safety Port Needle with Needleless Connector Market, U.S., 2021 – 2031 |

| Figure 6‑34: Alternate Care Safety Port Needle without Needleless Connector Market, U.S., 2021 – 2031 |

| Figure 6‑35: Leading Competitors, Port Needle Market, U.S., 2024 |

| Figure 7‑1: Central Venous Catheter Market by Device Type, U.S., 2021 – 2031 (US$M) |

| Figure 7‑2: Total Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑3: Acute Central Venous Catheter Market by Device Type, U.S., 2021 – 2031 (US$M) |

| Figure 7‑4: Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑5: Conventional Acute Central Venous Catheter Market by Device Type, U.S., 2021 – 2031 |

| Figure 7‑6: Conventional Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑7: Single-Lumen Conventional Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑8: Multi-Lumen Conventional Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑9: Antimicrobial Acute Central Venous Catheter Market by Device Type, U.S., 2021 – 2031 |

| Figure 7‑10: Antimicrobial Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑11: Impregnated Antimicrobial Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑12: Coated Antimicrobial Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑13: Antimicrobial Acute Central Venous Catheter Market by Lumen Count, U.S., 2021 – 2031 |

| Figure 7‑14: Antimicrobial Acute Central Venous Catheter Market by Lumen Count, U.S., 2021 – 2031 |

| Figure 7‑15: Single-Lumen Antimicrobial Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑16: Multi-Lumen Antimicrobial Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑17: Acute Central Venous Catheter Market by Power-Injectability, U.S., 2021 – 2031 (US$M) |

| Figure 7‑18: Total Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑19: Power-Injectable Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑20: Non-Power-Injectable Acute Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑21: Total Chronic Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑22: Chronic Central Venous Catheter Market by Power-Injectability, U.S., 2021 – 2031 (US$M) |

| Figure 7‑23: Power-Injectable Chronic Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑24: Non-Power-Injectable Chronic Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑25: Chronic Central Venous Catheter Market by Device Type, U.S., 2021 – 2031 (US$M) |

| Figure 7‑26: Advanced Materials Chronic Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑27: Conventional Chronic Central Venous Catheter Market, U.S., 2021 – 2031 |

| Figure 7‑28: Leading Competitors, Central Venous Catheter Market, U.S., 2024 |

| Figure 8‑1: Peripherally Inserted Central Catheter Market by Tip-Placement Type, U.S., 2021–2031 (US$M) |

| Figure 8‑2: Peripherally Inserted Central Catheter Market by Care Setting, U.S., 2021 – 2031 (US$M) |

| Figure 8‑3: Peripherally Inserted Central Catheter Market by Valve Type, U.S., 2021 – 2031 (US$M) |

| Figure 8‑4: Peripherally Inserted Central Catheter Market by Kit Type, U.S., 2021 – 2031 (US$M) |

| Figure 8‑5: Total Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑6: Tip-Placement Peripherally Inserted Central Catheter Kit Market by Lumen Number, U.S., 2021 – 2031 (US$M) |

| Figure 8‑7: Tip-Placement Peripherally Inserted Central Catheter Kit Market, U.S., 2021 – 2031 |

| Figure 8‑8: Single-Lumen Tip-Placement Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑9: Double-Lumen Tip-Placement Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑10: Triple-Lumen Tip-Placement Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑11: Peripherally Inserted Central Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 8‑12: Tip-Placement Peripherally Inserted Central Catheter Kit Market, U.S., 2021 – 2031 |

| Figure 8‑13: Non-Power-Injectable Tip-Placement Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑14: Power-Injectable Tip-Placement Peripherally Inserted Central Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 8‑15: Power-Injectable Tip-Placement Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑16: Antimicrobial Power-Injectable Tip-Placement Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑17: Conventional Power-Injectable Tip-Placement Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑18: Non-Tip-Guidance Peripherally Inserted Central Catheter Kit Market by Lumen Number, U.S., 2021 – 2031 (US$M) |

| Figure 8‑19: Non-Tip-Guidance Peripherally Inserted Central Catheter Kit Market, U.S., 2021 – 2031 |

| Figure 8‑20: Single-Lumen Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑21: Double-Lumen Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑22: Triple-Lumen Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑23: Non-Tip-Guidance Peripherally Inserted Central Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 8‑24: Non-Tip-Guidance Peripherally Inserted Central Catheter Kit Market, U.S., 2021 – 2031 |

| Figure 8‑25: Non-Power-Injectable Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑26: Power-Injectable Non-Tip-Guidance Peripherally Inserted Central Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 8‑27: Power-Injectable Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑28: Antimicrobial Power-Injectable Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑29: Antithrombogenic Power-Injectable Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑30: Conventional Power-Injectable Non-Tip-Guidance Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑31: Hospital-Based Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑32: Non-Hospital-Based Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑33: Valved Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑34: Non-Valved Peripherally Inserted Central Catheter Market, U.S., 2021 – 2031 |

| Figure 8‑35: Long Guidewire Peripherally Inserted Central Catheter Kit Market, U.S., 2021 – 2031 |

| Figure 8‑36: Standard Peripherally Inserted Central Catheter Kit Market, U.S., 2021 – 2031 |

| Figure 8‑37: Peripherally Inserted Central Catheter Units Sold by Material, U.S., 2021 – 2031 |

| Figure 8‑38: Peripherally Inserted Central Catheter Units Sold by Material and Lumen, U.S., 2024 |

| Figure 8‑39: Peripherally Inserted Central Catheter Units Sold by Age and Material, U.S., 2024 |

| Figure 8‑40: Leading Competitors, Peripherally Inserted Central Catheter Market, U.S., 2024 |

| Figure 9‑1: Peripheral Intravenous Catheter Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 9‑2: Peripheral Intravenous Catheter Market by Setting, U.S., 2021 – 2031 (US$M) |

| Figure 9‑3: Total Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑4: Conventional Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑5: Safety Peripheral Intravenous Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 9‑6: Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑7: Blood Control Safety Peripheral Intravenous Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 9‑8: Blood Control Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑9: Integrated Blood Control Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑10: Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑11: Blood Control Safety Peripheral Intravenous Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 9‑12: Active Blood Control Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑13: Passive Blood Control Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑14: Non-Blood Control Safety Peripheral Intravenous Catheter Market by Type, U.S., 2021 – 2031 (US$M) |

| Figure 9‑15: Non-Blood Control Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑16: Non-Blood Control Active Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑17: Non-Blood Control Passive Safety Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑18: Acute Care Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑19: Alternate Care Peripheral Intravenous Catheter Market by Setting, U.S., 2021 – 2031 (US$M) |

| Figure 9‑20: Alternate Care Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑21: Home Care Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑22: Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑23: Peripheral Intravenous Catheter Market by Length, U.S., 2021 – 2031 |

| Figure 9‑24: Standard Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑25: Long Peripheral Intravenous Catheter Market, U.S., 2021 – 2031 |

| Figure 9‑26: Peripheral Intravenous Catheter Market by Insertion Site, U.S., 2021 – 2031 |

| Figure 9‑27: Peripheral Intravenous Catheter Units Sold by Insertion Technique, U.S., 2019 – 2029 |

| Figure 9‑28: Leading Competitors, Peripheral Intravenous Catheter Market, U.S., 2024 |

| Figure 10‑1: Midline Market by Insertion Method, U.S., 2021 – 2031 (US$M) |

| Figure 10‑2: Midline Market, U.S., 2021 – 2031 |

| Figure 10‑3: AST Midline Market, U.S., 2021 – 2031 |

| Figure 10‑4: MST Midline Market by Power Injectability, U.S., 2021 – 2031 |

| Figure 10‑5: MST Midline Market, U.S., 2021 – 2031 |

| Figure 10‑6: MST Midline Market by Power Injectability, U.S., 2021 – 2031 |

| Figure 10‑7: Total Power-Injectable MST Midline Market, U.S., 2021 – 2031 |

| Figure 10‑8: Long Power-Injectable MST Midline Market, U.S., 2021 – 2031 |

| Figure 10‑9: Short Power-Injectable MST Midline Market, U.S., 2021 – 2031 |

| Figure 10‑10: Non-Power-Injectable MST Midline Market, U.S., 2021 – 2031 |

| Figure 10‑11: Midline Market by Configuration, U.S., 2021 – 2031 |

| Figure 10‑12: Single-Lumen Midline Market, U.S., 2021 – 2031 |

| Figure 10‑13: Double-Lumen Midline Market, U.S., 2021 – 2031 |

| Figure 10‑14: Leading Competitors, Midline Market, U.S., 2024 |

| Figure 11‑1: Extended Dwell Catheter Market, U.S., 2021 – 2031 |

| Figure 11‑2: Leading Competitors, Extended Dwell Catheter Market, U.S., 2024 |

| Figure 12‑1: Dialysis Catheter Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 12‑2: Dialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑3: Hemodialysis Catheter Market by Dwell Time, U.S., 2021–2031 (US$M) |

| Figure 12‑4: Total Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑5: Long-Term Hemodialysis Catheter Market by Device Type, U.S., 2021 – 2031 (US$M) |

| Figure 12‑6: Total Long-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑7: Conventional Long-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑8: Anti-Microbial Material Long-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑9: Antithrombogenic Material Long-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑10: Long-Term Hemodialysis Catheter Market by Care Setting, U.S., 2021 – 2031 (US$M) |

| Figure 12‑11: In-Center Long-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑12: Home Care Long-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑13: Short-Term Hemodialysis Catheter Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 12‑14: Total Short-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑15: Power-Injectable Short-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑16: Non-Power-Injectable Short-Term Hemodialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑17: Peritoneal Dialysis Catheter Market, U.S., 2021 – 2031 |

| Figure 12‑18: Leading Competitors, Dialysis Catheter Market, U.S., 2024 |

| Figure 13‑1: Ultrasound Vascular Access Device and Accessory Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 13‑2: Cart-Based Ultrasound System Specialized for Vascular Access Market, U.S., 2021 – 2031 |

| Figure 13‑3: Hand-Carried and Portable Ultrasound System Specialized for Vascular Access Market, U.S., 2021 – 2031 |

| Figure 13‑4: Multi-Purpose Hand-Carried and Portable Ultrasound System Specialized for Vascular Access Market, U.S., 2021 – 2031 |

| Figure 13‑5: Leading Competitors, Ultrasound Vascular Access Device and Accessory Market, U.S., 2024 |

| Figure 14‑1: Vein Visualization Technology Market, U.S., 2021 – 2031 |

| Figure 14‑2: Leading Competitors, Vein Visualization Technology Market, U.S., 2024 |

| Figure 15‑1: Tip-Placement System and Accessory Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 15‑2: Tip-Placement System Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 15‑3: Total Tip-Placement System Market, U.S., 2021 – 2031 |

| Figure 15‑4: Standalone Tip-Placement System Market, U.S., 2021 – 2031 |

| Figure 15‑5: Integrated Tip-Placement System Market, U.S., 2021 – 2031 |

| Figure 15‑6: Disposable Tip-Placement Accessory Market, U.S., 2021 – 2031 |

| Figure 15‑7: Leading Competitors, Tip-Placement System and Accessory Market, U.S., 2024 |

| Figure 16‑1: Catheter Securement Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 16‑2: Catheter Securement Market, U.S., 2021 – 2031 |

| Figure 16‑3: Tape and Dressing Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 16‑4: Total Tape and Dressing Market, U.S., 2021 – 2031 |

| Figure 16‑5: Antimicrobial Tape and Dressing Market, U.S., 2021 – 2031 |

| Figure 16‑6: Standard Tape and Dressing Market, U.S., 2021 – 2031 |

| Figure 16‑7: Suture Market, U.S., 2021 – 2031 |

| Figure 16‑8: Manufactured Catheter Securement Device Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 16‑9: Total Manufactured Catheter Securement Device Market, U.S., 2021 – 2031 |

| Figure 16‑10: Mechanical Manufactured Catheter Securement Device Market, U.S., 2021 – 2031 |

| Figure 16‑11: Non-Mechanical Manufactured Catheter Securement Device Market, U.S., 2021 – 2031 |

| Figure 16‑12: Manufactured Catheter Securement Device Units Sold by Catheter Type, U.S., 2021 – 2031 |

| Figure 16‑13: Leading Competitors, Catheter Securement Market, U.S., 2024 |

| Figure 17‑1: Antibacterial Catheter Patch Market, U.S., 2021 – 2031 |

| Figure 17‑2: Leading Competitors, Antibacterial Catheter Patch Market, U.S., 2024 |

| Figure 18‑1: Catheter Cap Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 18‑2: Catheter Cap Market, U.S., 2021 – 2031 |

| Figure 18‑3: Standard Catheter Cap Market, U.S., 2021 – 2031 |

| Figure 18‑4: Dialysis Catheter Cap Market, U.S., 2021 – 2031 |

| Figure 18‑5: Leading Competitors, Catheter Cap Market, U.S., 2024 |

| Figure 19‑1: Syringe and Needle Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 19‑2: Syringe Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 19‑3: Total Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑4: Conventional Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑5: Sliding Sleeve Safety Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑6: Retractable Safety Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑7: Hinged Safety Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑8: Insulin Syringe Market by Usage, U.S., 2021 – 2031 (US$M) |

| Figure 19‑9: Total Insulin Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑10: Personal Insulin Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑11: Professional Insulin Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑12: Insulin Syringe Market by Device Type, U.S., 2021 – 2031 (US$M) |

| Figure 19‑13: Total Insulin Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑14: Safety Insulin Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑15: Non-Safety Insulin Syringe Market, U.S., 2021 – 2031 |

| Figure 19‑16: Needle Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 19‑17: Total Needle Market, U.S., 2021 – 2031 |

| Figure 19‑18: Conventional Needle Market, U.S., 2021 – 2031 |

| Figure 19‑19: Shielding Safety Needle Market, U.S., 2021 – 2031 |

| Figure 19‑20: Pivoting Needle Market, U.S., 2021 – 2031 |

| Figure 19‑21: Blunt Fill Needle Market, U.S., 2021 – 2031 |

| Figure 19‑22: Insulin Pen Needle Market by Segment, U.S., 2021 – 2031 (US$M) |

| Figure 19‑23: Total Insulin Pen Needle Market, U.S., 2021 – 2031 |

| Figure 19‑24: Safety Insulin Pen Needle Market, U.S., 2021 – 2031 |

| Figure 19‑25: Non-Safety Insulin Pen Needle Market, U.S., 2021 – 2031 |

| Figure 19‑26: Leading Competitors, Syringe and Needle Market, U.S., 2024 |

| Figure 20‑1: Arterial Catheter Market, U.S., 2021 – 2031 (US$M) |

| Figure 20‑2: Leading Competitors, Arterial Catheter Market, U.S., 2024 |

Becton Dickinson (BD) held the largest share of the U.S. vascular access devices (VADs) and accessories market in 2024, driven by its dominance in key segments like PIVCs and syringes and needles, which together made up about half the market’s total value. The company’s scale, established sales networks and deep GPO relationships enabled it to offer high-volume safety products at unmatched prices, creating a competitive barrier for smaller players. BD has expanded its portfolio through acquisitions and continues to act as a comprehensive solution provider for healthcare facilities. In the U.S., BD has invested heavily in syringe and needle production capacity, particularly in response to 2024 tariffs on Chinese imports. New U.S. production lines are expected to generate millions of units annually. In product development, BD has shifted its PICC focus from antimicrobial coatings to innovations that reduce thrombosis and withstand chemotherapy degradation.

Becton Dickinson (BD) held the largest share of the U.S. vascular access devices (VADs) and accessories market in 2024, driven by its dominance in key segments like PIVCs and syringes and needles, which together made up about half the market’s total value. The company’s scale, established sales networks and deep GPO relationships enabled it to offer high-volume safety products at unmatched prices, creating a competitive barrier for smaller players. BD has expanded its portfolio through acquisitions and continues to act as a comprehensive solution provider for healthcare facilities. In the U.S., BD has invested heavily in syringe and needle production capacity, particularly in response to 2024 tariffs on Chinese imports. New U.S. production lines are expected to generate millions of units annually. In product development, BD has shifted its PICC focus from antimicrobial coatings to innovations that reduce thrombosis and withstand chemotherapy degradation. Becton Dickinson (BD) held the largest share of the U.S. vascular access devices (VADs) and accessories market in 2024, driven by its dominance in key segments like PIVCs and syringes and needles, which together made up about half the market’s total value. The company’s scale, established sales networks and deep GPO relationships enabled it to offer high-volume safety products at unmatched prices, creating a competitive barrier for smaller players. BD has expanded its portfolio through acquisitions and continues to act as a comprehensive solution provider for healthcare facilities. In the U.S., BD has invested heavily in syringe and needle production capacity, particularly in response to 2024 tariffs on Chinese imports. New U.S. production lines are expected to generate millions of units annually. In product development, BD has shifted its PICC focus from antimicrobial coatings to innovations that reduce thrombosis and withstand chemotherapy degradation.

Becton Dickinson (BD) held the largest share of the U.S. vascular access devices (VADs) and accessories market in 2024, driven by its dominance in key segments like PIVCs and syringes and needles, which together made up about half the market’s total value. The company’s scale, established sales networks and deep GPO relationships enabled it to offer high-volume safety products at unmatched prices, creating a competitive barrier for smaller players. BD has expanded its portfolio through acquisitions and continues to act as a comprehensive solution provider for healthcare facilities. In the U.S., BD has invested heavily in syringe and needle production capacity, particularly in response to 2024 tariffs on Chinese imports. New U.S. production lines are expected to generate millions of units annually. In product development, BD has shifted its PICC focus from antimicrobial coatings to innovations that reduce thrombosis and withstand chemotherapy degradation.