Product Description

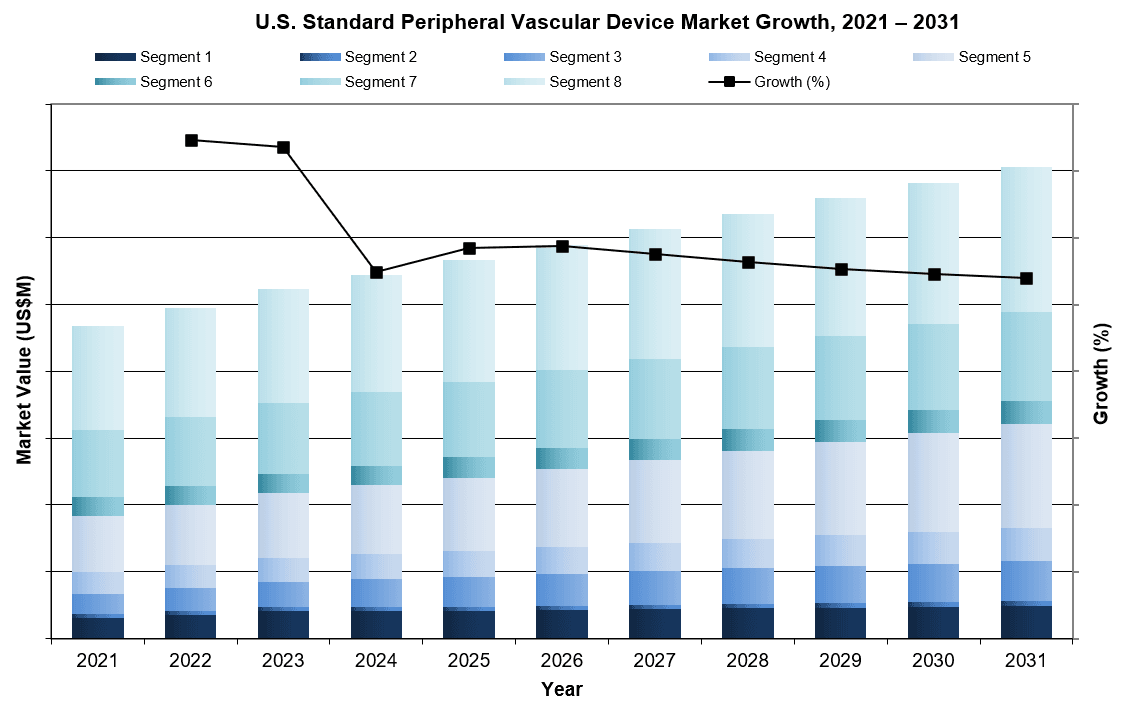

The U.S. standard peripheral vascular device market was valued at over $2.7 billion in 2024. This is expected to increase over the forecast period at a CAGR of 3.8% to reach over $3.5 billion.

This report suite on the U.S. market for peripheral vascular devices covers inferior vena cava filters (IVCFs) and retrieval devices, carotid shunts, transcarotid arterial revascularization (TCAR) flow reversal systems and stents, diagnostic and interventional catheters, diagnostic and interventional guidewires, introducer sheaths, vascular closure devices (VCDs) and transcatheter embolization devices.

MARKET REPORT DATA TYPES INCLUDED

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2021

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

U.S. STANDARD PERIPHERAL VASCULAR DEVICE MARKET TRENDS

A notable trend within the VCD market is the increasing adoption of non–invasive and extravascular closure technologies, driven by the growing shift toward radial and same-day discharge procedures. As peripheral interventions increasingly move into outpatient and OBL settings, there is heightened demand for closure devices that minimize complications, reduce patient recovery time and support faster ambulation.

U.S. STANDARD PERIPHERAL VASCULAR DEVICE MARKET SHARE INSIGHTS

- Terumo led the U.S. peripheral vascular device market in 2024, driven by strong sales in the guidewire and VCD segments. The company also held top positions in the diagnostic and interventional catheter and introducer sheath markets. Terumo dominated the hydrophilic guidewire segment with its Glidewire® line, featuring a kink-resistant nitinol core and a radiopaque tungsten jacket. Variants like the Glidewire® GT and Glidewire® Gold offer enhanced tip flexibility and visibility. To stay competitive, Terumo has lowered guidewire prices in select regions. The company secured its leadership in the U.S. VCD market following its 2016 acquisition of Angio-Seal™ and FemoSeal™ from St. Jude Medical, a divestiture prompted by antitrust concerns during Abbott’s acquisition of St. Jude.

- Boston Scientific held the second-leading position in the peripheral vascular market. Its 2019 acquisition of BTG for $7.4 billion significantly expanded its portfolio, making the company a leader in transcatheter embolization devices. Boston Scientific also gained FDA approval for its VICI® venous stent and continues to hold a notable share with its legacy Wallstent®. The company has increasingly focused on oncology devices and deep vein thrombosis treatment.

- Abbott Vascular held the third-largest share of the U.S. peripheral vascular device market in 2024, driven largely by its dominance in the large-bore VCD segment. The company led the overall VCD market with its suture-mediated systems, namely StarClose™, Perclose® and ProStar® XL, which seal arterial access sites using needles and knots. Abbott has steadily improved these devices to enhance stability, ease of use, and reduce inflammation. While it maintained a near-monopoly in large-bore invasive VCDs in 2024, its position is expected to weaken as new single-device closure solutions enter the market, though these alternatives have yet to gain significant traction.

U.S. STANDARD PERIPHERAL VASCULAR DEVICE MARKET SEGMENTATION SUMMARY

- Inferior Vena Cava Filter Market – Further Segmented Into:

- Device Type: IVCF, and IVCF Retrieval Device.

- Carotid Shunt

- Transcarotid Artery Revascularization (TCAR) – Further Segmented Into:

- Device Type: Transcarotid Bare-Metal Stent, and TCAR Neuroprotection System.

- Diagnostic & Interventional Catheter – Further Segmented Into:

- Device Type: Diagnostic Catheter, and Support Catheter.

- Diagnostic & Interventional Guidewire – Further Segmented Into:

- Device Type: Standard, and Hydrophilic.

- Introducer Sheath – Further Segmented Into:

- Device Type: Standard, and Guiding.

- Vascular Closure Device – Further Segmented Into:

- Device Type: Non-Invasive, and Invasive.

- Approach: Radial, and Femoral.

- Transcatheter Embolization – Further Segmented Into:

- Device Type: Particle, Coil, Liquid, and Plug.

- Approach: Radial, and Femoral.

RESEARCH SCOPE SUMMARY

| Report Attribute | Details |

|---|---|

| Region | United States |

| Base Year | 2024 |

| Forecast | 2025-2031 |

| Historical Data | 2021-2023 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.