Product Description

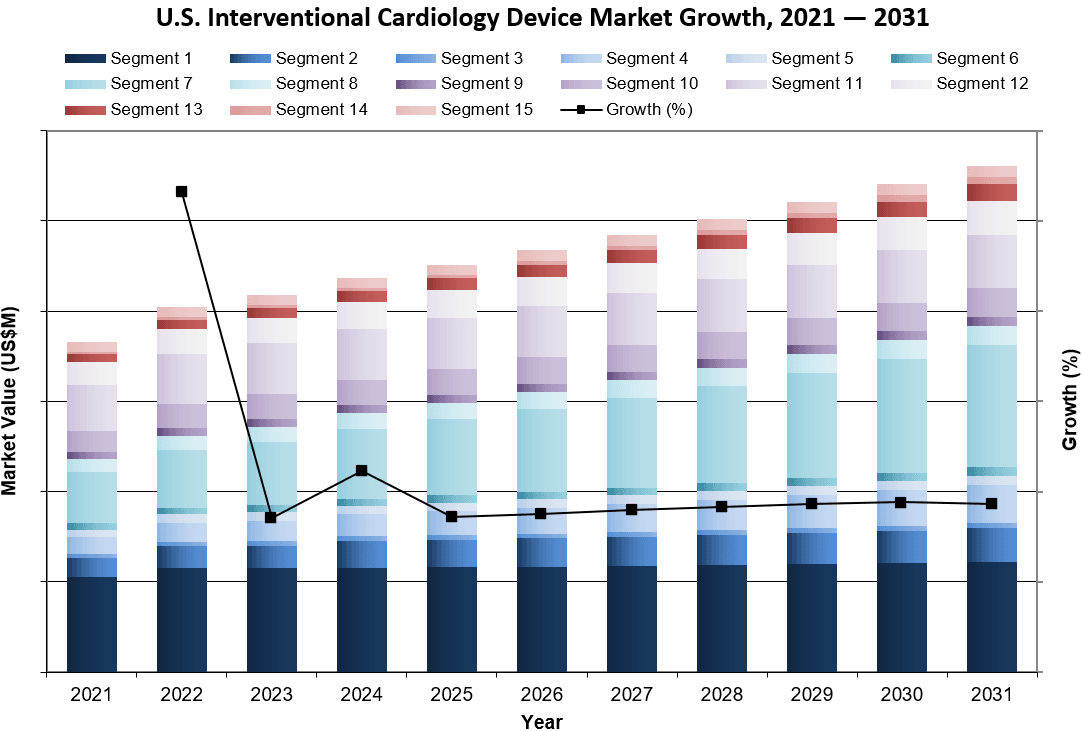

The U.S. interventional cardiology device market was valued at nearly $4.4 billion in 2024. This is expected to increase over the forecast period at a CAGR of 3.6% to reach over $5.6 billion.

This report suite on the U.S. market for interventional cardiology devices includes coronary stents, coronary balloon catheters, balloon-inflation devices, interventional coronary catheters, interventional coronary guidewires, coronary embolic protection devices (EPDs), coronary atherectomy and intravascular lithotripsy devices, coronary thrombectomy devices, coronary chronic total occlusion (CTO) systems, introducer sheaths, coronary vascular closure devices (VCDs), diagnostic coronary catheters and guidewires, coronary intravascular ultrasound (IVUS), coronary optical coherence tomography (OCT) catheters and hemostasis valves.

MARKET REPORT DATA TYPES INCLUDED

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2021

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

U.S. INTERVENTIONAL CARDIOLOGY DEVICE MARKET TRENDS

In the coming years, imaging technologies are set to become deeply integrated into interventional cardiology, shaping both diagnostic and procedural strategies. Tools such as OCT, IVUS and high-resolution CT will attract ongoing investment as physicians increasingly rely on their ability to deliver precise, real-time views of coronary structures and disease.

U.S. INTERVENTIONAL CARDIOLOGY DEVICE MARKET SHARE INSIGHTS

- Boston Scientific was the leading competitor in the U.S. interventional cardiology market in 2024, maintaining dominant positions in the coronary stent, coronary balloon catheter and coronary embolic protection device segments. The company’s market presence is expected to expand modestly with the introduction of its new coronary drug-coated balloon.

- Abbott ranked as the second-largest competitor in the interventional cardiology market in the U.S. in 2024, participating across a broad range of device segments and frequently holding top positions within each. The company faces no direct competition in the OCT segment, further reinforcing its market standing. Abbott is expected to maintain its overall market share in the coming years.

- ShockWave Medical ranked as the third-leading competitor in the interventional cardiology market in the U.S. in 2024. The company specializes in intravascular lithotripsy (IVL) technology, designed to treat calcified plaque in patients with peripheral vascular, coronary vascular and heart valve diseases worldwide. This technology has only been approved for the last four years but is continuing to see rapid expansion.

U.S. INTERVENTIONAL CARDIOLOGY DEVICE MARKET SEGMENTATION SUMMARY

- Coronary Stent Market – Further Segmented Into:

- Device Type: Bare-Metal Stent, Drug-Eluting Stent, Covered Stent, and Bifurcated Stent.

- Units by Size*: Diameter, and Length.

- Coronary Balloon Catheter – Further Segmented Into:

- Device Type: PTCA Balloon, and Specialty Balloon.

- Units by Classification*: Compliant, Semi-Compliant, and Non-Compliant.

- Units by Indication*: Pre-Dilation & Stent Placement, and Post-Dilation.

- Balloon-Inflation Device

- Interventional Coronary Catheter – Further Segmented Into:

- Device Type: Guiding Catheter, Extension Guide Catheter, and Micro-Catheter.

- Interventional Coronary Guidewire

- Coronary Embolic Protection Device

- Coronary Atherectomy Device – Further Segmented Into:

- Device Type: Mechanical Atherectomy, Laser Atherectomy, and Intravascular Lithotripsy (IVL).

- Coronary Thrombectomy

- Coronary Chronic Total Occlusion System – Further Segmented Into:

- Device Type: CTO Guidewire, CTO Catheter, and CTO Device.

- Introducer Sheath – Further Segmented Into:

- Device Type: Standard Introducer, and Micro-Introducer.

- By Approach: Femoral, and Radial.

- Coronary Vascular Closure Device – Further Segmented Into:

- Invasive VCD, and Non-Invasive VCD.

- Diagnostic Coronary Catheter & Guidewire – Further Segmented Into:

- Device Type: Diagnostic Catheter, Diagnostic Guidewire, and Fractional Flow Reserve Guidewire.

- Coronary Intravascular Ultrasound – Further Segmented Into:

- Device Type: IVUS Catheter, and IVUS Console.

- Coronary Optical Coherency Tomography – Further Segmented Into:

- Device Type: OCT Catheter, and OCT Console.

- Hemostasis Valve

*Single-year unit share breakdown only

RESEARCH SCOPE SUMMARY

| Report Attribute | Details |

|---|---|

| Region | United States |

| Base Year | 2024 |

| Forecast | 2025-2031 |

| Historical Data | 2021-2023 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.