Product Description

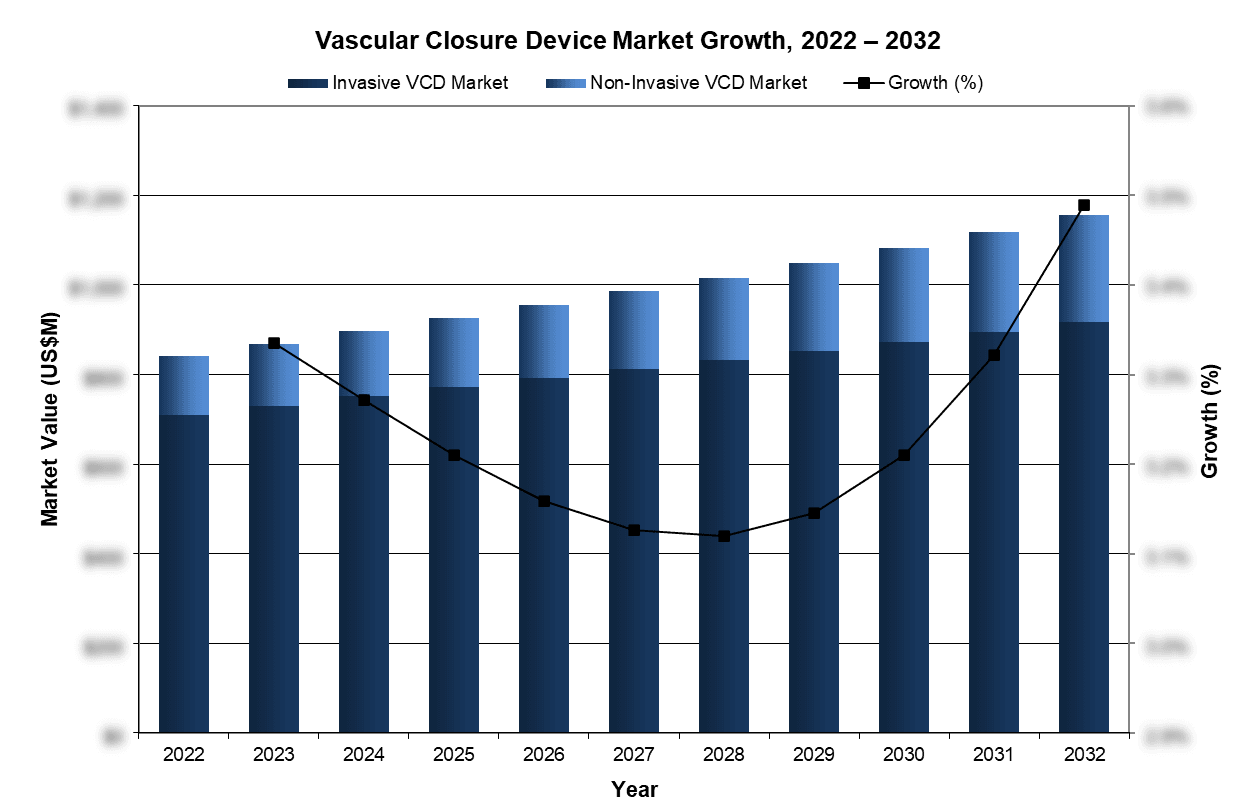

Overall, the global VCD market was valued at over $926 million in 2025. This is expected to increase over the forecast period at a CAGR of 3.2% to reach nearly $1.2 billion.

The full report suite on the global market for vascular closure devices (VCDs) includes a meticulous examination across seven prominent geographical regions, namely North America, Latin America, Western Europe, Central and Eastern Europe, the Middle East, Asia Pacific and Africa. Within each of these delineated regions, a comprehensive scrutiny will be conducted encompassing various facets, including market valuation, unit analysis and ASP. Moreover, the report will extend its projections up to the year 2032, thereby providing a comprehensive and anticipatory understanding of the market trends and trajectories for the given period.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2032, and Historical Data to 2022

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

Global Vascular Closure Device Market Trends

The incidence and severity of complications, such as compromised blood flow, remain a factor constraining the VCD market. However, complication rates have steadily declined due to improved device designs and more selective use by physicians. Despite these advancements, market growth will remain limited until clinicians are confident that complication rates have decreased sufficiently to justify the higher cost of these devices.

Global Vascular Closure Device Market Share Insights

- Abbott led the global vascular closure device (VCD) market in 2025 and it’s portfolio includes three invasive options: StarClose™, PerClose ProGlide™ and ProStar™ XL. The PerClose™ device closes the arterial puncture using sutures with needles and a knot, while StarClose™ employs an external nitinol clip to reduce the risk of emboli. ProStar™ XL is a suture-based system designed for access sites ranging from 8.5 F to 10 F. Additionally, Abbott offers non-invasive options through the RadiStop™ and FemoStop™ Gold lines, acquired from St. Jude Medical in 2017.

- Terumo’s leadership in the vascular closure device (VCD) market is largely driven by its Angio-Seal™ product line making them the second largest in 2025. The Angio-Seal™ VIP, featuring enhancements such as a coated suture and collagen sponge, has bolstered the company’s market position. The Angio-Seal™ Evolution™, launched in 2010, incorporates an automated deployment system designed to accommodate procedural variability. Terumo also markets the Angio-Seal™ STS PLUS. Expanding into large-bore vessel closure, Terumo acquired the XPro™ device from Medeon Biodesign in 2018, which utilizes a unique dual-suture delivery system and received CE mark approval in 2017.

- Cardinal Health strengthened its presence in the vascular closure device (VCD) market through the 2015 acquisition of Cordis and held the third position in 2025. Prior to this, AccessClosure had launched the Mynx™ VCD, which effectively addressed challenges such as vessel malpositioning by using a tissue tract sealant that dissolves within 30 days, allowing for quicker site re-access if needed. The 2012 introduction of MynxGrip™ further improved closure performance and expanded market share. Under Cardinal Health, the Mynx™ product line now includes Mynx™ACE® and MynxGrip® VCDs. Additionally, Cordis previously marketed the EXOSEAL™ VCD before its acquisition.

Global Vascular Closure Device Market Segmentation Summary

- Vascular Closure Device Market – Further Segmented Into:

- Device Type: Non-Invasive, and Invasive.

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, United Kingdom) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Malaysia, Mongolia, Myanmar, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2025 |

| Forecast | 2026-2032 |

| Historical Data | 2022-2024 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.