Product Description

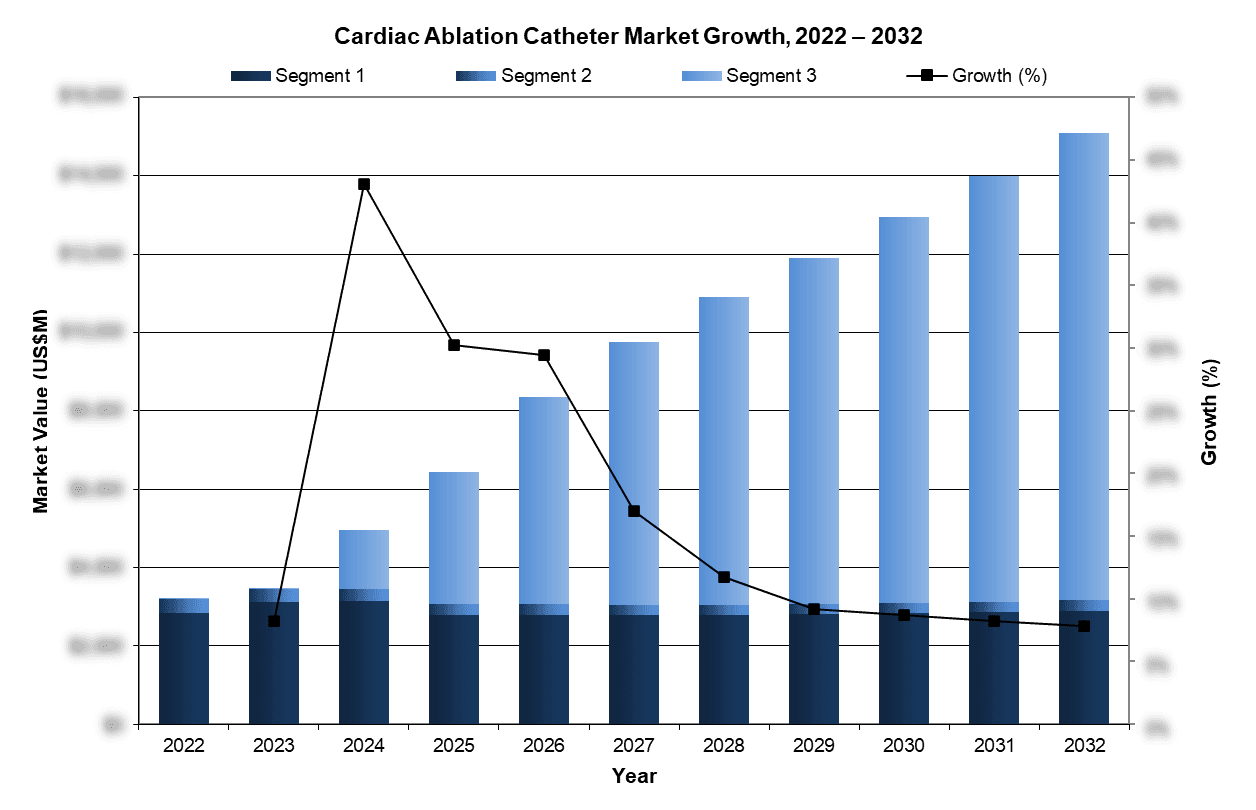

The global cardiac ablation catheter market was valued at $6.4 billion in 2025. This is expected to increase over the forecast period at a CAGR of 12.9% to reach nearly $15.0 billion.

The full report suite on the global market for cardiac ablation catheters includes radiofrequency (RF) ablation catheters, cryoablation catheters, and PFA catheters.

The report includes data for 65 countries across 7 different regions which include North America, Latin America, Western Europe, Central & Eastern Europe, Middle East, Asia-Pacific, and Africa.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2032, and Historical Data to 2022

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

Global Cardiac Ablation Catheter Market Trends

The cardiac ablation catheter market is experiencing a major disruption driven by the rapid global adoption of pulsed field ablation (PFA), which is fundamentally reshaping energy modality preferences across EP labs. PFA’s strong safety profile and procedural efficiency are accelerating share gains at the expense of legacy technologies, with cryoablation seeing clear declines and conventional RF ablation volumes beginning to contract in key North American and Western European markets. At the same time, emerging dual-energy ablation platforms are gaining traction as labs seek flexibility and future-proofing, reinforcing a shift toward higher-value, system-based solutions and concentrating share among companies best positioned in next-generation ablation ecosystems.

The cardiac ablation catheter market is experiencing a major disruption driven by the rapid global adoption of pulsed field ablation (PFA), which is fundamentally reshaping energy modality preferences across EP labs. PFA’s strong safety profile and procedural efficiency are accelerating share gains at the expense of legacy technologies, with cryoablation seeing clear declines and conventional RF ablation volumes beginning to contract in key North American and Western European markets. At the same time, emerging dual-energy ablation platforms are gaining traction as labs seek flexibility and future-proofing, reinforcing a shift toward higher-value, system-based solutions and concentrating share among companies best positioned in next-generation ablation ecosystems.

Global Cardiac Ablation Catheter Market Share Insights

- Boston Scientific led the cardiac ablation catheter market in 2025, driven by early scale leadership in pulsed field ablation through the FARAPULSE platform and FARAWAVE catheter, which strengthened physician adoption and accelerated conversion of AF ablations toward its disposable ecosystem. With an established RF portfolio and broad EP capital footprint, each incremental PFA installation reinforced catheter pull-through and positioned the company to capture an outsized share of continued growth in global AF ablation volumes.

- Johnson & Johnson ranked second in cardiac ablation catheters, underpinned by its leading irrigated RF franchise tightly integrated with its mapping ecosystem and supported by expanding PFA offerings in 2025. Its scale in EP diagnostics and broad RF plus PFA portfolio positions the company to defend and incrementally grow share as global AF ablation volumes continue rising.

- Medtronic reinforced its position in cardiac ablation as adoption of pulsed field ablation scaled, supported by U.S. FDA approvals that broadened access to its PFA portfolio led by PulseSelect™ and the Sphere-9™ catheter used with the Affera™ mapping and ablation system. By late 2025, the company was reporting rapid, PFA-led acceleration in its Cardiac Ablation Solutions business, reflecting meaningful commercial traction as centers expanded PFA utilization.

Global Cardiac Ablation Catheter Market Segmentation Summary

- Radiofrequency Ablation (RF) Catheter Market

- Cryoablation Catheter Market

- Pulsed Field Ablation (PFA) Catheter Market

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, United Kingdom) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Malaysia, Mongolia, Myanmar, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2025 |

| Forecast | 2026-2032 |

| Historical Data | 2022-2024 |

| Quantitative Coverage | Procedure Numbers, Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.