| Figure 1‑1: Digital Dentistry Market Share Ranking by Segment, Global, 2021 |

| Figure 1‑2: Companies Researched in this Report (1 of 2) |

| Figure 1‑3: Companies Researched in this Report (2 of 2) |

| Figure 1‑4: Factors Impacting the Digital Dentistry Market by Segment, Global |

| Figure 1‑5: Recent Events in the Digital Dentistry Market, Global, 2018 – 2022 (1 of 2) |

| Figure 1‑6: Recent Events in the Digital Dentistry Market, Global, 2018 – 2022 (2 of 2) |

| Figure 1‑7: Digital Dentistry Markets Covered |

| Figure 1‑8: Digital Dentistry Regions Covered, Global (1 of 2) |

| Figure 1‑9: Digital Dentistry Regions Covered, Global (2 of 2) |

| Figure 1‑10: Version History |

| Figure 2‑1: Digital Dentistry Market by Segment, Worst Case Scenario, Global, 2018 – 2028 (US$M) |

| Figure 2‑2: Digital Dentistry Market by Segment, Base Case Scenario, Global, 2018 – 2028 (US$M) |

| Figure 2‑3: Digital Dentistry Market by Segment, Best Case Scenario, Global, 2018 – 2028 (US$M) |

| Figure 4‑1: CAD/CAM Systems by Company (1 of 2) |

| Figure 4‑2: CAD/CAM Systems by Company (2 of 2) |

| Figure 4‑3: CAD/CAM Materials by Company (1 of 2) |

| Figure 4‑4: CAD/CAM Materials by Company (2 of 2) |

| Figure 4‑5: Dental 3D Printers by Company |

| Figure 4‑6: Class 2 Device Recall Ivoclar Vivadent |

| Figure 4‑7: One-Tooth One-Time (1T1T) A Straightforward Approach to Replace Missing Teeth in the Posterior Region: a Case Series (1T1T) |

| Figure 4‑8: Evaluation of the Accuracy of Digital Models Obtained Using Intraoral and Extraoral Scanners |

| Figure 4‑9: Clinical Performance of Ceramic CAD/CAM Crowns |

| Figure 4‑10: Retrospective Study on Clinical Performance of Screw-retained Implant Crowns |

| Figure 4‑11: Patient Satisfaction & Retention of Milled, 3D Printed and Conventional Complete Dentures |

| Figure 4‑12: Clinical Evaluation of Chairside CAD/CAM Resilient Ceramic Crowns |

| Figure 4‑13: Assessment of the Accuracy of Surgical Guide Designed From Digital Impression, Dental Model Scanning Using CBCT and Desktop Scanner in Computer Guided Implantology |

| Figure 4‑14: Complete Denture Tooth Movement in Digital Light Processing Versus Conventional Fabrication Techniques |

| Figure 4‑15: Clinical Performance of Chairside CAD/CAM Restorations |

| Figure 4‑16: Clinical Performance of Milled Resin Composite in Restoration of Endodontically Treated Posterior Teeth Over One Year |

| Figure 4‑17: Clinical Performance of Milled Resin Composite in Restoration of Endodontically Treated Posterior Teeth Over One Year |

| Figure 4‑18: Clinical Outcomes of CAD/CAM Single-Retainer Monolithic Zirconia Ceramic Resin-Bonded Fixed Dentures Bonded With Two Different Resin Cements |

| Figure 4‑19: Monolithic CAD/CAM Single Tooth Ceramic Crowns |

| Figure 4‑20: Clinical Performance of Chairside CAD/CAM Restorations |

| Figure 4‑21: Complete Denture Tooth Movement in Digital Light Processing Versus Conventional Fabrication Techniques |

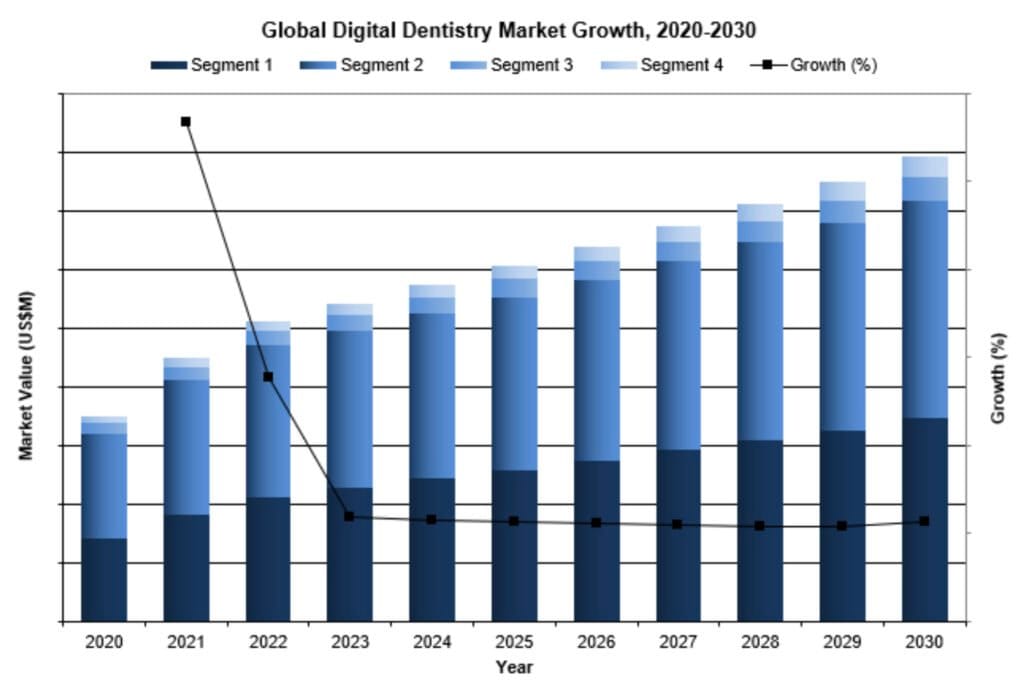

| Figure 5‑1: Digital Dentistry Market by Segment, Global, 2018 – 2028 (US$M) |

| Figure 5‑2: Digital Dentistry Market by Region, Global, 2018 – 2028 (US$M) |

| Figure 5‑3: Leading Competitors, Digital Dentistry Market by Segment, Global, 2021 |

| Figure 5‑4: SWOT Analysis, 3D Systems |

| Figure 5‑5: SWOT Analysis, 3M ESPE |

| Figure 5‑6: SWOT Analysis, 3Shape |

| Figure 5‑7: SWOT Analysis, Align Technology |

| Figure 5‑8: SWOT Analysis, Dentsply Sirona |

| Figure 5‑9: SWOT Analysis, Digital Dental |

| Figure 5‑10: SWOT Analysis, E4D Technologies |

| Figure 5‑11: SWOT Analysis, Formlabs |

| Figure 5‑12: SWOT Analysis, Glidewell Dental |

| Figure 5‑13: SWOT Analysis, Ivoclar Vivadent |

| Figure 5‑14: SWOT Analysis, Stratasys |

| Figure 6‑1: CAD/CAM Device Markets Covered |

| Figure 6‑2: CAD/CAM Device Regions Covered, Global (1 of 2) |

| Figure 6‑3: CAD/CAM Device Regions Covered, Global (2 of 2) |

| Figure 6‑4: CAD/CAM Device Market by Segment, Global, 2018 – 2028 (US$M) |

| Figure 6‑5: CAD/CAM Device Market by Region, Global, 2018 – 2028 (US$M) |

| Figure 6‑6: Milling System Market, Global, 2018 – 2028 |

| Figure 6‑7: Units Sold by Region, Milling System Market, Global, 2018 – 2028 |

| Figure 6‑8: Average Selling Price by Region, Milling System Market, Global, 2018 – 2028 (US$) |

| Figure 6‑9: Market Value by Region, Milling System Market, Global, 2018 – 2028 (US$M) |

| Figure 6‑10: Installed Base by Region, Milling System Market, Global, 2018 – 2028 |

| Figure 6‑11: Laboratory Scanner Market, Global, 2018 – 2028 |

| Figure 6‑12: Units Sold by Region, Laboratory Scanner Market, Global, 2018 – 2028 |

| Figure 6‑13: Average Selling Price by Region, Laboratory Scanner Market, Global, 2018 – 2028 (US$) |

| Figure 6‑14: Market Value by Region, Laboratory Scanner Market, Global, 2018 – 2028 (US$M) |

| Figure 6‑15: Installed Base by Region, Laboratory Scanner Market, Global, 2018 – 2028 |

| Figure 6‑16: Chairside System Market, Global, 2018 – 2028 |

| Figure 6‑17: Units Sold by Region, Chairside System Market, Global, 2018 – 2028 |

| Figure 6‑18: Average Selling Price by Region, Chairside System Market, Global, 2018 – 2028 (US$) |

| Figure 6‑19: Market Value by Region, Chairside System Market, Global, 2018 – 2028 (US$M) |

| Figure 6‑20: Installed Base by Region, Chairside System Market, Global, 2018 – 2028 |

| Figure 6‑21: Intraoral Scanner Market, Global, 2018 – 2028 |

| Figure 6‑22: Units Sold by Region, Intraoral Scanner Market, Global, 2018 – 2028 |

| Figure 6‑23: Average Selling Price by Region, Intraoral Scanner Market, Global, 2018 – 2028 (US$) |

| Figure 6‑24: Market Value by Region, Intraoral Scanner Market, Global, 2018 – 2028 (US$M) |

| Figure 6‑25: Installed Base by Region, Intraoral Scanner Market, Global, 2018 – 2028 |

| Figure 6‑26: Leading Competitors, CAD/CAM Device Market, Global, 2021 |

| Figure 6‑27: Leading Competitors, CAD/CAM Device Market by Segment, Global, 2021 |

| Figure 6‑28: Leading Competitors, Milling System Market, Global, 2021 |

| Figure 6‑29: Leading Competitors, Laboratory Scanner Market, Global, 2021 |

| Figure 6‑30: Leading Competitors, Chairside System Market, Global, 2021 |

| Figure 6‑31: Leading Competitors, Intraoral Scanner Market, Global, 2021 |

| Figure 7‑1: CAD/CAM Material Markets Covered |

| Figure 7‑2: CAD/CAM Material Regions Covered, Global (1 of 2) |

| Figure 7‑3: CAD/CAM Material Regions Covered, Global (2 of 2) |

| Figure 7‑4: CAD/CAM Material Market by Segment, Global, 2018 – 2028 (US$M) |

| Figure 7‑5: CAD/CAM Material Market by Region, Global, 2018 – 2028 (US$M) |

| Figure 7‑6: CAD/CAM Block Market, Global, 2018 – 2028 |

| Figure 7‑7: Units Sold by Region, CAD/CAM Block Market, Global, 2018 – 2028 |

| Figure 7‑8: Average Selling Price by Region, CAD/CAM Block Market, Global, 2018 – 2028 (US$) |

| Figure 7‑9: Market Value by Region, CAD/CAM Block Market, Global, 2018 – 2028 (US$M) |

| Figure 7‑10: CAD/CAM Disc Market, Global, 2018 – 2028 |

| Figure 7‑11: Units Sold by Region, CAD/CAM Disc Market, Global, 2018 – 2028 |

| Figure 7‑12: Average Selling Price by Region, CAD/CAM Disc Market, Global, 2018 – 2028 (US$) |

| Figure 7‑13: Market Value by Region, CAD/CAM Disc Market, Global, 2018 – 2028 (US$M) |

| Figure 7‑14: CAD/CAM Block Units Sold by Material Type, U.S., 2018 – 2028 |

| Figure 7‑15: Zirconia CAD/CAM Block Units Sold by Region, U.S., 2018 – 2028 |

| Figure 7‑16: Lithium Disilicate CAD/CAM Block Units Sold by Region, U.S., 2018 – 2028 |

| Figure 7‑17: Other Ceramic CAD/CAM Block Units Sold by Region, U.S., 2018 – 2028 |

| Figure 7‑18: CAD/CAM Disc Units Sold by Material Type, U.S., 2018 – 2028 |

| Figure 7‑19: Zirconia CAD/CAM Disc Units Sold by Region, U.S., 2018 – 2028 |

| Figure 7‑20: Metal CAD/CAM Disc Units Sold by Region, U.S., 2018 – 2028 |

| Figure 7‑21: Other Ceramic CAD/CAM Disc Units Sold by Region, U.S., 2018 – 2028 |

| Figure 7‑22: Leading Competitors, CAD/CAM Material Market, Global, 2021 |

| Figure 8‑1: Dental 3D Printer Regions Covered, Global (1 of 2) |

| Figure 8‑2: Dental 3D Printer Regions Covered, Global (2 of 2) |

| Figure 8‑3: Dental 3D Printer Market, Global, 2018 – 2028 |

| Figure 8‑4: Units Sold by Region, Dental 3D Printer Market, Global, 2018 – 2028 |

| Figure 8‑5: Average Selling Price by Region, Dental 3D Printer Market, Global, 2018 – 2028 (US$) |

| Figure 8‑6: Market Value by Region, Dental 3D Printer Market, Global, 2018 – 2028 (US$M) |

| Figure 8‑7: Installed Base by Region, Dental 3D Printer Market, Global, 2018 – 2028 |

| Figure 8‑8: Leading Competitors, Dental 3D Printer Market, Global, 2021 |