Product Description

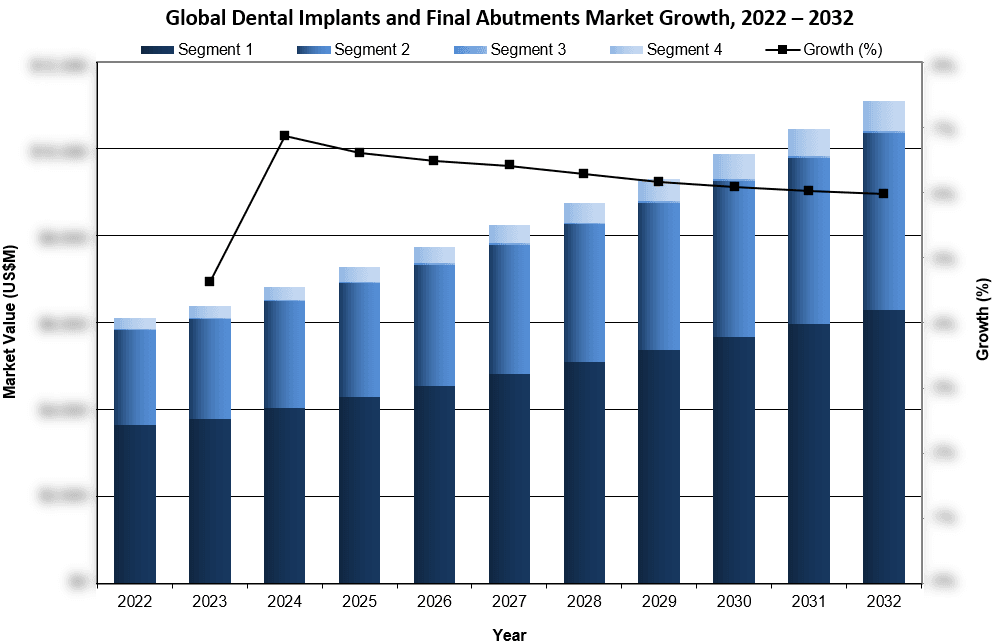

Overall, the global dental implant and final abutment market was valued at over $7 billion in 2025. This is expected to increase over the forecast period at a CAGR of 6.2% to reach over $11 billion by 2032.

The full report suite on the global market for dental implants and final abutments includes dental implants, final abutments, treatment planning software and surgical guides.

The report includes data for 65 countries across 7 different regions which include North America, Latin America, Western Europe, Central & Eastern Europe, Middle East, Asia-Pacific, and Africa.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Market Drivers & Limiters

- Market Forecasts Until 2032, and Historical Data to 2022

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

Global Dental Implant and Final Abutment Market Trends

The availability of reimbursement for dental implant procedures in select countries represents a significant near- to mid-term growth driver for the dental implant and final abutment market, while the high cost of treatment relative to alternative restorative options continues to limit widespread adoption. In markets where partial public reimbursement or coverage through premium private insurance plans is available, improved patient affordability has historically led to a measurable increase in the proportion of the population opting for implant-based restorations, thereby supporting procedure volumes and the uptake of advanced treatment workflows. However, most private health and dental insurance policies do not provide coverage for implant procedures and out-of-pocket expenses remain substantial. Consequently, cost continues to be a key barrier to penetration, particularly in developing and price-sensitive regions. Although the gradual expansion of reimbursement frameworks is expected to contribute to market growth over the forecast period, uneven coverage and persistent affordability constraints are likely to moderate the long-term rate of adoption globally.

Global Dental Implant and Final Abutment Market Share Insights

- Straumann Group was the strongest competitor in the global dental implant and final abutment market in 2025. The company benefits from strong brand recognition, an extensive clinical evidence base and a long-standing reputation for delivering high-quality implant solutions. Straumann maintained a leading position in the premium implant segment, supported by a comprehensive portfolio that spans implants, final abutments, guided surgery solutions and integrated digital workflows. In parallel, Straumann’s subsidiary, Neodent, continued to strengthen the group’s position in the value implant segment, contributing meaningfully to overall unit growth and market penetration, particularly in price-sensitive regions. Ongoing investments in product innovation, digital dentistry platforms and targeted mergers and acquisitions have further reinforced Straumann Group’s competitive positioning, leaving the company well placed to sustain its market leadership over the forecast period.

- Envista Holdings was the second-leading competitor in the global dental implant market and in the final abutment market in 2025. Through its core implant brands, most notably Nobel Biocare in the premium segment and Implant Direct in the value segment, the company participates across multiple price tiers and clinical workflows. Nobel Biocare continues to provide strong performance in premium and full-arch indications, while Implant Direct supports unit growth in price-sensitive markets and among general practitioners. Envista’s implant business is closely linked to its digital ecosystem, particularly the DTX Studio™ platform and guided surgery solutions, which drive utilization across implants, prosthetics and laboratory workflows. Implant-related products represent a significant portion of the company’s total revenue and are expected to benefit from aging demographics, increasing adoption of digital and guided treatment protocols and the ongoing expansion of dental service organizations (DSOs). Envista was created through the separation of Danaher’s dental segment and has operated as an independent, publicly traded company since its 2019 listing on the New York Stock Exchange under the ticker NVST, with a continued strategic focus on implant, orthodontic and digital workflow integration.

- Dentsply Sirona was the third-leading competitor in the dental implant and final abutment market in 2025. The company maintains a leading position in the surgical guide and treatment planning software segments and remains a major participant in both implants and prosthetics through its premium implant systems and its value-based MIS Implants brand. This multi-tier implant strategy enables Dentsply Sirona to address both premium and price-sensitive customer segments, while its integrated digital ecosystem, spanning imaging, intraoral scanning, planning software and guided surgery supports utilization across the implant workflow. The company’s broad and highly diversified portfolio across equipment, consumables and digital solutions positions it to capture growth across multiple segments of the implant market and to leverage cross-selling opportunities within its large installed base. Ongoing product development and workflow integration continue to strengthen its competitive position.

Global Dental Implant and Final Abutment Market Segmentation Summary

- Dental Implants Market – Further Segmented Into:

- Type: Premium, Value, and Discount Implants.

- Material: Titanium, and Ceramic/Zirconia.

- Shape: Parallel Wall, and Tapered.

- Procedure Type*: One-Stage Surgery, Two-Stage Surgery, and Immediate Loading.

- Connection Type*: Internal Connection, External Connection, and One-Piece.

- Application*: Single-Tooth Replacement, Multi-Tooth Bridge Partial and Full Arch Securement, and Denture Securement.

- Final Abutments Market – Further Segmented Into:

-

- Fabrication: Stock, Custom Cast, and CAD/CAM.

- Material: Titanium, Ceramic/Zirconia, and Gold.

- Type*: Cement-Retained, Screw-Retained, and Denture Retaining.

-

- Treatment Planning Software Market

- Surgical Guide Market

*Segment is analyzed at a unit level only.

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Region | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, United Kingdom) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Malaysia, Mongolia, Myanmar, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2025 |

| Forecast | 2026-2032 |

| Historical Data | 2022-2024 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.