Product Description

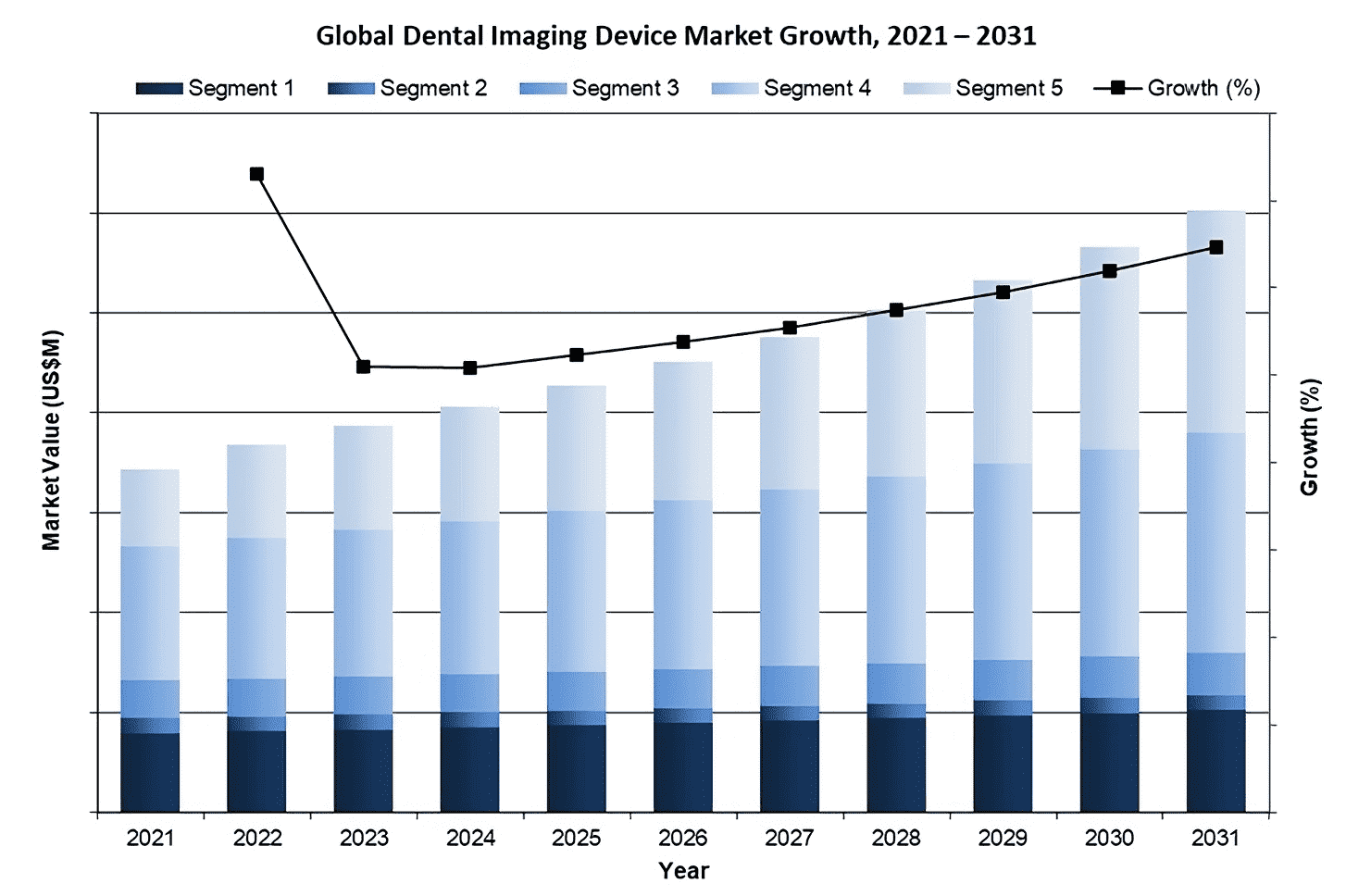

Overall, the global dental imaging device market was valued at over $4 billion in 2024. This is expected to increase over the forecast period at a CAGR of 5.8% to reach over $6 billion.

The full report suite on the global market for dental imaging devices includes the intraoral X-ray imaging equipment, intraoral X-ray imaging consumables, extraoral X-ray imaging, cone beam computed tomography (CBCT) and intraoral scanner markets.

This report includes data for 65+ countries across 7 different regions. These regions are North America, Latin America, Western Europe, Central & Eastern Europe, Middle East, Asia-Pacific, and Africa.

MARKET REPORT DATA TYPES INCLUDED

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2021

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

GLOBAL DENTAL IMAGING MARKET TRENDS

AI-powered algorithms are increasingly being integrated into dental imaging systems, enabling automated identification of caries, nerve cavitation, and other dental conditions. This is enhancing the accuracy of diagnoses, improving workflow efficiency, and helping dentists make more informed treatment decisions. AI is also aiding in reducing image processing times, enhancing patient comfort, and supporting faster, more accurate diagnostics.

GLOBAL DENTAL IMAGING DEVICE MARKET LEADERS

- Dentsply Sirona is the leading company in the global dental imaging device market, holding a dominant position in extraoral imaging. The company continues to be at the forefront of technological advancements in the intraoral X-ray and CBCT segments while maintaining its stronghold in the extraoral imaging market. Dentsply Sirona’s reputation for research and development is strengthened by its recent focus on integrating AI technologies and cloud-based systems into its imaging products. Its extraoral imaging devices are known for their precision and high-quality results, making them the top choice for practices worldwide. The company is also leading the way with its partnership with Google Cloud, which enhances its machine learning capabilities and contributes to more automated diagnostics.

- KaVo remains top of the market in the intraoral X-ray imaging equipment and CBCT segments. With its comprehensive range of dental sensors, including the GXS-700™, IXS™ and KaVo Titanium, KaVo provides reliable solutions for precise diagnostics. The company’s offerings, such as the NOMAD Pro 2™ and FOCUS™, dominate the intraoral X-ray segment, providing portability, ease of use and excellent image quality. KaVo’s commitment to innovation in the CBCT space has positioned it as the leader in this fast-growing sector, which continues to expand as dentists increasingly rely on 3D imaging for more accurate diagnosis and treatment planning.

- Carestream Dental holds a significant position in the dental consumables market and is a strong player across all segments, particularly in the intraoral X-ray and CBCT markets. While Carestream Dental is known for its high-tech solutions such as the CS 9600, the company’s focus on the dental consumables market—including sensors and digital imaging plates—has allowed it to maintain a competitive edge. Carestream continues to show growth in the CBCT segment with innovative models that offer versatile imaging capabilities. The company’s transition from the analog market to digital solutions positions it as a strong player with cutting-edge technology that remains affordable and reliable for dental professionals globally.

MARKET SEGMENTATION SUMMARY

While this report suite contains all applicable market data, each of the markets are also available as stand alone MedCore reports. This allows you to get access to only the specific market segment research that you need. You can view all these included reports and segmentation here:

- Intraoral X-ray Imaging Equipment Market – Further Segmented Into:

- Device Type: Intraoral X-ray Device, PSP System, and Digital Sensors.

- Intraoral X-ray Imaging Consumables – Further Segmented Into:

- Device Type: Analog Film and PSP Plates.

- Extraoral X-ray Imaging – Further Segmented Into:

- Device Type: Digital Panoramic System, and Pan/Ceph System.

- CBCT Market – Further Segmented Into:

- Modality Type: Small FOV, Medium FOV, and Large FOV Devices.

- Intraoral Scanner Market

RESEARCH SCOPE SUMMARY

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, United Kingdom) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Malaysia, Mongolia, Myanmar, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Historical Data | 2021-2023 |

| Quantitative Data | Procedure Numbers, Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Data | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.