Product Description

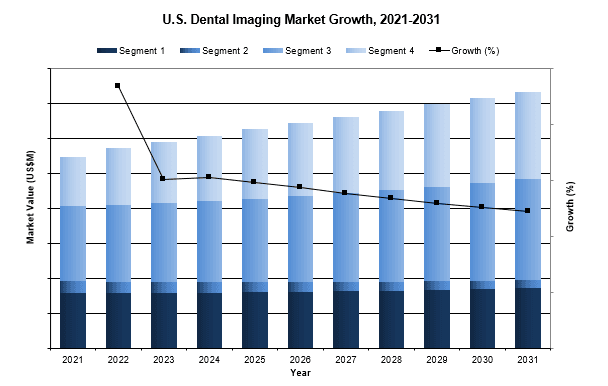

Overall, the U.S. dental imaging device market was valued at nearly $1.2 billion in 2024. This is expected to increase over the forecast period at a CAGR of 2.7% to reach nearly $1.5 billion.

The comprehensive report on the U.S. market for dental imaging devices covers intraoral X-ray devices, including intraoral imaging consumables, extraoral X-ray devices, cone beam computed tomography (CBCT) scanners and intraoral scanners, with a focus on digital sensors, PSP plates and a gradually phasing-out analog film segment.

MARKET DATA INCLUDED

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- COVID-19 Impact Analysis

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2021

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

U.S. DENTAL IMAGING PROCEDURE NUMBERS

Dental X-ray procedures include intraoral and extraoral X-rays, as well as cone beam computed tomography (CBCT) scans. Intraoral X-rays consist of only one X-ray image that is captured intraorally. In 2024, approximately over 1 billion X-ray procedures were performed in the U.S., with the majority of dental X-ray procedures resulting from routine dental checkups among the general population. The growth in the total number of procedures is not primarily driven by an increase in the number of patients but rather by the widespread transition to digital imaging technology.

U.S. DENTAL IMAGING MARKET INSIGHTS

One of the primary drivers in the U.S. dental imaging market is the shift toward modular extraoral devices. Growing confidence in CBCT technology among U.S. dentists has fueled the adoption of modular CBCT systems, with 2D and 3D components becoming increasingly interchangeable. This trend not only keeps clinics equipped with familiar 2D functionality but also enables expanded operatory efficiency through modular CBCT, aligning with rising demand for advanced diagnostics and cosmetic dentistry services.

TOP U.S. DENTAL IMAGING COMPANIES

- In 2024, KaVo Kerr (under Danaher) led nearly all dental imaging markets, excluding intraoral scanners, capturing close to one-third of the market. Its dominance in digital sensors outpaced Carestream’s X-ray and analog film foothold, securing KaVo Kerr’s lead in intraoral imaging. Soon, KaVo Kerr will become independent as part of Envista.

- Align Technologies solidified its second position, driven by its iTero intraoral scanners and proprietary Invisalign integration, fueling demand across orthodontic and general dental practices and maintaining its lead in digital dental workflows.

- Dentsply Sirona remains a top competitor in intraoral, CBCT, and extraoral markets, bolstered by its Shick sensor and Orthophos scanner lines. It holds the third-largest U.S. share, close behind Align Technologies.

MARKET SEGMENTATION SUMMARY

- Intraoral X-ray Imaging – Broken down by:

-

- Segment: Intraoral X-ray Equipment, Intraoral X-ray Consumables

- Device Type

-

- Extraoral X-ray Imaging – Broken down by:

- Device Type: Digital Panoramic System, Pan/Ceph System

- CBCT Device – Broken down by:

- Modality: Small FOV, Medium FOV, Large FOV

- Intraoral Scanner – Broken down by:

- General Practitioner: Orthodontist, Other Specialties

RESEARCH SCOPE SUMMARY

| Report Attribute | Details |

|---|---|

| Region | North America (United States) |

| Base Year | 2024 |

| Forecast | 2021-2031 |

| Historical Data | 2021-2023 |

| Quantitative Coverage | Procedure Numbers, Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | COVID-19 Impact, Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |