Product Description

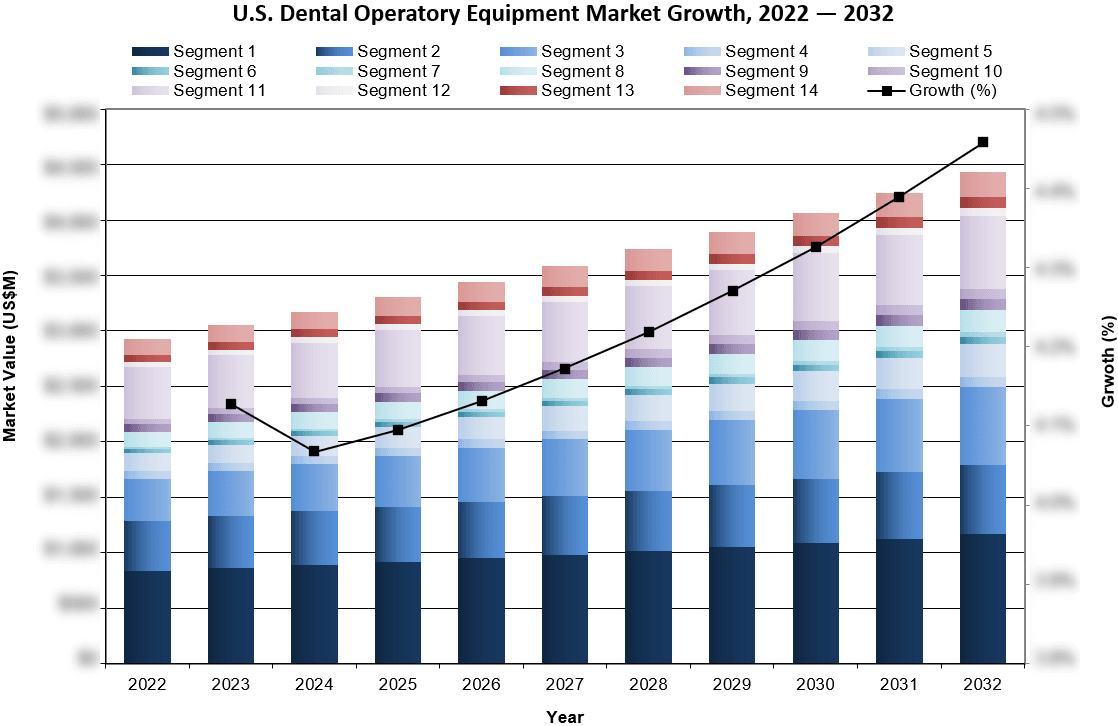

The U.S. dental operatory equipment market was valued at over $3.3 billion in 2025. This is expected to increase over the forecast period at a CAGR of 4.3% to reach over $4.4 billion.

The full report suite on the U.S. market for dental operatory equipment includes dental treatment centers, dental cabinetry, dental handpieces, curing lights, ultrasonic scalers, intraoral cameras, caries detection devices, dental autoclaves, dental vacuum systems, dental air compressors, practice management software, dental microscopes, dental loupes and dental lasers.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Market Drivers & Limiters

- Market Forecasts Until 2032, and Historical Data to 2022

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

U.S. Dental Operatory Equipment Market Trends

Intraoral scanners are becoming an increasingly important entry point to digital workflows. While penetration remains below half of U.S. practices, adoption is accelerating as prices gradually decline and integration with CAD/CAM systems improves. Dental support organizations (DSOs) and younger dentists are leading uptake, whereas smaller independent practices often delay purchases due to cost considerations. Overall, scanners are expected to be a key driver of operatory modernization over the forecast period.

U.S. Dental Operatory Equipment Market Share Insights

- A-dec led the dental operatory equipment market in 2025 in the U.S.. The company maintained its frontrunner position in the dental treatment center and cabinetry segments. A-dec also remained active in the dental handpiece market.

- Midmark was the second-largest player in the dental operatory equipment market in 2025. The company held strong positions in the dental cabinetry, air compressor and vacuum system segments Midmark also led the autoclave market and was active in the dental treatment center segment.

- DCI Edge ranked as the third-largest company in the dental operatory equipment market in 2025 in the U.S.. The company maintained a strong presence in the dental treatment center and cabinetry segments and was recognized for its value-driven, modular solutions.

U.S. Dental Operatory Equipment Market Segmentation Summary

- Intraoral Camera Market – Further Segmented Into:

- Device Type: Economy, and Standard.

- Caries Detection Market – Further Segmented Into:

- Device Type:Imaging-Based, and Non-Imaging-Based.

- Dental Autoclave Market

- Dental Vacuum System Market – Further Segmented Into:

- Product Type: Wet, and Dry.

- Dental Air Compressor Market

- Practice Management Software Market – Further Segmented Into:

- Product Type: Client Server Software, and Cloud-Based Software.

- Dental Microscope Market

- Dental Laser Market – Further Segmented Into:

- Product Type: Soft Tissue, and All-Tissue.

- Dental Loupes Market

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Region | United States |

| Base Year | 2025 |

| Forecast | 2026-2032 |

| Historical Data | 2022-2024 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.