Product Description

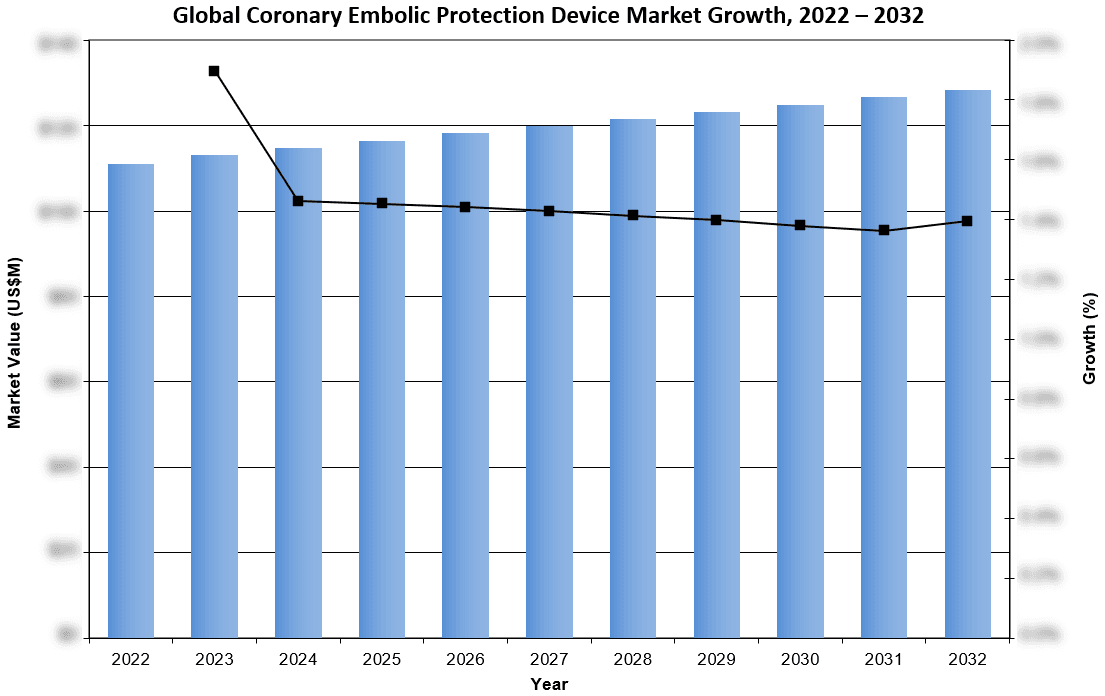

Overall, the global coronary embolic protection device market was valued at over $116 million in 2025. This is expected to increase over the forecast period at a CAGR of 1.4% to reach over $128 million.

The full report suite includes the global coronary embolic protection device (EPD) market. The EPD was invented to address the risk of a dislodged thrombus or embolus during interventional coronary procedures.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Market Drivers & Limiters

- Market Forecasts Until 2032, and Historical Data to 2022

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

Global Coronary Embolic Protection Device Market Trends

Market expansion is being driven by the growing shift toward minimally invasive, catheter-based procedures. These less invasive approaches are more compatible with the use of EPDs, creating opportunities for the market to grow and reach new regions.

Global Coronary Embolic Protection Device Market Share Insights

- Boston Scientific was the leading competitor in the coronary EPD market in 2025. The company offers the FilterWire EZ™ product line, a distal filter-basket system designed to adapt to various vessel shapes and sizes, as well as the SENTINEL™ Cerebral Protection System. The FilterWire EZ™ is indicated for use during angioplasty and stenting procedures in coronary saphenous vein bypass grafts and carotid arteries.

- Medtronic ranked as the second-leading competitor in the coronary EPD market in 2025. The company offers the SpiderFX® distal filter-basket embolic protection system. With a broad portfolio spanning both coronary and peripheral markets, Medtronic is able to strategically bundle products and strengthen its competitive position.

- Abbott ranked as the third-leading competitor in the coronary EPD market in 2025. The company offers the RX Accunet® embolic protection systems, designed for carotid interventions and featuring rapid-exchange delivery for ease of use.

Global Coronary Embolic Protection Device Market Segmentation Summary

- Coronary Embolic Protection Device Market

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Regions | North America (Canada, United States) Latin America (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Mexico, Panama, Paraguay, Peru, Puerto Rico, Uruguay, Venezuela) Western Europe (Austria, Benelux, France, Germany, Italy, Portugal, Scandinavia, Spain, Switzerland, United Kingdom) Central & Eastern Europe (Azerbaijan, Baltic States, Belarus, Bulgaria, Croatia, Czech Republic, Georgia, Greece, Hungary, Kazakhstan, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Turkey, Ukraine) Middle East (Bahrain, Iran, Israel, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates) Asia Pacific (Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Kyrgyzstan, Macao, Malaysia, Mongolia, Myanmar, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Uzbekistan, Vietnam) Africa (Algeria, Egypt, Ethiopia, Ghana, Kenya, Libya, Morocco, Nigeria, South Africa, Sudan, Uganda) |

| Base Year | 2025 |

| Forecast | 2026-2032 |

| Historical Data | 2022-2024 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.