Product Description

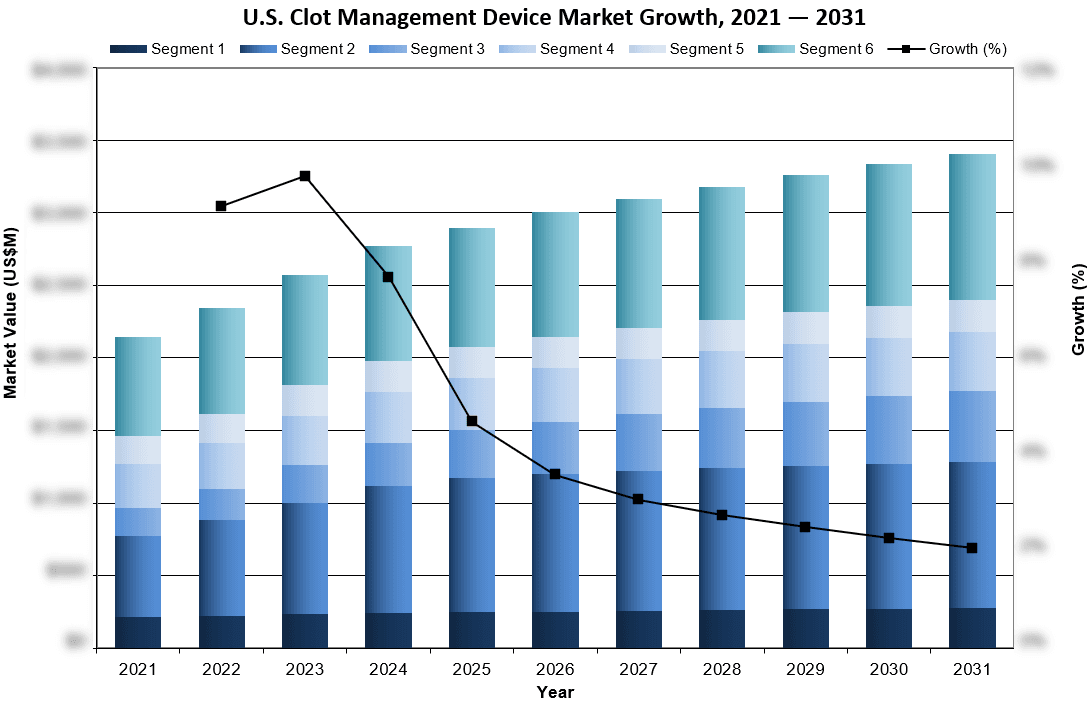

The U.S. clot management device market was valued at nearly $2.8 billion in 2025. This is expected to increase over the forecast period at a CAGR of 3% to reach nearly $3.4 billion.

The full report suite on the U.S. market for clot management devices includes neurovascular detachable coil, neurovascular catheter, neurovascular guidewire, neurovascular stent, liquid embolic and peripheral vascular transcatheter embolization device markets.

Data Types Included

- Unit Sales, Average Selling Prices, Market Size & Growth Trends

- Procedure Numbers

- Market Drivers & Limiters

- Market Forecasts Until 2031, and Historical Data to 2021

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

U.S. Clot Management Device Market Trends

Neurovascular catheters remain the dominant segment in the clot management device market, driven by their critical role in thrombectomy procedures and by continuous refinements in aspiration and delivery technologies that improve safety and efficacy. Increasing use of these devices in both ischemic stroke and peripheral applications underscores their central place in procedural workflows.

At the same time, neurovascular guidewires are posting significant growth as improvements in trackability, torque response and device compatibility enable smoother navigation through complex vascular anatomies. Heightened demand for rapid, minimally invasive stroke interventions, coupled with ongoing technological innovation, is fueling adoption across both product categories and reshaping the competitive dynamics of the clot management landscape.

U.S. Clot Management Device Market Share Insights

- Medtronic remains a dominant force in the clot management device market, though increasing competition has eroded several of its historical monopolies. The company continues to hold more than half of the market share in the liquid embolic segment. Leveraging its extensive research and development capabilities, Medtronic continues to innovate, sustaining its leadership while expanding its portfolio of advanced neurological solutions. In 2025, Medtronic was the leading competitor in the U.S. neurovascular stent market, despite intensifying competition in the flow diversion stent segment. Its current offering, the Pipeline™ Flex, builds on the first-generation flow-diverting stent, which received FDA approval in 2011 for the treatment of large or giant wide-necked aneurysms in adults. Since its initial release, the device has increasingly been adopted for smaller and less complex aneurysms, and in 2019 its indication was expanded to include small- and medium-sized aneurysms.

- Stryker ranked as the second-largest competitor in the clot management device market in 2025, driven primarily by its strong performance in neurovascular guidewires and detachable coils. In January 2025, the company announced a definitive agreement to acquire Inari Medical, describing Inari’s venous thromboembolism portfolio as both innovative and highly complementary to Stryker’s neurovascular business. Beyond this acquisition, Stryker has expanded its portfolio by advancing innovative neurological solutions, with a particular emphasis on minimally invasive procedures, further solidifying its position as a key player in the evolving neurological device market.

- Terumo ranked as the third-leading competitor in the clot management device market in 2025, supported by its strong share across several key segments. The company’s Sofia series of guiding catheters secured its leading position in that category. Within the neurovascular stent space, Terumo offers the LVIS® and LVIS® Jr. devices, with the latter designed to complement smaller detachable coils through its larger compliant cell system. The company also led the intrasaccular stent market in 2025 with the expansion of its WEB™ family, including the FDA-approved WEB™ 17, available in multiple size variations for precise patient fit. In addition, Terumo provides the FRED™ and FRED™ X flow diversion systems, which are dual-layer devices engineered for flexibility, repositioning and compatibility with Headway® microcatheters. The FRED™ X further incorporates proprietary nano-polymer technology, enhancing durability and performance in complex cerebral vessels

U.S. Clot Management Device Market Segmentation Summary

- Detachable Coil Market – Further Segmented Into:

- Device Type: Bare Platinum, and Coated.

- Neurovascular Catheter Market – Further Segmented Into:

- Device Type: Over-the-Wire Microcatheter, Flow-Directed Microcatheter, and Guiding Catheter.

- Unit Analysis by Inner Diameter: <0.05 inch, and >0.05 inch.

- Unit Analysis by Inner Diameter: <1 mm, in between 1 and 2 mm, and >2 mm.

- Unit Analysis by Working Length: <100 cm, in between 100 and 150 cm, and >150 cm.

- Neurovascular Guidewire Market

- Neurovascular Stent Market – Further Segmented Into:

- Device Type: Traditional, Flow Diversion, and Intrasaccular Stent.

- Liquid Embolics Market – Further Segmented Into:

- Device Type: Neurovascular, and Peripheral Vascular.

- Transcatheter Embolization Market – Further Segmented Into:

- Device Type: Particle Embolization, Coil Embolization, and Plug Embolization.

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Region | United States |

| Base Year | 2024 |

| Forecast | 2025-2031 |

| Historical Data | 2021-2023 |

| Quantitative Coverage | Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |

CONTACT US FOR ADDITIONAL INFORMATION

For full segmentation and any questions regarding research coverage, please contact us for a complimentary demo of the full report.