The global dental implants and final abutments market was valued at over $6.1 billion in 2023 and is expected to reach $9.2 billion by 2030. Despite steady expansion, the market faces uneven regional growth and ongoing price sensitivity.

While demand for restorative and aesthetic dentistry is climbing, premium implant brands are under pressure from emerging value-oriented competitors.

In regions where affordability defines access, lower-priced alternatives are capturing share.

The coming years will see innovation and price efficiency reshape the definition of the best dental implants worldwide.

Find growth niches in minutes, not months.

Explore quick, actionable insights from the select markets.

Table of Contents

➜ Dental Implants Market Painpoints and Opportunities

➜ Dental Implants Market Segmentation

➜ Key Dental Implants Market Drivers

➜ Best Dental Implants Companies in 2025

➜ Dental Implants Regional Outlook

➜ Technology and Innovation Shaping the Best Dental Implants

➜ Dental Implants Insights: How Companies Can Compete

➜ A Steady Climb Towards Broader Accessibility

Key Takeaways

- The global dental implants market is projected to grow from $6.1 billion in 2023 to $9.2 billion by 2030.

- Price sensitivity remains the main limiter across all regions and segments.

- Value-oriented implant brands are gaining ground over premium competitors.

- Asia-Pacific, North America, and Western Europe remain the largest regional markets.

- Straumann, Envista, and Dentsply Sirona lead globally, each with unique strengths.

Dental Implants Market Painpoints and Opportunities

A defining challenge in the dental implants market is price competition.

Even premium manufacturers are being forced to adjust pricing strategies as value and discount brands expand globally. Many emerging markets cannot absorb large price increases, placing downward pressure on the average selling price (ASP) of implants and abutments.

Despite these constraints, opportunities remain strong.

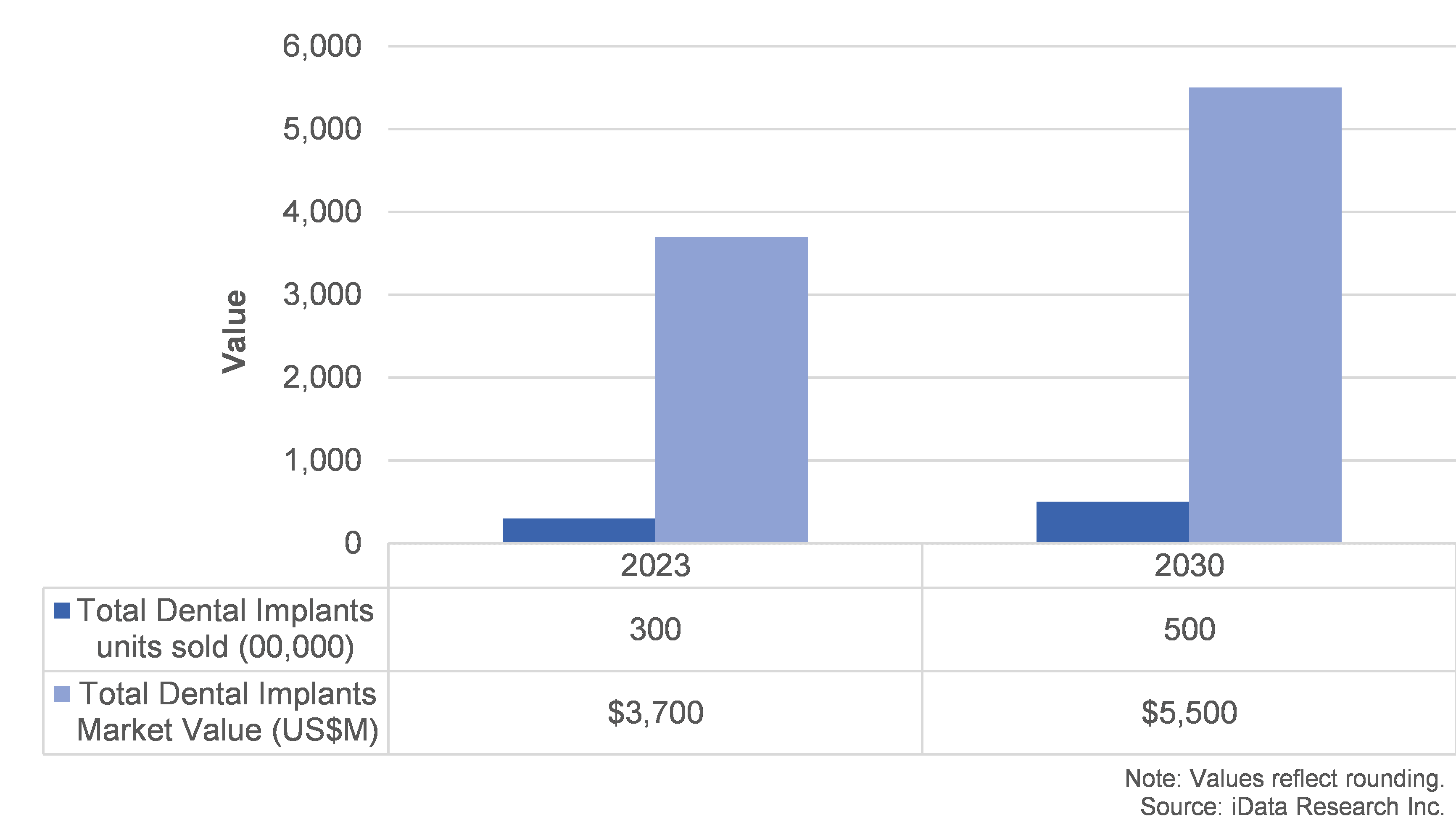

The market for dental implant units sold is projected to rise from 300 million in 2023 to 500 million by 2030, reflecting consistent procedural demand growth. As access to oral health services expands, so does patient education about implant benefits compared to traditional dentures or bridges.

Overall, while price limitations slow revenue growth, the continued expansion of patient access and rising awareness of long-term outcomes will sustain steady market momentum.

Dental Implants Market Segmentation

The full dental implants report suite includes dental implants, final abutments, treatment planning software, and surgical guides. Each category follows distinct trends that contribute to overall market behavior.

Dental Implants

Dental implants are artificial tooth roots that replace missing teeth and preserve jawbone health. They are typically made of titanium.

The dental implant segment represents the majority of total market value and continues to be the strongest growth driver.

Implant types are categorized as premium, value, discount, and mini-implants.

Premium Dental Implants

Premium dental implants are high‑quality versions of regular implants, designed to replace missing teeth with the most natural look and feel possible.

Like standard implants, they use a small screw (usually titanium) placed in the jawbone to act as an artificial root, but premium ones are made with superior materials, advanced designs, and often placed using more precise technology.

Premium implants remain dominant in high-income regions but face growing competition from value products that balance quality with affordability.

Value Dental Implants

Value dental implants are the affordable option, using simpler materials or techniques to restore chewing and appearance at a lower cost.

Discount Dental Implants

Discount dental implants push the price down further, often through special deals or budget‑focused clinics, but may come with fewer choices, less customization, or shorter warranties.

Mini Dental Implants

Mini dental implants are smaller, less invasive versions, placed quickly and often used when there isn’t enough bone for a full implant or to stabilize dentures.

They heal faster and are practical for lighter use, but because of their size, they aren’t as strong or long‑lasting as full implants, more like a compact car that’s easy to handle but not built for heavy loads.

Mini-implants, usually ≤ 2.8 mm in diameter, are gaining popularity for smaller prosthetic needs and cost-sensitive patients.

Final Abutments

Final dental abutments are the permanent connectors that link the implant screw in the jaw to the visible crown.

Unlike temporary abutments used during healing, these are custom‑fit for long‑term stability, comfort, and a natural bite, essentially the finished piece that makes the implant system complete.

They can be made from strong titanium or tooth‑colored zirconia, depending on whether strength or appearance is the priority. Once placed, the crown is attached on top, so the implant looks and works like a real tooth, ready for everyday use.

The final abutment market is smaller in value but growing slightly faster than implants themselves.

Abutment adoption rates are climbing as more practitioners incorporate custom CAD/CAM designs for aesthetic precision and efficient workflows.

Surgical Guides and Planning Software

The surgical guide and treatment planning software segment has become one of the fastest-growing parts of the dental implants market.

Surgical guides allow implantologists to plan implant positioning virtually, ensuring the optimal angle and depth before any procedure begins. This not only increases procedural safety but also helps minimize post-operative complications.

Modern software integrates 3D imaging, cone beam CT data, and intraoral scans to create precise digital plans.

These programs are often sold as part of bundled packages with implants and abutments, especially from leading brands like Straumann, Dentsply Sirona, and Envista, adding value across the treatment pathway.

In recent years, the popularity of guided surgery has surged across dental schools and DSOs, solidifying it as a standard of care in implantology.

As digital scanners and chairside milling units become more affordable, smaller clinics are beginning to adopt these systems as well.

The trend supports a broader movement toward digital dentistry, where planning software and surgical guides help define what the best dental implant procedures look like in practice: efficient, precise, and patient-centered.

Key Dental Implants Market Drivers

These include the rising demand for aesthetics, improved healthcare access, evolving insurance coverage, and rapid technological innovation.

Together, they’re making the best dental implants more accessible and attractive to patients worldwide.

Rising Demand for Aesthetic and Functional Restorations

Patients increasingly view dental implants as the gold standard for replacing missing teeth because they look and function like natural teeth.

Beyond appearance, implants preserve jawbone density and prevent bone atrophy, addressing both aesthetic and functional needs. As awareness of these benefits grows, more patients are choosing implants over bridges or removable dentures.

The demand for aesthetic implant dentistry is especially strong in urban centers and aging populations where disposable incomes are rising.

Expanding Access and Reimbursement Policies

In several countries, public and private insurers are beginning to provide limited coverage for implant procedures. While the level of reimbursement remains modest, the presence of any financial support significantly increases adoption.

Governments in parts of Western Europe and Asia are integrating implantology into broader oral health initiatives. As these policies expand, patients who once considered implants unaffordable are reentering the market.

This dynamic makes reimbursement expansion one of the most impactful long-term growth drivers for the dental implants market.

Efficiency and Precision through CAD/CAM

Technological efficiency is transforming how implants are manufactured and placed.

Computer-aided design and manufacturing (CAD/CAM) technologies have streamlined the production of custom final abutments, improving accuracy and reducing procedural times.

Clinics can now fabricate individualized components with near-perfect precision, minimizing chair time and improving patient satisfaction.

The shift to CAD/CAM workflows has also reduced costs for dental labs, enabling smaller practices to offer high-quality implant services.

Best Dental Implants Companies in 2025

Straumann Group

Straumann Group remains the undisputed leader in the global dental implants and final abutments market. The company’s strength lies in its comprehensive portfolio that covers every major price segment. Straumann dominates the premium implant segment, driven by its long-standing reputation for clinical reliability, precision engineering, and research-backed outcomes.

Its subsidiary Neodent plays a pivotal role in Straumann’s success, giving the group a strong foothold in the value implant segment, one of the fastest-growing areas globally.

This strategy allows Straumann to reach both high-income markets and cost-sensitive regions without diluting its brand.

The company’s acquisition-focused growth model and integration of digital workflows position it as a benchmark for the best dental implant systems in 2025.

Envista Holdings Corporation

Envista holds the second-largest position and stands out for its strategic balance between product diversity and digital innovation. Through well-known brands such as Nobel Biocare and Implant Direct, Envista competes across the premium and value categories. While the company doesn’t dominate a single niche, its broad product mix and strong DSO partnerships make it highly resilient.

Roughly 40% of Envista’s total revenue stems from implant sales, reflecting its deep commitment to this sector.

Since its 2019 spin-off from Danaher, Envista has focused on operational independence and digital growth. Its strength lies in integrating implant solutions with diagnostic imaging and software, key areas that define the modern dental implants market.

As demand for efficiency and affordability grows, Envista’s product alignment positions it for above-average growth through 2030.

Dentsply Sirona

Dentsply Sirona ranks third among the major global players, offering a wide spectrum of implant and prosthetic solutions.

The company is particularly well positioned in surgical guides, digital planning software, and CAD/CAM workflows, giving it a technological edge. Its value-oriented brand, MIS Implants, helps capture the price-sensitive portion of the market, especially in emerging economies.

The company’s innovation pipeline remains active, launching around 30 new dental products each year, many of which integrate digital tools with implant systems.

This strategy strengthens its standing among clinicians seeking efficient workflows and reliable outcomes. With a diverse range of offerings, Dentsply Sirona continues to compete effectively across both premium and mid-tier price points.

Dental Implants Regional Outlook

Asia-Pacific Dental Implants Market

Asia-Pacific remains the largest regional market in 2023, supported by expanding dental infrastructure and rising disposable incomes.

Countries such as Japan, China, and South Korea continue to adopt the best dental implant technologies due to an increasing middle class and growing awareness of aesthetic treatments.

📌 Learn More About APAC Dental Implant Market Growth

➜ What’s Driving Dental Implant Growth in Asia-Pacific? (Key Trends in 2025)

North America Dental Implants Market

North America is one of the most mature implant markets. The U.S. continues to dominate due to a high number of trained specialists, established implant brands, and steady innovation in CAD/CAM and guided surgery. The market is expected to see healthy growth as dental service organizations (DSOs) expand implant offerings at scale.

📌 Learn More About U.S. Dental Implant Market Growth

➜ Top 7 US Dental Implant Market Leaders: Who’s Winning in a Competitive Market

Western Europe Dental Implants Market

Western Europe remains a cornerstone of the premium implant segment. Germany, Switzerland, and the U.K. maintain strong procedural volumes.

However, pricing pressure from value-oriented imports has slightly constrained revenue growth. Still, established dental systems and patient trust in leading brands maintain Europe’s stability.

Latin America Dental Implants Market

Latin America is expected to be among the fastest-growing regions through 2030. Improved access to dental care and education are fueling patient demand.

Brazil and Mexico lead the region, with both premium and value-tier implants expanding as awareness increases.

Technology and Innovation Shaping the Best Dental Implants

Growth of Digital Workflows

Digital dentistry continues to transform how clinicians plan and place implants. From intraoral scanning to 3D printing of surgical guides, integration of software and hardware has improved precision and patient outcomes.

CAD/CAM Custom Abutments

Customized abutments are growing in use because they eliminate manual adjustments and reduce procedure times. As production costs fall, these abutments are becoming more widely available even in developing markets.

Materials and Mini-Implants

Titanium remains the gold standard, but zirconia and hybrid materials are expanding the best dental implant options for patients with metal sensitivities or specific aesthetic needs. Mini-implants, once a niche product, are gaining wider acceptance for overdenture stabilization and narrow ridge cases.

Dental Implants Insights: How Companies Can Compete

Manufacturers are reshaping their portfolios to align with new pricing realities.

The shift toward value-oriented brands is driving bundling strategies, where premium companies combine implants with abutments, surgical kits, and digital tools to offer comprehensive solutions.

To remain competitive, industry professionals may want to:

- Embrace digital integration: Pair implants with planning software, scanners, and CAD/CAM tools.

- Expand value offerings: Capture emerging markets with mid-tier or mini-implant lines.

- Partner with DSOs and dental labs: Strengthen distribution and procedural adoption.

- Invest in education: Increase clinician awareness of implant advantages through training programs.

The combination of affordability, accessibility, and digital efficiency will define the best dental implant manufacturers over the next decade.

👉 See the Global Dental Implants and Final Abutments Market Report Summary, 2024–2030, to discover more insights.

A Steady Climb Toward Broader Accessibility

The global dental implants market continues to evolve as clinical awareness, affordability, and innovation drive adoption. With demand rising from 300 million units in 2023 to 500 million by 2030, the sector’s outlook remains positive.

Yet, success depends on addressing price sensitivity and ensuring access to care. Premium brands must adapt to the expanding influence of value competitors, while emerging regions stand to benefit from improved healthcare infrastructure and patient education.

The future of the best dental implants lies in balancing quality, cost, and digital integration—making advanced restorative solutions accessible to more patients worldwide.

Turn market painpoints into opportunities

Explore how procedure trends and competitor positioning create clear openings for industry experts in the market.