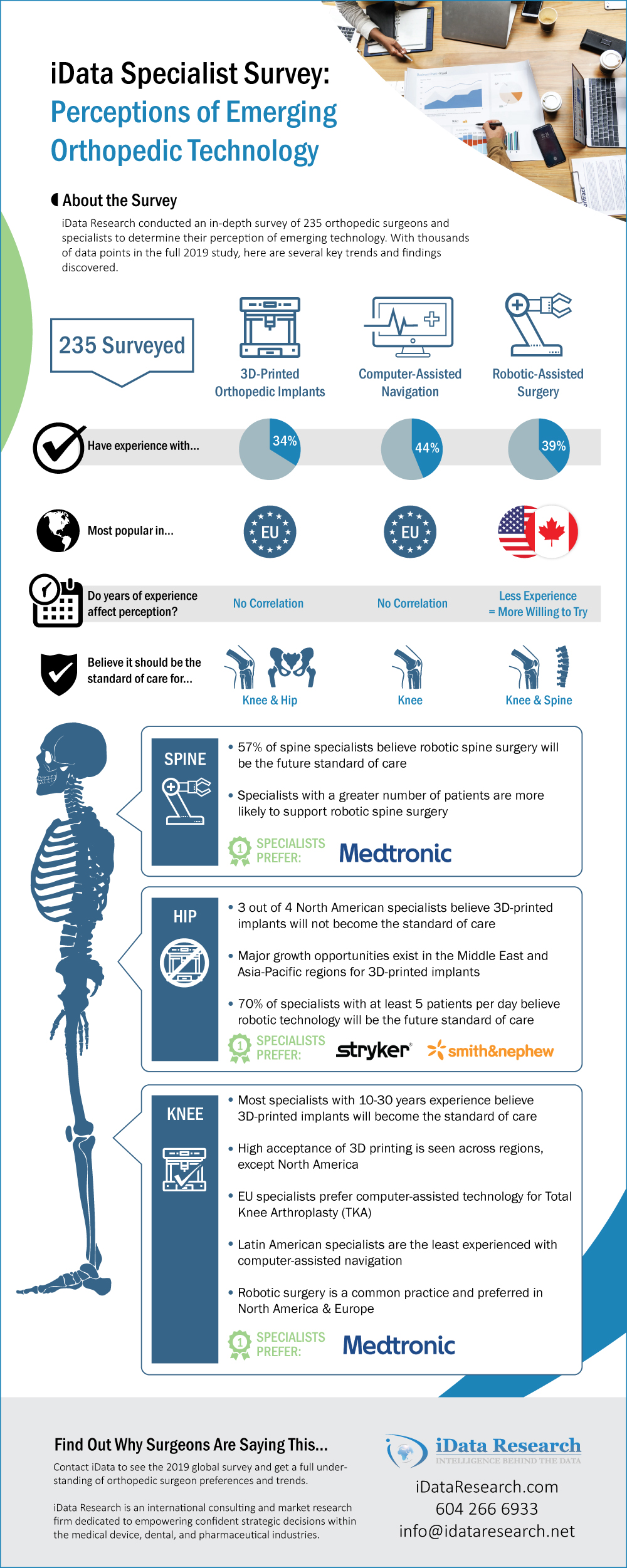

According to a new global survey conducted by iData Research, more than two third of orthopedic physicians surveyed believe that 3D-printed technology will become the standard of care for their orthopedic implant surgeries.

The survey was conducted to collect opinions of orthopedic physicians about the growing markets and trend forecast for the technological innovations in orthopedic surgeries: 3D-printed implants, robotic-assisted-surgery (RAS) and computer-assisted navigation (CAN). Over 200 physicians who practice in multiple segments were surveyed, including multi-specialties, arthroplasty, sports medicine, spine and foot and ankle markets. The survey looks at current market penetration, future growth, top competitors, and opportunities for manufacturers to grow in different regions of these markets.

Among the surgeons surveyed, the most commonly performed surgery with 3D-printed implants was total knee arthroplasty (TKA), and more than 65% put their trust in this technology for the future standard of care. However, 68% of orthopedic physicians believe that 3D-printing technology is not a good choice for spine surgeries. In 2017, the world’s first vertebrae implantation in spine, done by Neurosurgeon Ralph Mobbs who works at The Neurospine Clinic in Sydney, Australia, made spinal experts pay more attention to 3D application in spine surgery. After the first surgery, there are now many articles and research papers which dive into a deeper understanding and hard evidence to prove the utility of 3D-printed implants. Despite all the information on the market which supports the use of 3D technology, the surgeons are still skeptical about its possibility to become a standard of care in spine surgery.

Among the three new technologies studied for orthopedic surgeries, 3D-printed implants are the most commonly used. More than half of the orthopedic surgeons surveyed have performed surgery using 3D-printed implants, while there are only 39% for robotic-assisted surgery and 44% for computer-assisted navigation. 3D-printed implants procedures are commonly practiced by surgeons from the Middle East & Africa and North America; however, there is no strong evidence of brand preference from those surgeons. This indicates that the 3D-printed implant devices market is more accessible for newer entrants in the market.

However, this is not the case in the U.S. market; Stryker is reported to be a top-of-mind manufacturer when 3D implant devices for knee arthroplasty procedures are requested, and Smith & Nephew is acclaimed to be the most popular manufacturer within hip arthroplasty procedures. The overall spinal implants market is led by Medtronic, according to the U.S. Market Report for Spinal Implants conducted by iData Research, creating significant competition for Stryker’s products.

Based on iData’s findings from the survey, the 3D-printing market is expected to grow substantially because the technology is forecasted to become the new standard of care, and the market is not yet dominated by any specific brands, other than in the U.S. market.

To Learn Why Orthopedic Physicians Say this…

If you’re interested in seeing the full survey conducted across 223 orthopedic professionals globally please contact iData Research. This report outlines perceptions and use of 3D-printed implants, robotic surgery trends, computer-assisted navigation trends, top competitors, and the future growth of the market.

Click here to speak to an iData representative today to bring this data and insight to the forefront of your product and marketing strategies.