| Figure 1-1: Interventional Cardiology Device Market Share Ranking by Segment, Global, 2025 (1 of 3) |

| Figure 1‑2: Interventional Cardiology Device Market Share Ranking by Segment, Global, 2025 (2 of 3) |

| Figure 1‑3: Interventional Cardiology Device Market Share Ranking by Segment, Global, 2025 (3 of 3) |

| Figure 1‑4: Companies Researched in This Report (1 of 2) |

| Figure 1‑5: Companies Researched in This Report (2 of 2) |

| Figure 1‑6: Factors Impacting the Interventional Cardiology Device Market by Segment, Global (1 of 3) |

| Figure 1‑7: Factors Impacting the Interventional Cardiology Device Market by Segment, Global (2 of 3) |

| Figure 1‑8: Factors Impacting the Interventional Cardiology Device Market by Segment, Global (3 of 3) |

| Figure 1‑9: Recent Events in the Interventional Cardiology Device Market, Global, 2021 – 2025 (1 of 2) |

| Figure 1‑10: Recent Events in the Interventional Cardiology Device Market, Global, 2021 – 2025 (2 of 2) |

| Figure 1‑11: Interventional Cardiology Device Procedure Segmentation |

| Figure 1‑12: Procedure Codes Investigated |

| Figure 1‑13: Interventional Cardiology Device Market Segmentation |

| Figure 1‑14: Key Report Updates |

| Figure 1‑15: Version History |

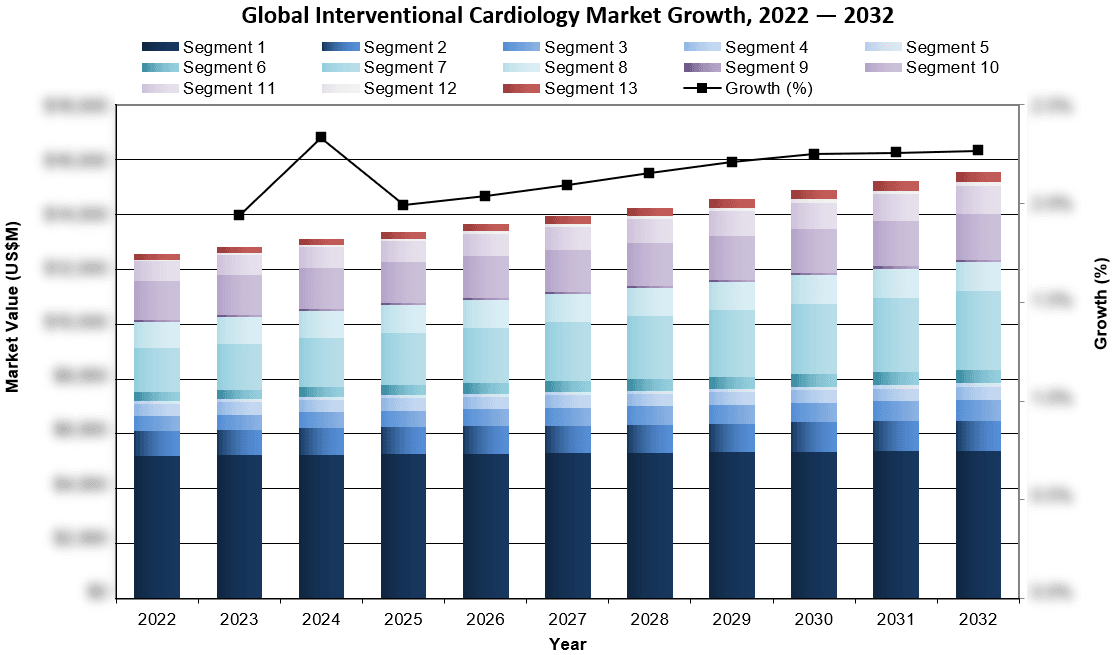

| Figure 3‑1: Interventional Cardiology Device Market by Segment, Global, 2022 – 2032 (US$M) (1 of 2) |

| Figure 3‑2: Interventional Cardiology Device Market by Segment, Global, 2022 – 2032 (US$M) (2 of 2) |

| Figure 3‑3: Interventional Cardiology Device Market by Region, Global, 2022 – 2032 (US$M) |

| Figure 3‑4: Leading Competitors, Interventional Cardiology Device Market by Segment, Global, 2025 (1 of 2) |

| Figure 3‑5: Leading Competitors, Interventional Cardiology Device Market by Segment, Global, 2025 (2 of 2) |

| Figure 4‑1: Coronary Stent Procedure Segmentation |

| Figure 4‑2: Coronary Stent Market Segmentation |

| Figure 4‑3: Coronary Stent Regions Covered, Global (1 of 2) |

| Figure 4‑4: Coronary Stent Regions Covered, Global (2 of 2) |

| Figure 4‑5: Angioplasty/ PCI Procedures by Region, Global, 2022 – 2032 |

| Figure 4‑6: Angioplasty/ PCI Procedures by Country, North America, 2022 – 2032 |

| Figure 4‑7: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 4‑8: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 4‑9: Angioplasty/ PCI Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 4‑10: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 4‑11: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 4‑12: Angioplasty/ PCI Procedures by Country, Middle East, 2022 – 2032 |

| Figure 4‑13: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 4‑14: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 4‑15: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 4‑16: Angioplasty/ PCI Procedures by Country, Africa, 2022 – 2032 |

| Figure 4‑17: Coronary Stent Market by Segment, Global, 2022 – 2032 (US$M) |

| Figure 4‑18: Coronary Stent Market by Region, Global, 2022 – 2032 (US$M) |

| Figure 4‑19: Coronary Stent Market, Global, 2022 – 2032 |

| Figure 4‑20: Units Sold by Region, Coronary Stent Market, Global, 2022 – 2032 |

| Figure 4‑21: Average Selling Price by Region, Coronary Stent Market, Global, 2022 – 2032 (US$) |

| Figure 4‑22: Market Value by Region, Coronary Stent Market, Global, 2022 – 2032 (US$M) |

| Figure 4‑23: Bare-Metal Stent Market, Global, 2022 – 2032 |

| Figure 4‑24: Units Sold by Region, Bare-Metal Stent Market, Global, 2022 – 2032 |

| Figure 4‑25: Average Selling Price by Region, Bare-Metal Stent Market, Global, 2022 – 2032 (US$) |

| Figure 4‑26: Market Value by Region, Bare-Metal Stent Market, Global, 2022 – 2032 (US$M) |

| Figure 4‑27: Drug-Eluting Stent Market, Global, 2022 – 2032 |

| Figure 4‑28: Units Sold by Region, Drug-Eluting Stent Market, Global, 2022 – 2032 |

| Figure 4‑29: Average Selling Price by Region, Drug-Eluting Stent Market, Global, 2022 – 2032 (US$) |

| Figure 4‑30: Market Value by Region, Drug-Eluting Stent Market, Global, 2022 – 2032 (US$M) |

| Figure 4‑31: Leading Competitors, Coronary Stent Market, Global, 2025 |

| Figure 5‑1: Coronary Balloon Catheter Procedure Segmentation |

| Figure 5‑2: Coronary Balloon Catheter Market Segmentation |

| Figure 5‑3: Coronary Balloon Catheter Regions Covered, Global (1 of 2) |

| Figure 5‑4: Coronary Balloon Catheter Regions Covered, Global (2 of 2) |

| Figure 5‑5: Angioplasty/ PCI Procedures by Region, Global, 2022 – 2032 |

| Figure 5‑6: Angioplasty/ PCI Procedures by Country, North America, 2022 – 2032 |

| Figure 5‑7: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 5‑8: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 5‑9: Angioplasty/ PCI Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 5‑10: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 5‑11: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 5‑12: Angioplasty/ PCI Procedures by Country, Middle East, 2022 – 2032 |

| Figure 5‑13: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 5‑14: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 5‑15: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 5‑16: Angioplasty/ PCI Procedures by Country, Africa, 2022 – 2032 |

| Figure 5‑17: Coronary Balloon Catheter Market by Segment, Global, 2022 – 2032 (US$M) |

| Figure 5‑18: Coronary Balloon Catheter Market by Region, Global, 2022 – 2032 (US$M) |

| Figure 5‑19: Coronary Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑20: Units Sold by Region, Coronary Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑21: Average Selling Price by Region, Coronary Balloon Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 5‑22: Market Value by Region, Coronary Balloon Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 5‑23: PTCA Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑24: Units Sold by Region, PTCA Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑25: Average Selling Price by Region, PTCA Balloon Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 5‑26: Market Value by Region, PTCA Balloon Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 5‑27: Specialty Balloon Catheter Market by Segment, Global, 2022 – 2032 (US$M) |

| Figure 5‑28: Total Specialty Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑29: Units Sold by Region, Specialty Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑30: Average Selling Price by Region, Specialty Balloon Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 5‑31: Market Value by Region, Specialty Balloon Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 5‑32: Drug-Coated Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑33: Units Sold by Region, Drug-Coated Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑34: Average Selling Price by Region, Drug-Coated Balloon Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 5‑35: Market Value by Region, Drug-Coated Balloon Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 5‑36: Other Specialty Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑37: Units Sold by Region, Other Specialty Balloon Catheter Market, Global, 2022 – 2032 |

| Figure 5‑38: Average Selling Price by Region, Other Specialty Balloon Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 5‑39: Market Value by Region, Other Specialty Balloon Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 5‑40: Leading Competitors, Coronary Balloon Catheter Market, Global, 2025 |

| Figure 6‑1: Interventional Coronary Catheter Procedure Segmentation |

| Figure 6‑2: Interventional Coronary Catheter Market Segmentation |

| Figure 6‑3: Interventional Coronary Catheter Regions Covered, Global (1 of 2) |

| Figure 6‑4: Interventional Coronary Catheter Regions Covered, Global (2 of 2) |

| Figure 6‑5: Angioplasty/ PCI Procedures by Region, Global, 2022 – 2032 |

| Figure 6‑6: Angioplasty/ PCI Procedures by Country, North America, 2022 – 2032 |

| Figure 6‑7: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 6‑8: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 6‑9: Angioplasty/ PCI Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 6‑10: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 6‑11: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 6‑12: Angioplasty/ PCI Procedures by Country, Middle East, 2022 – 2032 |

| Figure 6‑13: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 6‑14: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 6‑15: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 6‑16: Angioplasty/ PCI Procedures by Country, Africa, 2022 – 2032 |

| Figure 6‑17: Interventional Coronary Catheter Market by Segment, Global, 2022 – 2032 (US$M) |

| Figure 6‑18: Interventional Coronary Catheter Market by Region, Global, 2022 – 2032 (US$M) |

| Figure 6‑19: Interventional Coronary Catheter Market, Global, 2022 – 2032 |

| Figure 6‑20: Units Sold by Region, Interventional Coronary Catheter Market, Global, 2022 – 2032 |

| Figure 6‑21: Average Selling Price by Region, Interventional Coronary Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 6‑22: Market Value by Region, Interventional Coronary Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 6‑23: Extension Guide Catheter Market, Global, 2022 – 2032 |

| Figure 6‑24: Units Sold by Region, Extension Guide Catheter Market, Global, 2022 – 2032 |

| Figure 6‑25: Average Selling Price by Region, Extension Guide Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 6‑26: Market Value by Region, Extension Guide Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 6‑27: Guiding Catheter Market, Global, 2022 – 2032 |

| Figure 6‑28: Units Sold by Region, Guiding Catheter Market, Global, 2022 – 2032 |

| Figure 6‑29: Average Selling Price by Region, Guiding Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 6‑30: Market Value by Region, Guiding Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 6‑31: Leading Competitors, Interventional Coronary Catheter Market, Global, 2025 |

| Figure 7‑1: Interventional Coronary Guidewire Procedure Segmentation |

| Figure 7‑2: Interventional Coronary Guidewire Regions Covered, Global (1 of 2) |

| Figure 7‑3: Interventional Coronary Guidewire Regions Covered, Global (2 of 2) |

| Figure 7‑4: Angioplasty/ PCI Procedures by Region, Global, 2022 – 2032 |

| Figure 7‑5: Angioplasty/ PCI Procedures by Country, North America, 2022 – 2032 |

| Figure 7‑6: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 7‑7: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 7‑8: Angioplasty/ PCI Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 7‑9: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 7‑10: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 7‑11: Angioplasty/ PCI Procedures by Country, Middle East, 2022 – 2032 |

| Figure 7‑12: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 7‑13: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 7‑14: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 7‑15: Angioplasty/ PCI Procedures by Country, Africa, 2022 – 2032 |

| Figure 7‑16: Interventional Coronary Guidewire Market, Global, 2022 – 2032 |

| Figure 7‑17: Units Sold by Region, Interventional Coronary Guidewire Market, Global, 2022 – 2032 |

| Figure 7‑18: Average Selling Price by Region, Interventional Coronary Guidewire Market, Global, 2022 – 2032 (US$) |

| Figure 7‑19: Market Value by Region, Interventional Coronary Guidewire Market, Global, 2022 – 2032 (US$M) |

| Figure 7‑20: Leading Competitors, Interventional Coronary Guidewire Market, Global, 2025 |

| Figure 8‑1: Coronary Embolic Protection Device Regions Covered, Global (1 of 2) |

| Figure 8‑2: Coronary Embolic Protection Device Regions Covered, Global (2 of 2) |

| Figure 8‑3: Coronary Embolic Protection Device Market, Global, 2022 – 2032 |

| Figure 8‑4: Units Sold by Region, Coronary Embolic Protection Device Market, Global, 2022 – 2032 |

| Figure 8‑5: Average Selling Price by Region, Coronary Embolic Protection Device Market, Global, 2022 – 2032 (US$) |

| Figure 8‑6: Market Value by Region, Coronary Embolic Protection Device Market, Global, 2022 – 2032 (US$M) |

| Figure 8‑7: Leading Competitors, Coronary Embolic Protection Device Market, Global, 2025 |

| Figure 9‑1: Coronary Atherectomy Procedure Segmentation |

| Figure 9‑2: Coronary Atherectomy Market Segmentation |

| Figure 9‑3: Coronary Atherectomy Regions Covered, Global (1 of 2) |

| Figure 9‑4: Coronary Atherectomy Regions Covered, Global (2 of 2) |

| Figure 9‑5: Coronary Atherectomy Procedures by Region, Global, 2022 – 2032 |

| Figure 9‑6: Coronary Atherectomy Procedures by Country, North America, 2022 – 2032 |

| Figure 9‑7: Coronary Atherectomy Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 9‑8: Coronary Atherectomy Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 9‑9: Coronary Atherectomy Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 9‑10: Coronary Atherectomy Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 9‑11: Coronary Atherectomy Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 9‑12: Coronary Atherectomy Procedures by Country, Middle East, 2022 – 2032 |

| Figure 9‑13: Coronary Atherectomy Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 9‑14: Coronary Atherectomy Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 9‑15: Coronary Atherectomy Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 9‑16: Coronary Atherectomy Procedures by Country, Africa, 2022 – 2032 |

| Figure 9‑17: Coronary Atherectomy Market by Segment, Global, 2022 – 2032 (US$M) |

| Figure 9‑18: Coronary Atherectomy Market by Region, Global, 2022 – 2032 (US$M) |

| Figure 9‑19: Coronary Atherectomy Market, Global, 2022 – 2032 |

| Figure 9‑20: Units Sold by Region, Coronary Atherectomy Market, Global, 2022 – 2032 |

| Figure 9‑21: Average Selling Price by Region, Coronary Atherectomy Market, Global, 2022 – 2032 (US$) |

| Figure 9‑22: Market Value by Region, Coronary Atherectomy Market, Global, 2022 – 2032 (US$M) |

| Figure 9‑23: Mechanical Atherectomy Market, Global, 2022 – 2032 |

| Figure 9‑24: Units Sold by Region, Mechanical Atherectomy Market, Global, 2022 – 2032 |

| Figure 9‑25: Average Selling Price by Region, Mechanical Atherectomy Market, Global, 2022 – 2032 (US$) |

| Figure 9‑26: Market Value by Region, Mechanical Atherectomy Market, Global, 2022 – 2032 (US$M) |

| Figure 9‑27: Laser Atherectomy Market, Global, 2022 – 2032 |

| Figure 9‑28: Units Sold by Region, Laser Atherectomy Market, Global, 2022 – 2032 |

| Figure 9‑29: Average Selling Price by Region, Laser Atherectomy Market, Global, 2022 – 2032 (US$) |

| Figure 9‑30: Market Value by Region, Laser Atherectomy Market, Global, 2022 – 2032 (US$M) |

| Figure 9‑31: Leading Competitors, Coronary Atherectomy Market, Global, 2025 |

| Figure 10‑1: Intravascular Lithotripsy Device Procedure Segmentation |

| Figure 10‑2: Intravascular Lithotripsy Device Regions Covered, Global (1 of 2) |

| Figure 10‑3: Intravascular Lithotripsy Device Regions Covered, Global (2 of 2) |

| Figure 10‑4: Intravascular Lithotripsy Procedures by Region, Global, 2022 – 2032 |

| Figure 10‑5: Intravascular Lithotripsy Procedures by Country, North America, 2022 – 2032 |

| Figure 10‑6: Intravascular Lithotripsy Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 10‑7: Intravascular Lithotripsy Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 10‑8: Intravascular Lithotripsy Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 10‑9: Intravascular Lithotripsy Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 10‑10: Intravascular Lithotripsy Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 10‑11: Intravascular Lithotripsy Procedures by Country, Middle East, 2022 – 2032 |

| Figure 10‑12: Intravascular Lithotripsy Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 10‑13: Intravascular Lithotripsy Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 10‑14: Intravascular Lithotripsy Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 10‑15: Intravascular Lithotripsy Procedures by Country, Africa, 2022 – 2032 |

| Figure 10‑16: Intravascular Lithotripsy Device Market, Global, 2022 – 2032 |

| Figure 10‑17: Units Sold by Region, Intravascular Lithotripsy Device Market, Global, 2022 – 2032 |

| Figure 10‑18: Average Selling Price by Region, Intravascular Lithotripsy Device Market, Global, 2022 – 2032 (US$) |

| Figure 10‑19: Market Value by Region, Intravascular Lithotripsy Device Market, Global, 2022 – 2032 (US$M) |

| Figure 10‑20: Leading Competitors, Intravascular Lithotripsy Device Market, Global, 2025 |

| Figure 11‑1: Coronary Introducer Sheath Procedure Segmentation |

| Figure 11‑2: Coronary Introducer Sheath Regions Covered, Global (1 of 2) |

| Figure 11‑3: Coronary Introducer Sheath Regions Covered, Global (2 of 2) |

| Figure 11‑4: Angioplasty/ PCI Procedures by Region, Global, 2022 – 2032 |

| Figure 11‑5: Angioplasty/ PCI Procedures by Country, North America, 2022 – 2032 |

| Figure 11‑6: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 11‑7: Angioplasty/ PCI Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 11‑8: Angioplasty/ PCI Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 11‑9: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 11‑10: Angioplasty/ PCI Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 11‑11: Angioplasty/ PCI Procedures by Country, Middle East, 2022 – 2032 |

| Figure 11‑12: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 11‑13: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 11‑14: Angioplasty/ PCI Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 11‑15: Angioplasty/ PCI Procedures by Country, Africa, 2022 – 2032 |

| Figure 11‑16: Coronary Introducer Sheath Market, Global, 2022 – 2032 |

| Figure 11‑17: Units Sold by Region, Coronary Introducer Sheath Market, Global, 2022 – 2032 |

| Figure 11‑18: Average Selling Price by Region, Coronary Introducer Sheath Market, Global, 2022 – 2032 (US$) |

| Figure 11‑19: Market Value by Region, Coronary Introducer Sheath Market, Global, 2022 – 2032 (US$M) |

| Figure 11‑20: Leading Competitors, Coronary Introducer Sheath Market, Global, 2025 |

| Figure 12‑1: Coronary Chronic Total Occlusion Guidewire Regions Covered, Global (1 of 2) |

| Figure 12‑2: Coronary Chronic Total Occlusion Guidewire Regions Covered, Global (2 of 2) |

| Figure 12‑3: Coronary Chronic Total Occlusion Guidewire Market, Global, 2022 – 2032 |

| Figure 12‑4: Units Sold by Region, Coronary Chronic Total Occlusion Guidewire Market, Global, 2022 – 2032 |

| Figure 12‑5: Average Selling Price by Region, Coronary Chronic Total Occlusion Guidewire Market, Global, 2022 – 2032 (US$) |

| Figure 12‑6: Market Value by Region, Coronary Chronic Total Occlusion Guidewire Market, Global, 2022 – 2032 (US$M) |

| Figure 12‑7: Leading Competitors, Coronary Chronic Total Occlusion Guidewire Market, Global, 2025 |

| Figure 13‑1: Coronary Vascular Closure Device Procedure Segmentation |

| Figure 13‑2: Coronary Vascular Closure Device Market Segmentation |

| Figure 13‑3: Coronary Vascular Closure Device Regions Covered, Global (1 of 2) |

| Figure 13‑4: Coronary Vascular Closure Device Regions Covered, Global (2 of 2) |

| Figure 13‑5: Catheterization Procedures by Region, Global, 2022 – 2032 |

| Figure 13‑6: Catheterization Procedures by Country, North America, 2022 – 2032 |

| Figure 13‑7: Catheterization Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 13‑8: Catheterization Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 13‑9: Catheterization Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 13‑10: Catheterization Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 13‑11: Catheterization Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 13‑12: Catheterization Procedures by Country, Middle East, 2022 – 2032 |

| Figure 13‑13: Catheterization Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 13‑14: Catheterization Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 13‑15: Catheterization Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 13‑16: Catheterization Procedures by Country, Africa, 2022 – 2032 |

| Figure 13‑17: Coronary Vascular Closure Device Market by Segment, Global, 2022 – 2032 (US$M) |

| Figure 13‑18: Coronary Vascular Closure Device Market by Region, Global, 2022 – 2032 (US$M) |

| Figure 13‑19: Coronary Vascular Closure Device Market, Global, 2022 – 2032 |

| Figure 13‑20: Units Sold by Region, Coronary Vascular Closure Device Market, Global, 2022 – 2032 |

| Figure 13‑21: Average Selling Price by Region, Coronary Vascular Closure Device Market, Global, 2022 – 2032 (US$) |

| Figure 13‑22: Market Value by Region, Coronary Vascular Closure Device Market, Global, 2022 – 2032 (US$M) |

| Figure 13‑23: Invasive VCD Market, Global, 2022 – 2032 |

| Figure 13‑24: Units Sold by Region, Invasive VCD Market, Global, 2022 – 2032 |

| Figure 13‑25: Average Selling Price by Region, Invasive VCD Market, Global, 2022 – 2032 (US$) |

| Figure 13‑26: Market Value by Region, Invasive VCD Market, Global, 2022 – 2032 (US$M) |

| Figure 13‑27: Non-Invasive VCD Market, Global, 2022 – 2032 |

| Figure 13‑28: Units Sold by Region, Non-Invasive VCD Market, Global, 2022 – 2032 |

| Figure 13‑29: Average Selling Price by Region, Non-Invasive VCD Market, Global, 2022 – 2032 (US$) |

| Figure 13‑30: Market Value by Region, Non-Invasive VCD Market, Global, 2022 – 2032 (US$M) |

| Figure 13‑31: Leading Competitors, Coronary Vascular Closure Device Market, Global, 2025 |

| Figure 14‑1: Diagnostic Catheter and Guidewire Procedure Segmentation |

| Figure 14‑2: Diagnostic Catheter and Guidewire Market Segmentation |

| Figure 14‑3: XX Regions Covered, Global (1 of 2) |

| Figure 14‑4: XX Regions Covered, Global (2 of 2) |

| Figure 14‑5: Diagnostic Catheter and Guidewire Procedures by Segment, Global, 2022 – 2032 |

| Figure 14‑6: Diagnostic Catheter and Guidewire Procedures by Region, Global, 2022 – 2032 |

| Figure 14‑7: Diagnostic Catheter and Guidewire Procedures by Country, North America, 2022 – 2032 |

| Figure 14‑8: Diagnostic Catheter and Guidewire Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 14‑9: Diagnostic Catheter and Guidewire Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 14‑10: Diagnostic Catheter and Guidewire Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 14‑11: Diagnostic Catheter and Guidewire Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 14‑12: Diagnostic Catheter and Guidewire Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 14‑13: Diagnostic Catheter and Guidewire Procedures by Country, Middle East, 2022 – 2032 |

| Figure 14‑14: Diagnostic Catheter and Guidewire Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 14‑15: Diagnostic Catheter and Guidewire Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 14‑16: Diagnostic Catheter and Guidewire Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 14‑17: Diagnostic Catheter and Guidewire Procedures by Country, Africa, 2022 – 2032 |

| Figure 14‑18: Angiography Procedures by Region, Global, 2022 – 2032 |

| Figure 14‑19: Angiography Procedures by Country, North America, 2022 – 2032 |

| Figure 14‑20: Angiography Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 14‑21: Angiography Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 14‑22: Angiography Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 14‑23: Angiography Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 14‑24: Angiography Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 14‑25: Angiography Procedures by Country, Middle East, 2022 – 2032 |

| Figure 14‑26: Angiography Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 14‑27: Angiography Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 14‑28: Angiography Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 14‑29: Angiography Procedures by Country, Africa, 2022 – 2032 |

| Figure 14‑30: FFR Procedures by Region, Global, 2022 – 2032 |

| Figure 14‑31: FFR Procedures by Country, North America, 2022 – 2032 |

| Figure 14‑32: FFR Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 14‑33: FFR Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 14‑34: FFR Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 14‑35: FFR Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 14‑36: FFR Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 14‑37: FFR Procedures by Country, Middle East, 2022 – 2032 |

| Figure 14‑38: FFR Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 14‑39: FFR Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 14‑40: FFR Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 14‑41: FFR Procedures by Country, Africa, 2022 – 2032 |

| Figure 14‑42: Diagnostic Catheter and Guidewire Market by Segment, Global, 2022 – 2032 (US$M) |

| Figure 14‑43: Diagnostic Catheter and Guidewire Market by Region, Global, 2022 – 2032 (US$M) |

| Figure 14‑44: Diagnostic Catheter and Guidewire Market, Global, 2022 – 2032 |

| Figure 14‑45: Units Sold by Region, Diagnostic Catheter and Guidewire Market, Global, 2022 – 2032 |

| Figure 14‑46: Average Selling Price by Region, Diagnostic Catheter and Guidewire Market, Global, 2022 – 2032 (US$) |

| Figure 14‑47: Market Value by Region, Diagnostic Catheter and Guidewire Market, Global, 2022 – 2032 (US$M) |

| Figure 14‑48: Interventional Diagnostic Catheter Market, Global, 2022 – 2032 |

| Figure 14‑49: Units Sold by Region, Interventional Diagnostic Catheter Market, Global, 2022 – 2032 |

| Figure 14‑50: Average Selling Price by Region, Interventional Diagnostic Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 14‑51: Market Value by Region, Interventional Diagnostic Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 14‑52: Interventional Diagnostic Guidewire Market, Global, 2022 – 2032 |

| Figure 14‑53: Units Sold by Region, Interventional Diagnostic Guidewire Market, Global, 2022 – 2032 |

| Figure 14‑54: Average Selling Price by Region, Interventional Diagnostic Guidewire Market, Global, 2022 – 2032 (US$) |

| Figure 14‑55: Market Value by Region, Interventional Diagnostic Guidewire Market, Global, 2022 – 2032 (US$M) |

| Figure 14‑56: Fractional Flow Reserve Guidewire Market, Global, 2022 – 2032 |

| Figure 14‑57: Units Sold by Region, Fractional Flow Reserve Guidewire Market, Global, 2022 – 2032 |

| Figure 14‑58: Average Selling Price by Region, Fractional Flow Reserve Guidewire Market, Global, 2022 – 2032 (US$) |

| Figure 14‑59: Market Value by Region, Fractional Flow Reserve Guidewire Market, Global, 2022 – 2032 (US$M) |

| Figure 14‑60: Leading Competitors, Diagnostic Catheter and Guidewire Market, Global, 2025 |

| Figure 15‑1: Optical Coherence Tomography Catheter Procedure Segmentation |

| Figure 15‑2: Optical Coherence Tomography Catheter Regions Covered, Global (1 of 2) |

| Figure 15‑3: Optical Coherence Tomography Catheter Regions Covered, Global (2 of 2) |

| Figure 15‑4: Optical Coherence Tomography Procedures by Region, Global, 2022 – 2032 |

| Figure 15‑5: Optical Coherence Tomography Procedures by Country, North America, 2022 – 2032 |

| Figure 15‑6: Optical Coherence Tomography Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 15‑7: Optical Coherence Tomography Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 15‑8: Optical Coherence Tomography Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 15‑9: Optical Coherence Tomography Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 15‑10: Optical Coherence Tomography Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 15‑11: Optical Coherence Tomography Procedures by Country, Middle East, 2022 – 2032 |

| Figure 15‑12: Optical Coherence Tomography Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 15‑13: Optical Coherence Tomography Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 15‑14: Optical Coherence Tomography Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 15‑15: Optical Coherence Tomography Procedures by Country, Africa, 2022 – 2032 |

| Figure 15‑16: Optical Coherence Tomography Catheter Market, Global, 2022 – 2032 |

| Figure 15‑17: Units Sold by Region, Optical Coherence Tomography Catheter Market, Global, 2022 – 2032 |

| Figure 15‑18: Average Selling Price by Region, Optical Coherence Tomography Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 15‑19: Market Value by Region, Optical Coherence Tomography Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 15‑20: Leading Competitors, Optical Coherence Tomography Catheter Market, Global, 2025 |

| Figure 16‑1: Intravascular Ultrasound Catheter Procedure Segmentation |

| Figure 16‑2: Intravascular Ultrasound Catheter Regions Covered, Global (1 of 2) |

| Figure 16‑3: Intravascular Ultrasound Catheter Regions Covered, Global (2 of 2) |

| Figure 16‑4: Intravascular Ultrasound Procedures by Region, Global, 2022 – 2032 |

| Figure 16‑5: Intravascular Ultrasound Procedures by Country, North America, 2022 – 2032 |

| Figure 16‑6: Intravascular Ultrasound Procedures by Country, Latin America, 2022 – 2032 (1 of 2) |

| Figure 16‑7: Intravascular Ultrasound Procedures by Country, Latin America, 2022 – 2032 (2 of 2) |

| Figure 16‑8: Intravascular Ultrasound Procedures by Country, Western Europe, 2022 – 2032 |

| Figure 16‑9: Intravascular Ultrasound Procedures by Country, Central & Eastern Europe, 2022 – 2032 (1 of 2) |

| Figure 16‑10: Intravascular Ultrasound Procedures by Country, Central & Eastern Europe, 2022 – 2032 (2 of 2) |

| Figure 16‑11: Intravascular Ultrasound Procedures by Country, Middle East, 2022 – 2032 |

| Figure 16‑12: Intravascular Ultrasound Procedures by Country, Asia-Pacific, 2022 – 2032 (1 of 3) |

| Figure 16‑13: Intravascular Ultrasound Procedures by Country, Asia-Pacific, 2022 – 2032 (2 of 3) |

| Figure 16‑14: Intravascular Ultrasound Procedures by Country, Asia-Pacific, 2022 – 2032 (3 of 3) |

| Figure 16‑15: Intravascular Ultrasound Procedures by Country, Africa, 2022 – 2032 |

| Figure 16‑16: Intravascular Ultrasound Catheter Market, Global, 2022 – 2032 |

| Figure 16‑17: Units Sold by Region, Intravascular Ultrasound Catheter Market, Global, 2022 – 2032 |

| Figure 16‑18: Average Selling Price by Region, Intravascular Ultrasound Catheter Market, Global, 2022 – 2032 (US$) |

| Figure 16‑19: Market Value by Region, Intravascular Ultrasound Catheter Market, Global, 2022 – 2032 (US$M) |

| Figure 16‑20: Leading Competitors, Intravascular Ultrasound Catheter Market, Global, 2025 |