| List of Figures |

| Figure 1‑1: Vascular Access Devices and Accessories Market Share Ranking by Segment, Europe, 2022 (1 of 3) |

5 |

| Figure 1‑2: Vascular Access Devices and Accessories Market Share Ranking by Segment, Europe, 2022 (2 of 3) |

5 |

| Figure 1‑3: Vascular Access Devices and Accessories Market Share Ranking by Segment, Europe, 2022 (3 of 3) |

5 |

| Figure 1‑4: Companies Researched in This Report (1 of 2) |

6 |

| Figure 1‑5: Companies Researched in This Report (2 of 2) |

7 |

| Figure 1‑6: Factors Impacting the Vascular Access Devices and Accessories Market by Segment, Europe (1 of 3) |

8 |

| Figure 1‑7: Factors Impacting the Vascular Access Devices and Accessories Market by Segment, Europe (2 of 3) |

9 |

| Figure 1‑8: Factors Impacting the Vascular Access Devices and Accessories Market by Segment, Europe (3 of 3) |

10 |

| Figure 1‑9: Recent Events in the Vascular Access Devices and Accessories Market, Europe, 2019 – 2023 (1 of 2) |

11 |

| Figure 1‑10: Recent Events in the Vascular Access Devices and Accessories Market, Europe, 2019 – 2023 (2 of 2) |

12 |

| Figure 1‑11: Vascular Access Devices and Accessories Procedures Covered, Europe |

13 |

| Figure 1‑12: Vascular Access Devices and Accessories Markets Covered, Europe (1 of 4) |

14 |

| Figure 1‑13: Vascular Access Devices and Accessories Markets Covered, Europe (2 of 4) |

15 |

| Figure 1‑14: Vascular Access Devices and Accessories Markets Covered, Europe (3 of 4) |

16 |

| Figure 1‑15: Vascular Access Devices and Accessories Markets Covered, Europe (4 of 4) |

17 |

| Figure 1‑16: Key Report Updates (1 of 2) |

18 |

| Figure 1‑17: Key Report Updates (2 of 2) |

19 |

| Figure 1‑18: Version History |

20 |

| Figure 2‑1: Vascular Access Devices and Accessories Market by Segment, Worst Case Scenario, Europe, 2019 – 2029 (€M) (1 of 3) |

38 |

| Figure 2‑2: Vascular Access Devices and Accessories Market by Segment, Worst Case Scenario, Europe, 2019 – 2029 (€M) (2 of 3) |

39 |

| Figure 2‑3: Vascular Access Devices and Accessories Market by Segment, Worst Case Scenario, Europe, 2019 – 2029 (€M) (3 of 3) |

40 |

| Figure 2‑4: Vascular Access Devices and Accessories Vascular Access Devices and Accessories Market by Segment, Base Case Scenario, Europe, 2019 – 2029 (€M) (1 of 3) |

41 |

| Figure 2‑5: Vascular Access Devices and Accessories Market by Segment, Base Case Scenario, Europe, 2019 – 2029 (€M) (2 of 3) |

42 |

| Figure 2‑6: Vascular Access Devices and Accessories Market by Segment, Base Case Scenario, Europe, 2019 – 2029 (€M) (3 of 3) |

43 |

| Figure 2‑7: Vascular Access Devices and Accessories Market by Segment, Best Case Scenario, Europe, 2019 – 2029 (€M) (1 of 3) |

44 |

| Figure 2‑8: Vascular Access Devices and Accessories Market by Segment, Best Case Scenario, Europe, 2019 – 2029 (€M) (2 of 3) |

45 |

| Figure 2‑9: Vascular Access Devices and Accessories Market by Segment, Best Case Scenario, Europe, 2019 – 2029 (€M) (3 of 3) |

46 |

| Figure 4‑1: Implantable Ports by Company |

68 |

| Figure 4‑2: Port Needles by Company (1 of 2) |

69 |

| Figure 4‑3: Port Needles by Company (2 of 2) |

70 |

| Figure 4‑4: Central Venous Catheters by Company |

73 |

| Figure 4‑5: Peripherally Inserted Central Catheters by Company |

75 |

| Figure 4‑6: Peripheral Intravenous Catheters by Company |

77 |

| Figure 4‑7: Midlines by Company |

78 |

| Figure 4‑8: Extended Dwell Catheter by Company |

79 |

| Figure 4‑9: Dialysis Catheters by Company (1 of 2) |

82 |

| Figure 4‑10: Dialysis Catheters by Company (2 of 2) |

83 |

| Figure 4‑11: Ultrasound Vascular Access Devices and Accessories by Company |

86 |

| Figure 4‑12: Tip-Placement System and Accessories by Company |

88 |

| Figure 4‑13: Catheter Securement by Company (1 of 2) |

90 |

| Figure 4‑14: Catheter Securement by Company (2 of 2) |

91 |

| Figure 4‑15: Antibacterial Catheter Patch by Company |

92 |

| Figure 4‑16: Catheter Cap by Company |

93 |

| Figure 4‑17: Syringes and Needles by Company (1 of 2) |

95 |

| Figure 4‑18: Syringes and Needles by Company (2 of 2) |

96 |

| Figure 4‑19: Vein Visualization by Company |

97 |

| Figure 4‑20: Class 2 Device Recall PowerPort duo M.R.I. Implantable Port |

98 |

| Figure 4‑21: Class 2 Device Recall Smart Port CT |

98 |

| Figure 4‑22: Class 2 Device Recall PORTACATH II POWER P.A.C. Low Profile" System |

98 |

| Figure 4‑23: Class 2 Device Recall BARD Access Systems PowerPort ClearVUE Slim Implantable Port |

99 |

| Figure 4‑24: Class 2 Device Recall Vaccess CT PowerInjectable Implantable Port |

99 |

| Figure 4‑25: Class 2 Device Recall XPort isp M.R.I. Implantable Port |

99 |

| Figure 4‑26: Class 2 Device Recall Power Port Implantable Port |

99 |

| Figure 4‑27: Class 2 Device Recall PowerPort M.R.I. Implantable Port |

100 |

| Figure 4‑28: Class 2 Device Recall BardPort Titanium Implantable Port |

100 |

| Figure 4‑29: Class 2 Device Recall BardPort M.R.I. Hard Base Implantable Port |

100 |

| Figure 4‑30: Class 2 Device Recall Powerport Cleavue Slim Implantable Port |

100 |

| Figure 4‑31: Class 2 Device Recall Bard Access Systems PowerPort isp M.R.I. Implantable Port |

101 |

| Figure 4‑32: Class 2 Device Recall BioFlo Port with ENDEXO and PASV Technology |

101 |

| Figure 4‑33: Class 2 Device Recall Port Access Kit |

102 |

| Figure 4‑34: Class 2 Device Recall SafeStep Huber Needle Set |

102 |

| Figure 4‑35: Class 2 Device Recall PowerLoc MAX Power |

103 |

| Figure 4‑36: Class 2 Device Recall GRIPPER Needles |

103 |

| Figure 4‑37: Class 1 Device Recall Arrow Pressure Injectable Arrowgard Blue Plus ThreeLumen CVC Kit |

104 |

| Figure 4‑38: Class 2 Device Recall Arrow ThreeLumen CVC |

104 |

| Figure 4‑39: Class 2 Device Recall Arrow Teleflex |

104 |

| Figure 4‑40: Class 2 Device Recall Groshong CV Catheter |

105 |

| Figure 4‑41: Class 2 Device Recall Centurion |

105 |

| Figure 4‑42: Class 2 Device Recall Arrow AGB MultiLumen CVC Kit |

105 |

| Figure 4‑43: Class 2 Device Recall ARROWgard Blue Plus |

105 |

| Figure 4‑44: Class 2 Device Recall ARROWgard Blue Plus MultiLumen CVC Kit |

106 |

| Figure 4‑45: Class 2 Device Recall PICC KIT |

107 |

| Figure 4‑46: Class 2 Device Recall Various PICC Line, Central Line Packs |

107 |

| Figure 4‑47: Class 2 Device Recall Navilyst |

107 |

| Figure 4‑48: Class 2 Device Recall 5Fr PowerPICC Catheter SingleLumen with 70cm Guidewire |

107 |

| Figure 4‑49: Class 2 Device Recall BioFlo and Xcela |

108 |

| Figure 4‑50: Class 2 Device Recall Arrow PICC |

108 |

| Figure 4‑51: Class 2 Device Recall Arrow Pressure Injectable PICC |

109 |

| Figure 4‑52: Class 2 Device Recall Navilyst Medical BioFlo PICC with ENDEXO and PASV |

109 |

| Figure 4‑53: Class 2 Device Recall BD Nexiva Closed IV Catheter System |

110 |

| Figure 4‑54: Class 2 Device Recall BD Nexiva 20 GA 1.00 (1.1 x 25mm) Dual Port |

110 |

| Figure 4‑55: Class 2 Device Recall DELTAVEN Safety I.V. Catheter in Pur with closed system |

110 |

| Figure 4‑56: Class 2 Device Recall B. Braun Introcan Safety IV Catheters |

111 |

| Figure 4‑57: Class 2 Device Recall BD Nexiva Closed IV Catheter System Dual Port |

111 |

| Figure 4‑58: Class 2 Device Recall BD Nexiva Closed IV Catheter System |

111 |

| Figure 4‑59: Class 2 Device Recall Jelco(R) ViaValve(TM) Safety Intravenous (I.V.) Catheters |

111 |

| Figure 4‑60: Class 2 Device Recall ARROW Pressure Injectable Arrowgard Blue Advance Midline Kit |

112 |

| Figure 4‑61: Class 2 Device Recall PowerMidline Catheter |

112 |

| Figure 4‑62: Class 2 Device Recall BioFlo Midline |

112 |

| Figure 4‑63: Class 2 Device Recall PowerGlide ST Midline Catheter Maximal Barrier |

112 |

| Figure 4‑64: Class 2 Device Recall Arrowgard Blue Advance Midline |

113 |

| Figure 4‑65: Class 2 Device Recall Peripherally Inserted Midline Catheter Kit with Placement Wire |

113 |

| Figure 4‑66: Class 3 Device Recall POWERWAND XL 4Fr 10cm Maximum Barrier Kit |

114 |

| Figure 4‑67: Class 2 Device Recall Arrow Endurance Catheter System |

114 |

| Figure 4‑68: Class 1 Device Recall Mahurkar |

115 |

| Figure 4‑69: Class 1 Device Recall Hemodialysis Catheter |

115 |

| Figure 4‑70: Class 2 Device Recall Hemodialysis Implanted Catheter |

115 |

| Figure 4‑71: Class 2 Device Recall PowerTrialysis ShortTerm Alphacurve Dialysis Catheter |

115 |

| Figure 4‑72: Class 2 Device Recall EQUISTREAM LongTerm Hemodialysis Catheter |

116 |

| Figure 4‑73: Class 2 Device Recall GLIDEPATH LongTerm Hemodialysis Catheter |

116 |

| Figure 4‑74: Class 2 Device Recall 14F SLX Double Lumen Full Tray |

116 |

| Figure 4‑75: Class 2 Device Recall MAHURKAR" and Argyle" Acute Hemodialysis Catheters |

117 |

| Figure 4‑76: Class 2 Device Recall 14F SLX Double Lumen Full Tray |

117 |

| Figure 4‑77: Class 2 Device Recall Vivid |

118 |

| Figure 4‑78: Class 2 Device Recall ACUSON Juniper Diagnostic Ultrasound System |

118 |

| Figure 4‑79: Class 2 Device Recall Vscan Extend System, Imaging, Pulsed Echo, Ultrasonic |

119 |

| Figure 4‑80: Class 2 Device Recall AC/DC POWER SUPPLY for 7400 |

119 |

| Figure 4‑81: Class 2 Device Recall SiteRite 8 Ultrasound Systems |

119 |

| Figure 4‑82: Class 2 Device Recall VPS Rhythm ECG Accessory Pack |

120 |

| Figure 4‑83: Class 2 Device Recall Busse I.V. START KIT |

121 |

| Figure 4‑84: Class 2 Device Recall MERSILK and PERMAHAND, Braided Silk and Virgin Silk NonAbsorbable Suture |

121 |

| Figure 4‑85: Class 2 Device Recall Coated VICRYL (Polyglactin 910) Suture |

121 |

| Figure 4‑86: Class 2 Device Recall ETHIBOND EXCEL ETHIBOND Polyester Suture |

122 |

| Figure 4‑87: Class 2 Device Recall 3M Durapore Advanced Surgical Tape |

122 |

| Figure 4‑88: Class 2 Device Recall HEB InControl Insulin Syringe |

123 |

| Figure 4‑89: Class 1 Device Recall Monoject 0.9 Sodium Chloride Flush Syringe |

123 |

| Figure 4‑90: Class 1 Device Recall JELCO HYPODERMIC NEEDLEPRO FIXED NEEDLE INSULIN SYRINGE |

123 |

| Figure 4‑91: Class 2 Device Recall Covidien |

124 |

| Figure 4‑92: Class 2 Device Recall BD PrecisionGlide Needle 30G x 1/2 |

124 |

| Figure 4‑93: Class 2 Device Recall BD UltraFine Pen Needles 32G x 4mm |

124 |

| Figure 4‑94: Class 2 Device Recall Monoject Standard Hypodermic Needle |

124 |

| Figure 4‑95: Class 2 Device Recall BD SafetyGlideTM 3ml 25G x 1 |

125 |

| Figure 4‑96: Class 2 Device Recall Monoject Hypodermic Safety Needle |

125 |

| Figure 4‑97: Class 2 Device Recall GRIPPER Needles |

125 |

| Figure 4‑98: Class 2 Device Recall 3mL SafetyLok Syringe |

125 |

| Figure 4‑99: Class 2 Device Recall 3mL LuerLok Syringe |

126 |

| Figure 4‑100: Safety of Extending the Routine Flushing of Implanted Port Devices from 4 Weeks to 12 |

128 |

| Figure 4‑101: Interest of Virtual Reality to Reduce Patient Anxiety During the Placement of a Percutaneous Implantable Port Catheter (RV-CIP) |

128 |

| Figure 4‑102: A Retrospective, Observational, Multicenter Study to Evaluate the Safety and Performance of POLYSITE® and SEESITE® Implantable Ports |

129 |

| Figure 4‑103: Comparison Between Internal Jugular Vein Versus Axillary Vein for Implantable Ports |

129 |

| Figure 4‑104: Maintaining Patency in Implanted Port Catheters |

129 |

| Figure 4‑105: Ultrasound Guided Port-A-Cath Insertion in Cancer Patients |

130 |

| Figure 4‑106: Study on Indications of "Bard" PowerPort Isp Implantable Port (BPIP) |

130 |

| Figure 4‑107: Wire-in-needle vs. Traditional Technique for Ultrasound-Guided Central Venous Catheter Placement |

131 |

| Figure 4‑108: Central Venous Catheter-Related Complications in Patients Under Anticancer Treatment (KTcCHO) |

131 |

| Figure 4‑109: Infection Related to Short-Term Central Venous Catheters |

132 |

| Figure 4‑110: Point of Care Ultrasonography Versus Standard Blind Technique for Central Venous Catheter Insertion in Emergency Hospital |

132 |

| Figure 4‑111: Central Venous Catheter (CVC) Associated Deep Vein Thrombosis (DVT) in Cancer Patients |

132 |

| Figure 4‑112: Novel Strategy to Encourage Early Removal of Central Venous Catheters |

133 |

| Figure 4‑113: Novel Strategy to Encourage Early Removal of Central Venous Catheters |

133 |

| Figure 4‑114: Peripherally Inserted Versus Centrally Inserted Central Venous Catheters in the Neurosurgical Intensive Care Unit (PICINI) |

133 |

| Figure 4‑115: Comparing Peripherally Inserted Central Catheters to Long Peripheral Catheters in Pediatrics (ComPLET) |

134 |

| Figure 4‑116: Comparing Arrow PICC Catheters w/ Arrowga+rd Blue Advanced Protection Performance and Safety to Unprotected PICC's |

134 |

| Figure 4‑117: Prospective Observational Study of the Power PICC Family of Devices and Accessories |

135 |

| Figure 4‑118: Peripherally Inserted Central Catheter Insertion Site and Complication Rate in Neonates |

135 |

| Figure 4‑119: Major Complications Related to PICC and Midline Insertion (PICC/MIDLINE) |

135 |

| Figure 4‑120: Safety and Effectiveness of CATHTONG™ II PICC |

136 |

| Figure 4‑121: Ultrasound-Guided Peripheral Intravenous Catheter Insertion Technique (PIVC) |

137 |

| Figure 4‑122: Comparison of Two Peripheral Inserted Intravenous Catheters |

137 |

| Figure 4‑123: Impact of PIVC Length and Gauge on Catheter Indwell Time |

137 |

| Figure 4‑124: Impact of a Multimodal Intervention on Peripheral Venous Catheterization of Cancer Patients (MultiCat) |

138 |

| Figure 4‑125: Peripheral Intravenous Catheter Securement with Tissue Adhesive |

138 |

| Figure 4‑126: Peripherally Inserted Versus Centrally Inserted Central Venous Catheters in the Neurosurgical Intensive Care Unit (PICINI) |

138 |

| Figure 4‑127: Midline Catheter and Its Impact on Central Lines Removal in ICU (MIDREA) |

139 |

| Figure 4‑128: Patient Perspective Midline Catheter in the Emergency Department |

139 |

| Figure 4‑129: Midline Failures: A Comparison Between a Hydrophilic Biomaterial and Thermoplastic Polyurethane |

139 |

| Figure 4‑130: Safety and Efficacy of Midline and PICC (MidLine_PICC) |

140 |

| Figure 4‑131: Midlines and Thrombophlebitis |

140 |

| Figure 4‑132: Midline Catheter and Its Impact on Central Lines Removal in ICU (MIDREA) |

140 |

| Figure 4‑133: Upper Limb Thrombosis Associated With Midline Catheter |

141 |

| Figure 4‑134: The Clinical Efficacy of Midline Catheters |

141 |

| Figure 4‑135: Occurrence of Emerging Infections After Placement of a Peritoneal Dialysis CatHeter (SINEPHILE) |

142 |

| Figure 4‑136: Tunneled Dialysis Catheters Versus Non-Tunneled Dialysis Catheters as First-Line for Renal Replacement Therapy in the ICU (BACKDOOR) |

142 |

| Figure 4‑137: Straight Versus Coiled Peritoneal Dialysis Catheter for Peritoneal Dialysis Patients |

142 |

| Figure 4‑138: A Percutaneous Ultrasound Device with Needle Guide for Vascular Access |

143 |

| Figure 4‑139: Ultrasound Guided Peripheral Catheterization Increases First-Attempt Success Rate (SPECTRA) |

143 |

| Figure 4‑140: Ultrasound-Guided Peripheral IV vs. Standard Technique in Difficult Vascular Access Patients by ICU Nurses |

144 |

| Figure 4‑14144: Innovative Central Line Securement Device in the Pediatric Population |

145 |

| Figure 4‑142: Efficacy of an Infrared Visualization Technique for the Identification of the Peripheral Venous Access Site in Patients with Cystic Fibrosis Aged 12 Years and Older (MUCOVEINE) |

148 |

| Figure 4‑143: Infra Red Vein Visualization: Efficacy vs. Standard Technique |

148 |

| Figure 4‑144: Can Veinlite Reduce Complications of Peripheral Intravenous Catheter Placement in Children |

149 |

| Figure 5‑1: Currency Exchange Rate, 2022 |

151 |

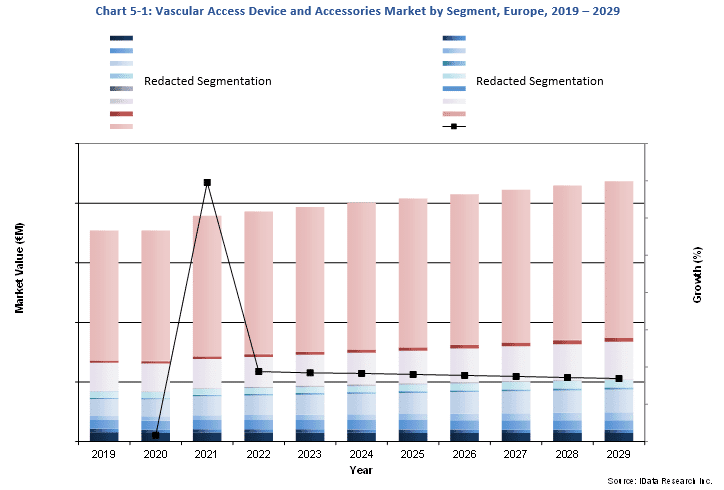

| Figure 5‑2: Vascular Access Devices and Accessories Market by Segment, Europe, 2019 – 2029 (€M) (1 of 3) |

154 |

| Figure 5‑3: Vascular Access Devices and Accessories Market by Segment, Europe, 2019 – 2029 (€M) (2 of 3) |

155 |

| Figure 5‑4: Vascular Access Devices and Accessories Market by Segment, Europe, 2019 – 2029 (€M) (3 of 3) |

156 |

| Figure 5‑5: Vascular Access Devices and Accessories Market by Segment, Europe, 2019 – 2029 (US$M) (1 of 3) |

157 |

| Figure 5‑6: Vascular Access Devices and Accessories Market by Segment, Europe, 2019 – 2029 (US$M) (2 of 3) |

158 |

| Figure 5‑7: Vascular Access Devices and Accessories Market by Segment, Europe, 2019 – 2029 (US$M) (3 of 3) |

159 |

| Figure 5‑8: Leading Competitors, Vascular Access Device and Accessories Market, Europe, 2022 (1 of 2) |

169 |

| Figure 5‑9: Leading Competitors, Vascular Access Device and Accessories Market, Europe, 2022 (2 of 2) |

170 |

| Figure 5‑10: SWOT Analysis, 3M |

189 |

| Figure 5‑11: SWOT Analysis, AccuVein |

190 |

| Figure 5‑12: SWOT Analysis, AngioDynamics |

191 |

| Figure 5‑13: SWOT Analysis, B. Braun |

192 |

| Figure 5‑14: SWOT Analysis, Becton Dickinson (1 of 2) |

193 |

| Figure 5‑15: SWOT Analysis, Becton Dickinson (2 of 2) |

194 |

| Figure 5‑16: SWOT Analysis, Cardinal Health |

195 |

| Figure 5‑17: SWOT Analysis, ICU Medical |

196 |

| Figure 5‑18: SWOT Analysis, Johnson & Johnson |

197 |

| Figure 5‑19: SWOT Analysis, Medcomp |

198 |

| Figure 5‑20: SWOT Analysis, Novo Nordisk |

199 |

| Figure 5‑21: SWOT Analysis, Teleflex Medical |

200 |

| Figure 7‑1: Vascular Access Procedures by Segment, Europe, 2019 – 2029 (1 of 2) |

213 |

| Figure 7‑2: Vascular Access Procedures by Segment, Europe, 2019 – 2029 (2 of 2) |

213 |

| Figure 7‑3: Vascular Access Procedures by Country, Europe, 2019 – 2029 (1 of 2) |

214 |

| Figure 7‑4: Vascular Access Procedures by Country, Europe, 2019 – 2029 (2 of 2) |

214 |

| Figure 7‑5: Implantable Port Insertion Procedures by Country, Europe, 2019 – 2029 |

217 |

| Figure 7‑6: Non-Power-Injectable Implantable Port Insertion Procedures by Country, Europe, 2019 – 2029 |

218 |

| Figure 7‑7: Power-Injectable Implantable Port Insertion Procedures by Country, Europe, 2019 – 2029 |

219 |

| Figure 7‑8: Port Needle Insertion Procedures by Country, Europe, 2019 – 2029 |

221 |

| Figure 7‑9: Conventional Port Needle Insertion Procedures by Country, Europe, 2019 – 2029 |

222 |

| Figure 7‑10: Safety Port Needle Insertion Procedures by Country, Europe, 2019 – 2029 |

223 |

| Figure 7‑11: CVC Insertion Procedures by Country, Europe, 2019 – 2029 |

225 |

| Figure 7‑12: Acute CVC Insertion Procedures by Country, Europe, 2019 – 2029 |

226 |

| Figure 7‑13: Chronic CVC Insertion Procedures by Country, Europe, 2019 – 2029 |

227 |

| Figure 7‑14: PICC Insertion Procedures by Country, Europe, 2019 – 2029 |

229 |

| Figure 7‑15: Non-Power-Injectable PICC Insertion Procedures by Country, Europe, 2019 – 2029 |

230 |

| Figure 7‑16: Power-Injectable PICC Insertion Procedures by Country, Europe, 2019 – 2029 |

231 |

| Figure 7‑17: PIVC Insertion Procedures by Country, Europe, 2019 – 2029 (1 of 2) |

233 |

| Figure 7‑18: PIVC Insertion Procedures by Country, Europe, 2019 – 2029 (2 of 2) |

233 |

| Figure 7‑19: Conventional PIVC Insertion Procedures by Country, Europe, 2019 – 2029 |

234 |

| Figure 7‑20: Safety PIVC Insertion Procedures by Country, Europe, 2019 – 2029 (1 of 2) |

235 |

| Figure 7‑21: Safety PIVC Insertion Procedures by Country, Europe, 2019 – 2029 (2 of 2) |

235 |

| Figure 7‑22: Midline Catheter Insertion Procedures by Country, Europe, 2019 – 2029 |

237 |

| Figure 7‑23: MST Midline Catheter Insertion Procedures by Country, Europe, 2019 – 2029 |

238 |

| Figure 7‑24: AST Midline Catheter Insertion Procedures by Country, Europe, 2019 – 2029 |

239 |

| Figure 7‑25: Dialysis Catheter Insertion Procedures by Country, Europe, 2019 – 2029 |

241 |

| Figure 7‑26: Long-Term Hemodialysis Catheter Insertion Procedures by Country, Europe, 2019 – 2029 |

242 |

| Figure 7‑27: Short-Term Hemodialysis Catheter Insertion Procedures by Country, Europe, 2019 – 2029 |

243 |

| Figure 7‑28: Peritoneal Dialysis Catheter Insertion Procedures by Country, Europe, 2019 – 2029 |

244 |

| Figure 8‑1: Implantable Port Market by Device Type, Europe, 2019 – 2029 (€M) |

247 |

| Figure 8‑2: Implantable Port Market by Device Type, Europe, 2019 – 2029 (US$M) |

247 |

| Figure 8‑3: Total Implantable Port Market, Europe, 2019 – 2029 |

250 |

| Figure 8‑4: Units Sold by Country, Implantable Port Market, Europe, 2019 – 2029 |

251 |

| Figure 8‑5: Average Selling Price by Country, Implantable Port Market, Europe, 2019 – 2029 (€) |

252 |

| Figure 8‑6: Average Selling Price by Country, Implantable Port Market, Europe, 2019 – 2029 (US$) |

253 |

| Figure 8‑7: Market Value by Country, Implantable Port Market, Europe, 2019 – 2029 (€M) |

254 |

| Figure 8‑8: Market Value by Country, Implantable Port Market, Europe, 2019 – 2029 (US$M) |

255 |

| Figure 8‑9: Non-Power-Injectable Implantable Port Market by Segment, Europe, 2019 – 2029 (€M) |

257 |

| Figure 8‑10: Non-Power-Injectable Implantable Port Market by Segment, Europe, 2019 – 2029 (US$M) |

258 |

| Figure 8‑11: Total Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

258 |

| Figure 8‑12: Units Sold by Country, Total Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

259 |

| Figure 8‑13: Average Selling Price by Country, Total Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€) |

260 |

| Figure 8‑14: Average Selling Price by Country, Total Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$) |

261 |

| Figure 8‑15: Market Value by Country, Total Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€M) |

262 |

| Figure 8‑16: Market Value by Country, Total Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$M) |

263 |

| Figure 8‑17: Single-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

264 |

| Figure 8‑18: Units Sold by Country, Single-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

265 |

| Figure 8‑19: Average Selling Price by Country, Single-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€) |

266 |

| Figure 8‑20: Average Selling Price by Country, Single-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$) |

267 |

| Figure 8‑21: Market Value by Country, Single-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€M) |

268 |

| Figure 8‑22: Market Value by Country, Single-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$M) |

269 |

| Figure 8‑23: Double-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

270 |

| Figure 8‑24: Units Sold by Country, Double-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

271 |

| Figure 8‑25: Average Selling Price by Country, Double-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€) |

272 |

| Figure 8‑26: Average Selling Price by Country, Double-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$) |

273 |

| Figure 8‑27: Market Value by Country, Double-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€M) |

274 |

| Figure 8‑28: Market Value by Country, Double-Lumen Non-Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$M) |

275 |

| Figure 8‑29: Power-Injectable Implantable Port Market by Segment, Europe, 2019 – 2029 (€M) |

277 |

| Figure 8‑30: Power-Injectable Implantable Port Market by Segment, Europe, 2019 – 2029 (US$M) |

277 |

| Figure 8‑31: Total Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

278 |

| Figure 8‑32: Units Sold by Country, Total Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

279 |

| Figure 8‑33: Average Selling Price by Country, Total Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€) |

280 |

| Figure 8‑34: Average Selling Price by Country, Total Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$) |

281 |

| Figure 8‑35: Market Value by Country, Total Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€M) |

282 |

| Figure 8‑36: Market Value by Country, Total Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$M) |

283 |

| Figure 8‑37: Single-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

284 |

| Figure 8‑38: Units Sold by Country, Single-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

285 |

| Figure 8‑39: Average Selling Price by Country, Single-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€) |

286 |

| Figure 8‑40: Average Selling Price by Country, Single-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$) |

287 |

| Figure 8‑41: Market Value by Country, Single-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€M) |

288 |

| Figure 8‑42: Market Value by Country, Single-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$M) |

289 |

| Figure 8‑43: Double-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

290 |

| Figure 8‑44: Units Sold by Country, Double-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 |

291 |

| Figure 8‑45: Average Selling Price by Country, Double-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€) |

292 |

| Figure 8‑46: Average Selling Price by Country, Double-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$) |

293 |

| Figure 8‑47: Market Value by Country, Double-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (€M) |

294 |

| Figure 8‑48: Market Value by Country, Double-Lumen Power-Injectable Implantable Port Market, Europe, 2019 – 2029 (US$M) |

295 |

| Figure 8‑49: Implantable Port Market by Device Property, Europe, 2019 – 2029 (€M) |

296 |

| Figure 8‑50: Implantable Port Market by Device Property, Europe, 2019 – 2029 (US$M) |

297 |

| Figure 8‑51: Antithrombogenic Implantable Port Market, Europe, 2019 – 2029 |

298 |

| Figure 8‑52: Units Sold by Country, Antithrombogenic Implantable Port Market, Europe, 2019 – 2029 |

299 |

| Figure 8‑53: Average Selling Price by Country, Antithrombogenic Implantable Port Market, Europe, 2019 – 2029 (€) |

300 |

| Figure 8‑54: Average Selling Price by Country, Antithrombogenic Implantable Port Market, Europe, 2019 – 2029 (US$) |

301 |

| Figure 8‑55: Market Value by Country, Antithrombogenic Implantable Port Market, Europe, 2019 – 2029 (€M) |

302 |

| Figure 8‑56: Market Value by Country, Antithrombogenic Implantable Port Market, Europe, 2019 – 2029 (US$M) |

303 |

| Figure 8‑57: Conventional Implantable Port Market, Europe, 2019 – 2029 |

304 |

| Figure 8‑58: Units Sold by Country, Conventional Implantable Port Market, Europe, 2019 – 2029 |

305 |

| Figure 8‑59: Average Selling Price by Country, Conventional Implantable Port Market, Europe, 2019 – 2029 (€) |

306 |

| Figure 8‑60: Average Selling Price by Country, Conventional Implantable Port Market, Europe, 2019 – 2029 (US$) |

307 |

| Figure 8‑61: Market Value by Country, Conventional Implantable Port Market, Europe, 2019 – 2029 (€M) |

308 |

| Figure 8‑62: Market Value by Country, Conventional Implantable Port Market, Europe, 2019 – 2029 (US$M) |

309 |

| Figure 8‑63: Leading Competitors by Country, Implantable Port Market, Europe, 2022 |

316 |

| Figure 9‑1: Port Needle Market by Segment, Europe, 2019 – 2029 (€M) |

320 |

| Figure 9‑2: Port Needle Market by Segment, Europe, 2019 – 2029 (US$M) |

321 |

| Figure 9‑3: Port Needle Market, Europe, 2019 – 2029 |

324 |

| Figure 9‑4: Units Sold by Country, Port Needle Market, Europe, 2019 – 2029 |

325 |

| Figure 9‑5: Average Selling Price by Country, Port Needle Market, Europe, 2019 – 2029 (€) |

326 |

| Figure 9‑6: Average Selling Price by Country, Port Needle Market, Europe, 2019 – 2029 (US$) |

327 |

| Figure 9‑7: Market Value by Country, Port Needle Market, Europe, 2019 – 2029 (€M) |

328 |

| Figure 9‑8: Market Value by Country, Port Needle Market, Europe, 2019 – 2029 (US$M) |

329 |

| Figure 9‑9: Conventional Port Needle Market, Europe, 2019 – 2029 |

331 |

| Figure 9‑10: Units Sold by Country, Conventional Port Needle Market, Europe, 2019 – 2029 |

332 |

| Figure 9‑11: Average Selling Price by Country, Conventional Port Needle Market, Europe, 2019 – 2029 (€) |

333 |

| Figure 9‑12: Average Selling Price by Country, Conventional Port Needle Market, Europe, 2019 – 2029 (US$) |

334 |

| Figure 9‑13: Market Value by Country, Conventional Port Needle Market, Europe, 2019 – 2029 (€M) |

335 |

| Figure 9‑14: Market Value by Country, Conventional Port Needle Market, Europe, 2019 – 2029 (US$M) |

336 |

| Figure 9‑15: Safety Port Needle Market by Segment, Europe, 2019 – 2029 (€M) |

338 |

| Figure 9‑16: Safety Port Needle Market by Segment, Europe, 2019 – 2029 (US$M) |

338 |

| Figure 9‑17: Total Safety Port Needle Market, Europe, 2019 – 2029 |

339 |

| Figure 9‑18: Units Sold by Country, Total Safety Port Needle Market, Europe, 2019 – 2029 |

340 |

| Figure 9‑19: Average Selling Price by Country, Total Safety Port Needle Market, Europe, 2019 – 2029 (€) |

341 |

| Figure 9‑20: Average Selling Price by Country, Total Safety Port Needle Market, Europe, 2019 – 2029 (US$) |

342 |

| Figure 9‑21: Market Value by Country, Total Safety Port Needle Market, Europe, 2019 – 2029 (€M) |

343 |

| Figure 9‑22: Market Value by Country, Total Safety Port Needle Market, Europe, 2019 – 2029 (US$M) |

344 |

| Figure 9‑23: Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 |

346 |

| Figure 9‑24: Units Sold by Country, Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 |

347 |

| Figure 9‑25: Average Selling Price by Country, Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (€) |

348 |

| Figure 9‑26: Average Selling Price by Country, Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (US$) |

349 |

| Figure 9‑27: Market Value by Country, Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (€M) |

350 |

| Figure 9‑28: Market Value by Country, Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (US$M) |

351 |

| Figure 9‑29: Non-Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 |

352 |

| Figure 9‑30: Units Sold by Country, Non-Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 |

353 |

| Figure 9‑31: Average Selling Price by Country, Non-Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (€) |

354 |

| Figure 9‑32: Average Selling Price by Country, Non-Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (US$) |

355 |

| Figure 9‑33: Market Value by Country, Non-Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (€M) |

356 |

| Figure 9‑34: Market Value by Country, Non-Power-Injectable Safety Port Needle Market, Europe, 2019 – 2029 (US$M) |

357 |

| Figure 9‑35: Leading Competitors by Country, Port Needle Market, Europe, 2022 |

363 |

| Figure 10‑1: Central Venous Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

367 |

| Figure 10‑2: Central Venous Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

367 |

| Figure 10‑3: Total Central Venous Catheter Market, Europe, 2019 – 2029 |

370 |

| Figure 10‑4: Units Sold by Country, Central Venous Catheter Market, Europe, 2019 – 2029 |

371 |

| Figure 10‑5: Average Selling Price by Country, Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

372 |

| Figure 10‑6: Average Selling Price by Country, Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

373 |

| Figure 10‑7: Market Value by Country, Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

374 |

| Figure 10‑8: Market Value by Country, Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

375 |

| Figure 10‑9: Total Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

376 |

| Figure 10‑10: Units Sold by Country, Total Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

377 |

| Figure 10‑11: Average Selling Price by Country, Total Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

378 |

| Figure 10‑12: Average Selling Price by Country, Total Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

379 |

| Figure 10‑13: Market Value by Country, Total Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

380 |

| Figure 10‑14: Market Value by Country, Total Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

381 |

| Figure 10‑15: Acute Central Venous Catheter Market by Device Type, Europe, 2019 – 2029 (€M) |

383 |

| Figure 10‑16: Acute Central Venous Catheter Market by Device Type, Europe, 2019 – 2029 (US$M) |

383 |

| Figure 10‑17: Conventional Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

385 |

| Figure 10‑18: Units Sold by Country, Conventional Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

386 |

| Figure 10‑19: Average Selling Price by Country, Conventional Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

387 |

| Figure 10‑20: Average Selling Price by Country, Conventional Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

388 |

| Figure 10‑21: Market Value by Country, Conventional Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

389 |

| Figure 10‑22: Market Value by Country, Conventional Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

390 |

| Figure 10‑23: Antimicrobial Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

392 |

| Figure 10‑24: Units Sold by Country, Antimicrobial Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

393 |

| Figure 10‑25: Average Selling Price by Country, Antimicrobial Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

394 |

| Figure 10‑26: Average Selling Price by Country, Antimicrobial Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

395 |

| Figure 10‑27: Market Value by Country, Antimicrobial Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

396 |

| Figure 10‑28: Market Value by Country, Antimicrobial Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

397 |

| Figure 10‑29: Acute Central Venous Catheter Market by Injectability, Europe, 2019 – 2029 (€M) |

399 |

| Figure 10‑30: Acute Central Venous Catheter Market by Injectability, Europe, 2019 – 2029 (US$M) |

399 |

| Figure 10‑31: Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

400 |

| Figure 10‑32: Units Sold by Country, Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

401 |

| Figure 10‑33: Average Selling Price by Country, Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

402 |

| Figure 10‑34: Average Selling Price by Country, Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

403 |

| Figure 10‑35: Market Value by Country, Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

404 |

| Figure 10‑36: Market Value by Country, Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

405 |

| Figure 10‑37: Non-Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

406 |

| Figure 10‑38: Units Sold by Country, Non-Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 |

407 |

| Figure 10‑39: Average Selling Price by Country, Non-Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

408 |

| Figure 10‑40: Average Selling Price by Country, Non-Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

409 |

| Figure 10‑41: Market Value by Country, Non-Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

410 |

| Figure 10‑42: Market Value by Country, Non-Power-Injectable Acute Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

411 |

| Figure 10‑43: Total Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

413 |

| Figure 10‑44: Units Sold by Country, Total Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

414 |

| Figure 10‑45: Average Selling Price by Country, Total Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

415 |

| Figure 10‑46: Average Selling Price by Country, Total Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

416 |

| Figure 10‑47: Market Value by Country, Total Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

417 |

| Figure 10‑48: Market Value by Country, Total Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

418 |

| Figure 10‑49: Chronic Central Venous Catheter Market by Injectability, Europe, 2019 – 2029 (€M) |

419 |

| Figure 10‑50: Chronic Central Venous Catheter Market by Injectability, Europe, 2019 – 2029 (US$M) |

420 |

| Figure 10‑51: Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

421 |

| Figure 10‑52: Units Sold by Country, Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

422 |

| Figure 10‑53: Average Selling Price by Country, Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

423 |

| Figure 10‑54: Average Selling Price by Country, Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

424 |

| Figure 10‑55: Market Value by Country, Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

425 |

| Figure 10‑56: Market Value by Country, Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

426 |

| Figure 10‑57: Non-Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

427 |

| Figure 10‑58: Units Sold by Country, Non-Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

428 |

| Figure 10‑59: Average Selling Price by Country, Non-Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

429 |

| Figure 10‑60: Average Selling Price by Country, Non-Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

430 |

| Figure 10‑61: Market Value by Country, Non-Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

431 |

| Figure 10‑62: Market Value by Country, Non-Power-Injectable Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

432 |

| Figure 10‑63: Chronic Central Venous Catheter Market by Device Type, Europe, 2019 – 2029 (€M) |

433 |

| Figure 10‑64: Chronic Central Venous Catheter Market by Device Type, Europe, 2019 – 2029 (US$M) |

434 |

| Figure 10‑65: Advanced Material Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

435 |

| Figure 10‑66: Units Sold by Country, Advanced Material Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

436 |

| Figure 10‑67: Average Selling Price by Country, Advanced Material Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

437 |

| Figure 10‑68: Average Selling Price by Country, Advanced Material Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

438 |

| Figure 10‑69: Market Value by Country, Advanced Material Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

439 |

| Figure 10‑70: Market Value by Country, Advanced Material Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

440 |

| Figure 10‑71: Conventional Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

441 |

| Figure 10‑72: Units Sold by Country, Conventional Chronic Central Venous Catheter Market, Europe, 2019 – 2029 |

442 |

| Figure 10‑73: Average Selling Price by Country, Conventional Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€) |

443 |

| Figure 10‑74: Average Selling Price by Country, Conventional Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$) |

444 |

| Figure 10‑75: Market Value by Country, Conventional Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (€M) |

445 |

| Figure 10‑76: Market Value by Country, Conventional Chronic Central Venous Catheter Market, Europe, 2019 – 2029 (US$M) |

446 |

| Figure 10‑77: Leading Competitors, Central Venous Catheter Market, Europe, 2022 |

453 |

| Figure 10‑78: Leading Competitors by Country, Central Venous Catheter Market, Europe, 2022 |

454 |

| Figure 11‑1: Peripherally Inserted Central Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

458 |

| Figure 11‑2: Peripherally Inserted Central Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

459 |

| Figure 11‑3: Total Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

463 |

| Figure 11‑4: Units Sold by Country, Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

464 |

| Figure 11‑5: Average Selling Price by Country, Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

465 |

| Figure 11‑6: Average Selling Price by Country, Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

466 |

| Figure 11‑7: Market Value by Country, Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

467 |

| Figure 11‑8: Market Value by Country, Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

468 |

| Figure 11‑9: Single-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

470 |

| Figure 11‑10: Units Sold by Country, Single-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

471 |

| Figure 11‑11: Average Selling Price by Country, Single-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

472 |

| Figure 11‑12: Average Selling Price by Country, Single-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

473 |

| Figure 11‑13: Market Value by Country, Single-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

474 |

| Figure 11‑14: Market Value by Country, Single-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

475 |

| Figure 11‑15: Double-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

476 |

| Figure 11‑16: Units Sold by Country, Double-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

477 |

| Figure 11‑17: Average Selling Price by Country, Double-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

478 |

| Figure 11‑18: Average Selling Price by Country, Double-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

479 |

| Figure 11‑19: Market Value by Country, Double-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

480 |

| Figure 11‑20: Market Value by Country, Double-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

481 |

| Figure 11‑21: Triple-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

482 |

| Figure 11‑22: Units Sold by Country, Triple-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

483 |

| Figure 11‑23: Average Selling Price by Country, Triple-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

484 |

| Figure 11‑24: Average Selling Price by Country, Triple-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

485 |

| Figure 11‑25: Market Value by Country, Triple-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

486 |

| Figure 11‑26: Market Value by Country, Triple-Lumen Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

487 |

| Figure 11‑27: Peripherally Inserted Central Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

488 |

| Figure 11‑28: Peripherally Inserted Central Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

489 |

| Figure 11‑29: Non-Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

491 |

| Figure 11‑30: Units Sold by Country, Non-Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

492 |

| Figure 11‑31: Average Selling Price by Country, Non-Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

493 |

| Figure 11‑32: Average Selling Price by Country, Non-Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

494 |

| Figure 11‑33: Market Value by Country, Non-Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

495 |

| Figure 11‑34: Market Value by Country, Non-Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

496 |

| Figure 11‑35: Power-Injectable Peripherally Inserted Central Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

498 |

| Figure 11‑36: Power-Injectable Peripherally Inserted Central Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

499 |

| Figure 11‑37: Total Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

499 |

| Figure 11‑38: Units Sold by Country, Total Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

500 |

| Figure 11‑39: Average Selling Price by Country, Total Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

501 |

| Figure 11‑40: Average Selling Price by Country, Total Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

502 |

| Figure 11‑41: Market Value by Country, Total Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

503 |

| Figure 11‑42: Market Value by Country, Total Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

504 |

| Figure 11‑43: Advanced Material Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

505 |

| Figure 11‑44: Units Sold by Country, Advanced Material Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

506 |

| Figure 11‑45: Average Selling Price by Country, Advanced Material Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

507 |

| Figure 11‑46: Average Selling Price by Country, Advanced Material Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

508 |

| Figure 11‑47: Market Value by Country, Advanced Material Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

509 |

| Figure 11‑48: Market Value by Country, Advanced Material Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

510 |

| Figure 11‑49: Conventional Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

511 |

| Figure 11‑50: Units Sold by Country, Conventional Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

512 |

| Figure 11‑51: Average Selling Price by Country, Conventional Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

513 |

| Figure 11‑52: Average Selling Price by Country, Conventional Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

514 |

| Figure 11‑53: Market Value by Country, Conventional Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

515 |

| Figure 11‑54: Market Value by Country, Conventional Power-Injectable Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

516 |

| Figure 11‑55: Peripherally Inserted Central Catheter Market by Kit Type, Europe, 2019 – 2029 (€M) |

517 |

| Figure 11‑56: Peripherally Inserted Central Catheter Market by Kit Type, Europe, 2019 – 2029 (US$M) |

518 |

| Figure 11‑57: Tip-Placement Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

519 |

| Figure 11‑58: Units Sold by Country, Tip-Placement Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

520 |

| Figure 11‑59: Average Selling Price by Country, Tip-Placement Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

521 |

| Figure 11‑60: Average Selling Price by Country, Tip-Placement Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

522 |

| Figure 11‑61: Market Value by Country, Tip-Placement Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

523 |

| Figure 11‑62: Market Value by Country, Tip-Placement Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

524 |

| Figure 11‑63: Conventional Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

525 |

| Figure 11‑64: Units Sold by Country, Conventional Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 |

526 |

| Figure 11‑65: Average Selling Price by Country, Conventional Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€) |

527 |

| Figure 11‑66: Average Selling Price by Country, Conventional Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$) |

528 |

| Figure 11‑67: Market Value by Country, Conventional Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (€M) |

529 |

| Figure 11‑68: Market Value by Country, Conventional Kit Peripherally Inserted Central Catheter Market, Europe, 2019 – 2029 (US$M) |

530 |

| Figure 11‑69: Leading Competitors by Country, Peripherally Inserted Central Catheter Market, Europe, 2022 |

536 |

| Figure 12‑1: Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

541 |

| Figure 12‑2: Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

542 |

| Figure 12‑3: Total Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

545 |

| Figure 12‑4: Units Sold by Country, Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

546 |

| Figure 12‑5: Units Sold by Country, Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

546 |

| Figure 12‑6: Average Selling Price by Country, Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

547 |

| Figure 12‑7: Average Selling Price by Country, Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

548 |

| Figure 12‑8: Market Value by Country, Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

549 |

| Figure 12‑9: Market Value by Country, Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

550 |

| Figure 12‑10: Conventional Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

552 |

| Figure 12‑11: Units Sold by Country, Conventional Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

553 |

| Figure 12‑12: Units Sold by Country, Conventional Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

553 |

| Figure 12‑13: Average Selling Price by Country, Conventional Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

554 |

| Figure 12‑14: Average Selling Price by Country, Conventional Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

555 |

| Figure 12‑15: Market Value by Country, Conventional Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

556 |

| Figure 12‑16: Market Value by Country, Conventional Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

557 |

| Figure 12‑17: Safety Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

559 |

| Figure 12‑18: Safety Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

560 |

| Figure 12‑19: Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

561 |

| Figure 12‑20: Units Sold by Country, Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

562 |

| Figure 12‑21: Units Sold by Country, Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

562 |

| Figure 12‑22: Average Selling Price by Country, Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

563 |

| Figure 12‑23: Average Selling Price by Country, Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

564 |

| Figure 12‑24: Market Value by Country, Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

565 |

| Figure 12‑25: Market Value by Country, Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

566 |

| Figure 12‑26: Blood Control Safety Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

567 |

| Figure 12‑27: Blood Control Safety Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

568 |

| Figure 12‑28: Total Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

568 |

| Figure 12‑29: Units Sold by Country, Total Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

569 |

| Figure 12‑30: Units Sold by Country, Total Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

569 |

| Figure 12‑31: Average Selling Price by Country, Total Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

570 |

| Figure 12‑32: Average Selling Price by Country, Total Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

571 |

| Figure 12‑33: Market Value by Country, Total Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

572 |

| Figure 12‑34: Market Value by Country, Total Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

573 |

| Figure 12‑35: Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

574 |

| Figure 12‑36: Units Sold by Country, Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

575 |

| Figure 12‑37: Average Selling Price by Country, Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

576 |

| Figure 12‑38: Average Selling Price by Country, Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

577 |

| Figure 12‑39: Market Value by Country, Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

578 |

| Figure 12‑40: Market Value by Country, Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

579 |

| Figure 12‑41: Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

580 |

| Figure 12‑42: Units Sold by Country, Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

581 |

| Figure 12‑43: Units Sold by Country, Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

581 |

| Figure 12‑44: Average Selling Price by Country, Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

582 |

| Figure 12‑45: Average Selling Price by Country, Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

583 |

| Figure 12‑46: Market Value by Country, Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

584 |

| Figure 12‑47: Market Value by Country, Non-Integrated Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

585 |

| Figure 12‑48: Non-Blood Control Safety Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

587 |

| Figure 12‑49: Non-Blood Control Safety Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

588 |

| Figure 12‑50: Total Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

588 |

| Figure 12‑51: Units Sold by Country, Total Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

589 |

| Figure 12‑52: Units Sold by Country, Total Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

589 |

| Figure 12‑53: Average Selling Price by Country, Total Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

590 |

| Figure 12‑54: Average Selling Price by Country, Total Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

591 |

| Figure 12‑55: Market Value by Country, Total Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

592 |

| Figure 12‑56: Market Value by Country, Total Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

593 |

| Figure 12‑57: Active Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

594 |

| Figure 12‑58: Units Sold by Country, Active Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

595 |

| Figure 12‑59: Units Sold by Country, Active Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

595 |

| Figure 12‑60: Average Selling Price by Country, Active Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

596 |

| Figure 12‑61: Average Selling Price by Country, Active Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

597 |

| Figure 12‑62: Market Value by Country, Active Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

598 |

| Figure 12‑63: Market Value by Country, Active Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

599 |

| Figure 12‑64: Passive Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

600 |

| Figure 12‑65: Units Sold by Country, Passive Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

601 |

| Figure 12‑66: Units Sold by Country, Passive Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

601 |

| Figure 12‑67: Average Selling Price by Country, Passive Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

602 |

| Figure 12‑68: Average Selling Price by Country, Passive Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

603 |

| Figure 12‑69: Market Value by Country, Passive Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

604 |

| Figure 12‑70: Market Value by Country, Passive Non-Blood Control Safety Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

605 |

| Figure 12‑71: Peripheral Intravenous Catheter Market by Setting, Europe, 2019 – 2029 (€M) |

607 |

| Figure 12‑72: Peripheral Intravenous Catheter Market by Setting, Europe, 2019 – 2029 (US$M) |

607 |

| Figure 12‑73: Acute Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

608 |

| Figure 12‑74: Units Sold by Country, Acute Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

609 |

| Figure 12‑75: Units Sold by Country, Acute Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

609 |

| Figure 12‑76: Average Selling Price by Country, Acute Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

610 |

| Figure 12‑77: Average Selling Price by Country, Acute Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

611 |

| Figure 12‑78: Market Value by Country, Acute Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

612 |

| Figure 12‑79: Market Value by Country, Acute Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

613 |

| Figure 12‑80: Alternate Care Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

615 |

| Figure 12‑81: Alternate Care Peripheral Intravenous Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

616 |

| Figure 12‑82: Total Alternate Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

616 |

| Figure 12‑83: Units Sold by Country, Total Alternate Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

617 |

| Figure 12‑84: Units Sold by Country, Total Alternate Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

617 |

| Figure 12‑85: Average Selling Price by Country, Total Alternate Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

618 |

| Figure 12‑86: Average Selling Price by Country, Total Alternate Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

619 |

| Figure 12‑87: Market Value by Country, Total Alternate Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

620 |

| Figure 12‑88: Market Value by Country, Total Alternate Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

621 |

| Figure 12‑89: Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

622 |

| Figure 12‑90: Units Sold by Country, Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

623 |

| Figure 12‑91: Average Selling Price by Country, Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

624 |

| Figure 12‑92: Average Selling Price by Country, Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

625 |

| Figure 12‑93: Market Value by Country, Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

626 |

| Figure 12‑94: Market Value by Country, Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

627 |

| Figure 12‑95: Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 |

628 |

| Figure 12‑96: Units Sold by Country, Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (1 of 2) |

629 |

| Figure 12‑97: Units Sold by Country, Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (2 of 2) |

629 |

| Figure 12‑98: Average Selling Price by Country, Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€) |

630 |

| Figure 12‑99: Average Selling Price by Country, Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$) |

631 |

| Figure 12‑100: Market Value by Country, Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (€M) |

632 |

| Figure 12‑101: Market Value by Country, Outpatient and Nursing Home Care Peripheral Intravenous Catheter Market, Europe, 2019 – 2029 (US$M) |

633 |

| Figure 12‑102: Leading Competitors by Country, Peripheral Intravenous Catheter Market, Europe, 2022 |

639 |

| Figure 13‑1: Midline Market by Segment, Europe, 2019 – 2029 (€M) |

643 |

| Figure 13‑2: Midline Market by Segment, Europe, 2019 – 2029 (US$M) |

643 |

| Figure 13‑3: Total Midline Market, Europe, 2019 – 2029 |

646 |

| Figure 13‑4: Units Sold by Country, Midline Market, Europe, 2019 – 2029 |

647 |

| Figure 13‑5: Average Selling Price by Country, Midline Market, Europe, 2019 – 2029 (€) |

648 |

| Figure 13‑6: Average Selling Price by Country, Midline Market, Europe, 2019 – 2029 (US$) |

649 |

| Figure 13‑7: Market Value by Country, Midline Market, Europe, 2019 – 2029 (€M) |

650 |

| Figure 13‑8: Market Value by Country, Midline Market, Europe, 2019 – 2029 (US$M) |

651 |

| Figure 13‑9: MST Midline Market by Segment, Europe, 2019 – 2029 (€M) |

653 |

| Figure 13‑10: MST Midline Market by Segment, Europe, 2019 – 2029 (US$M) |

653 |

| Figure 13‑11: Total MST Midline Market, Europe, 2019 – 2029 |

654 |

| Figure 13‑12: Units Sold by Country, Total MST Midline Market, Europe, 2019 – 2029 |

655 |

| Figure 13‑13: Average Selling Price by Country, Total MST Midline Market, Europe, 2019 – 2029 (€) |

656 |

| Figure 13‑14: Average Selling Price by Country, Total MST Midline Market, Europe, 2019 – 2029 (US$) |

657 |

| Figure 13‑15: Market Value by Country, Total MST Midline Market, Europe, 2019 – 2029 (€M) |

658 |

| Figure 13‑16: Market Value by Country, Total MST Midline Market, Europe, 2019 – 2029 (US$M) |

659 |

| Figure 13‑17: Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 |

660 |

| Figure 13‑18: Units Sold by Country, Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 |

661 |

| Figure 13‑19: Average Selling Price by Country, Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (€) |

662 |

| Figure 13‑20: Average Selling Price by Country, Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (US$) |

663 |

| Figure 13‑21: Market Value by Country, Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (€M) |

664 |

| Figure 13‑22: Market Value by Country, Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (US$M) |

665 |

| Figure 13‑23: Non-Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 |

666 |

| Figure 13‑24: Units Sold by Country, Non-Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 |

667 |

| Figure 13‑25: Average Selling Price by Country, Non-Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (€) |

668 |

| Figure 13‑26: Average Selling Price by Country, Non-Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (US$) |

669 |

| Figure 13‑27: Market Value by Country, Non-Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (€M) |

670 |

| Figure 13‑28: Market Value by Country, Non-Power-Injectable MST Midline Catheter Market, Europe, 2019 – 2029 (US$M) |

671 |

| Figure 13‑29: AST Midline Market, Europe, 2019 – 2029 |

673 |

| Figure 13‑30: Units Sold by Country, AST Midline Market, Europe, 2019 – 2029 |

674 |

| Figure 13‑31: Average Selling Price by Country, AST Midline Market, Europe, 2019 – 2029 (€) |

675 |

| Figure 13‑32: Average Selling Price by Country, AST Midline Market, Europe, 2019 – 2029 (US$) |

676 |

| Figure 13‑33: Market Value by Country, AST Midline Market, Europe, 2019 – 2029 (€M) |

677 |

| Figure 13‑34: Market Value by Country, AST Midline Market, Europe, 2019 – 2029 (US$M) |

678 |

| Figure 13‑35: Leading Competitors, Midline Market, Europe, 2022 |

683 |

| Figure 13‑36: Leading Competitors by Country, Midline Market, Europe, 2022 |

684 |

| Figure 14‑1: Extended Dwell Catheter Market, Europe, 2019 – 2029 |

688 |

| Figure 14‑2: Units Sold by Country, Extended Dwell Catheter Market, Europe, 2019 – 2029 |

690 |

| Figure 14‑3: Average Selling Price by Country, Extended Dwell Catheter Market, Europe, 2019 – 2029 (€) |

691 |

| Figure 14‑4: Average Selling Price by Country, Extended Dwell Catheter Market, Europe, 2019 – 2029 (US$) |

692 |

| Figure 14‑5: Market Value by Country, Extended Dwell Catheter Market, Europe, 2019 – 2029 (€M) |

693 |

| Figure 14‑6: Market Value by Country, Extended Dwell Catheter Market, Europe, 2019 – 2029 (US$M) |

694 |

| Figure 14‑7: Leading Competitors, Extended Dwell Catheter Market, Europe, 2022 |

698 |

| Figure 15‑1: Dialysis Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

702 |

| Figure 15‑2: Dialysis Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

702 |

| Figure 15‑3: Hemodialysis Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

704 |

| Figure 15‑4: Hemodialysis Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

705 |

| Figure 15‑5: Total Hemodialysis Catheter Market, Europe, 2019 – 2029 |

705 |

| Figure 15‑6: Units Sold by Country, Hemodialysis Catheter Market, Europe, 2019 – 2029 |

706 |

| Figure 15‑7: Average Selling Price by Country, Hemodialysis Catheter Market, Europe, 2019 – 2029 (€) |

707 |

| Figure 15‑8: Average Selling Price by Country, Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$) |

708 |

| Figure 15‑9: Market Value by Country, Hemodialysis Catheter Market, Europe, 2019 – 2029 (€M) |

709 |

| Figure 15‑10: Market Value by Country, Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$M) |

710 |

| Figure 15‑11: Long-Term Hemodialysis Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

712 |

| Figure 15‑12: Long-Term Hemodialysis Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

712 |

| Figure 15‑13: Total Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

713 |

| Figure 15‑14: Units Sold by Country, Total Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

714 |

| Figure 15‑15: Average Selling Price by Country, Total Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€) |

715 |

| Figure 15‑16: Average Selling Price by Country, Total Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$) |

716 |

| Figure 15‑17: Market Value by Country, Total Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€M) |

717 |

| Figure 15‑18: Market Value by Country, Total Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$M) |

718 |

| Figure 15‑19: Conventional Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

719 |

| Figure 15‑20: Units Sold by Country, Conventional Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

720 |

| Figure 15‑21: Average Selling Price by Country, Conventional Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€) |

721 |

| Figure 15‑22: Average Selling Price by Country, Conventional Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$) |

722 |

| Figure 15‑23: Market Value by Country, Conventional Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€M) |

723 |

| Figure 15‑24: Market Value by Country, Conventional Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$M) |

724 |

| Figure 15‑25: Antimicrobial Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

726 |

| Figure 15‑26: Units Sold by Country, Antimicrobial Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

727 |

| Figure 15‑27: Average Selling Price by Country, Antimicrobial Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€) |

728 |

| Figure 15‑28: Average Selling Price by Country, Antimicrobial Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$) |

729 |

| Figure 15‑29: Market Value by Country, Antimicrobial Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€M) |

730 |

| Figure 15‑30: Market Value by Country, Antimicrobial Long-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$M) |

731 |

| Figure 15‑31: Short-Term Hemodialysis Catheter Market by Segment, Europe, 2019 – 2029 (€M) |

733 |

| Figure 15‑32: Short-Term Hemodialysis Catheter Market by Segment, Europe, 2019 – 2029 (US$M) |

733 |

| Figure 15‑33: Total Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

734 |

| Figure 15‑34: Units Sold by Country, Total Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

735 |

| Figure 15‑35: Average Selling Price by Country, Total Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€) |

736 |

| Figure 15‑36: Average Selling Price by Country, Total Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$) |

737 |

| Figure 15‑37: Market Value by Country, Total Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€M) |

738 |

| Figure 15‑38: Market Value by Country, Total Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$M) |

739 |

| Figure 15‑39: Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

740 |

| Figure 15‑40: Units Sold by Country, Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

741 |

| Figure 15‑41: Average Selling Price by Country, Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€) |

742 |

| Figure 15‑42: Average Selling Price by Country, Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$) |

743 |

| Figure 15‑43: Market Value by Country, Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (€M) |

744 |

| Figure 15‑44: Market Value by Country, Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 (US$M) |

745 |

| Figure 15‑45: Non-Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

746 |

| Figure 15‑46: Units Sold by Country, Non-Power-Injectable Short-Term Hemodialysis Catheter Market, Europe, 2019 – 2029 |

747 |