Product Description

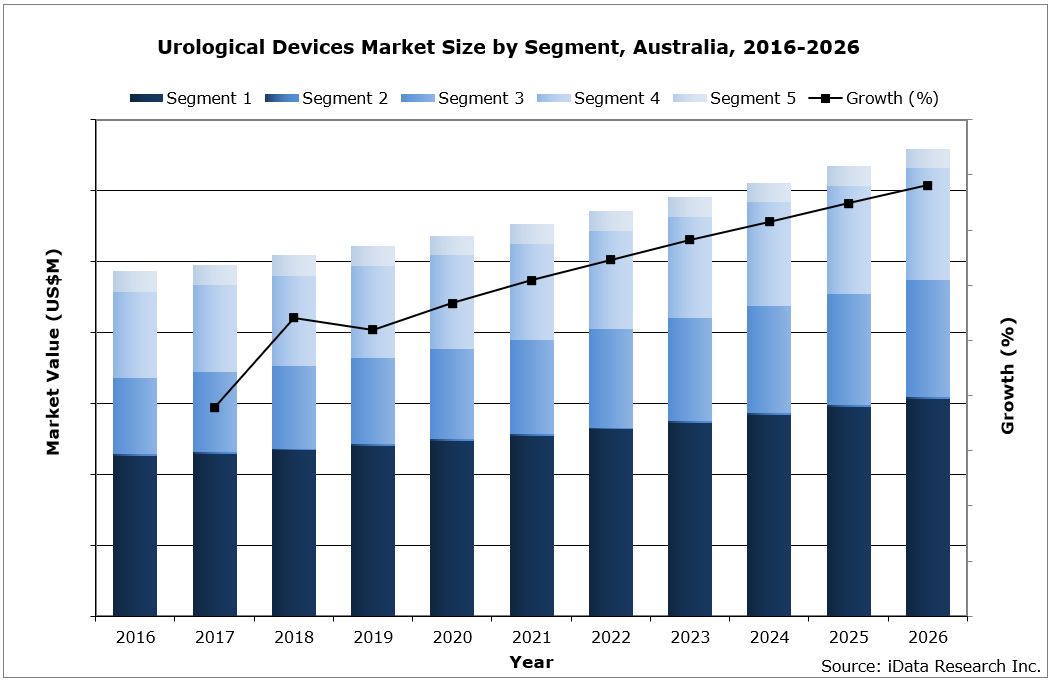

In 2020, the Australian urology market size was valued at nearly $72 million, with over 167,000 yearly urological procedures performed every year. The market size is expected to increase at a compound annual growth rate (CAGR) of 3% to reach nearly $89 million in 2026.

Throughout this medical market research, we analyzed 31 urology companies across Australia and used our comprehensive methodology to understand the market sizes, unit sales, company market shares, and to create accurate forecasts.

While this MedSuite report contains all of the Australian Urological Device market data and analysis, each of the market segments is also available as stand-alone MedCore reports. This allows you to get access to only the market research that you need.

DATA TYPES INCLUDED

- Unit Sales, Average Selling Prices, Market Value & Growth Trends

- Urology Procedure Volumes

- Market Forecasts Until 2026, and Historical Data to 2016

- Competitive Analysis with Market Shares for Each Segment

- Market Drivers & Limiters for Each Urological Device market

- Recent Mergers & Acquisitions

- Disease Overviews and Demographic Information

- Company Profiles, Product Portfolios and SWOT for Top Competitors

Market Value and Industry Trends

The BPH treatment market, and the stone management device market, accounted for the majority of the total market value in 2019. The growth in these two segments is driven by the stable demand for related procedures, the growing prevalence of prostatic and kidney diseases, and the premium prices for lasers and lithotripters.

The stable growth across the market is driven by the continuing adoption of new technologies, focused on the largest and the growing areas of the market. The UroLift® market has experienced rapid growth since its launch in Australia in 2012 and its reimbursement coverage in 2013.

The female urinary incontinence market, which represented nearly one-third of the combined incontinence management device market, is undergoing structural changes, due to regulatory and reimbursement changes regarding transvaginal tape and mini-slings. Both devices are currently banned in Australia.

Competitive Analysis

By 2020, the leading competitor in the Australian urological device market was Boston Scientific. The company held the leading positions in the pelvic organ prolapse repair market, stone management device market, and BPH treatment device market. The company’s leading position is attributed to its established products, including men’s health and prostate health businesses. The acquisition of NxThera and its Rezūm® system in 2018 provided Boston Scientific’s sole presence in the emerging Rezūm® market in Australia.

By 2020, the leading competitor in the Australian urological device market was Boston Scientific. The company held the leading positions in the pelvic organ prolapse repair market, stone management device market, and BPH treatment device market. The company’s leading position is attributed to its established products, including men’s health and prostate health businesses. The acquisition of NxThera and its Rezūm® system in 2018 provided Boston Scientific’s sole presence in the emerging Rezūm® market in Australia.

Coloplast was the second-leading competitor in the urology market in Australia. This was attributed to the company’s leading share in the urinary incontinence market, primarily driven by the catheter segment, as well as its notable share of pelvic organ prolapse repair and its leading share in erectile dysfunction treatment.

Olympus was the third-leading competitor in the Australian urological device market by 2020. This was attributed to its second-leading position in the BPH treatment market and a notable presence in the stone management device market. Olympus operates a urology/gynecology business unit (UGBU), the growth of which is supported by the company’s strength in the gastrointestinal business and in surgical device technologies.

Segments Covered

Click on each title to view detailed market segmentation.

- Procedure Volumes for Urological Devices – MedPro – The complete procedural analysis of the urological device market in Australia, which includes Incontinence Sling Implantation, Artificial Urinary Sphincter Implantation, Urethral Bulking, Transvaginal Tape Incontinence Sling, Transobturator Incontinence Sling, Single-Incision Incontinence Sling, and many other procedures for each of the market segments.

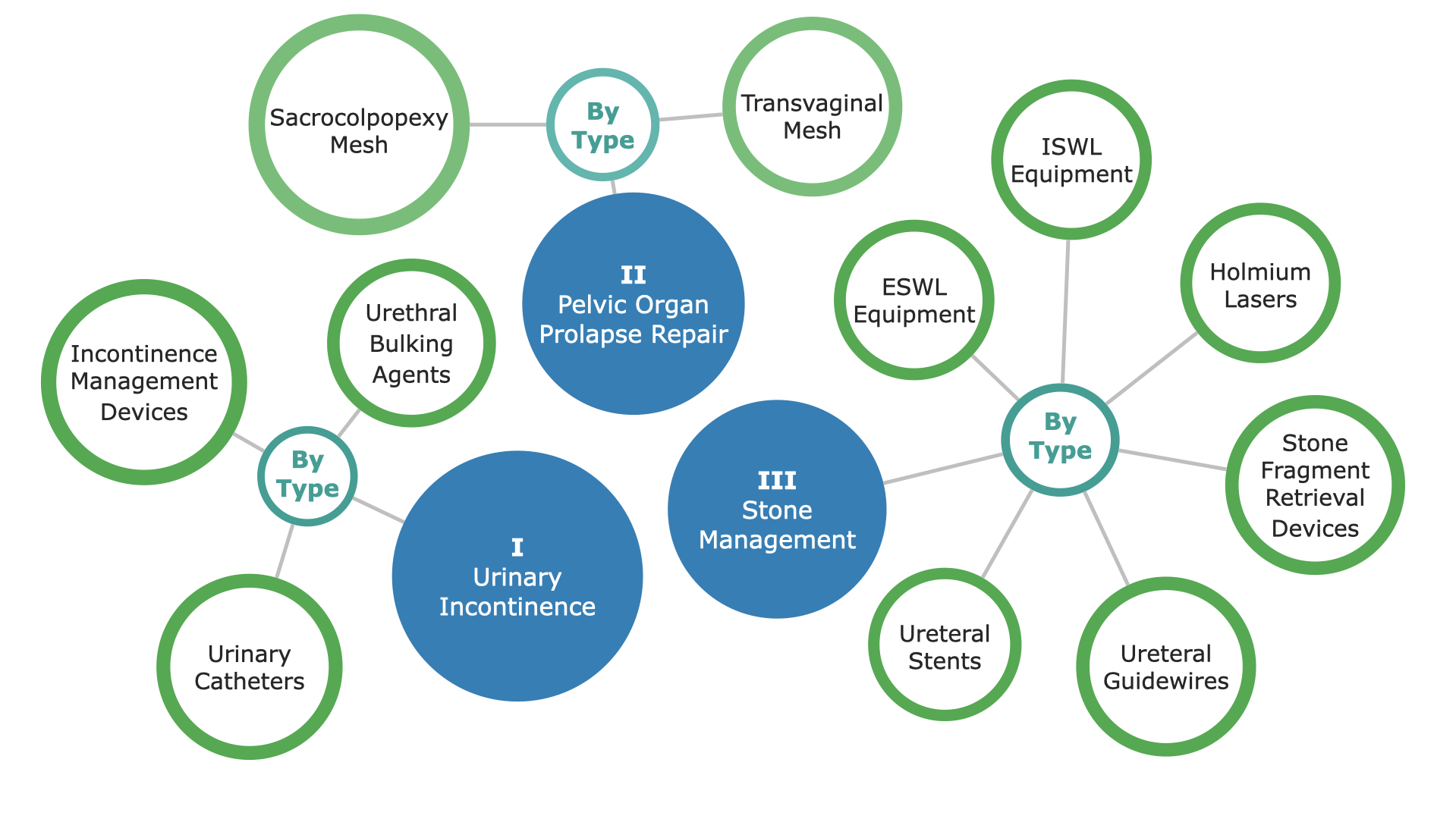

- Urinary Incontinence Market – MedCore – This market is further segmented into market segments, such as Urinary Catheters, Urethral Bulking Agents, and Incontinence Management Devices.

- Pelvic Organ Prolapse Repair Market – MedCore – The market is comprised of the segments for Transvaginal and Sacrocolpopexy Meshes.

- Stone Management Market – MedCore – This market is categorized by Device Type into ESWL Equipment, ISWL Equipment, Holmium Lasers, Stone Fragment Retrieval Device, Ureteral Stent, and Ureteral Guidewire market segments.

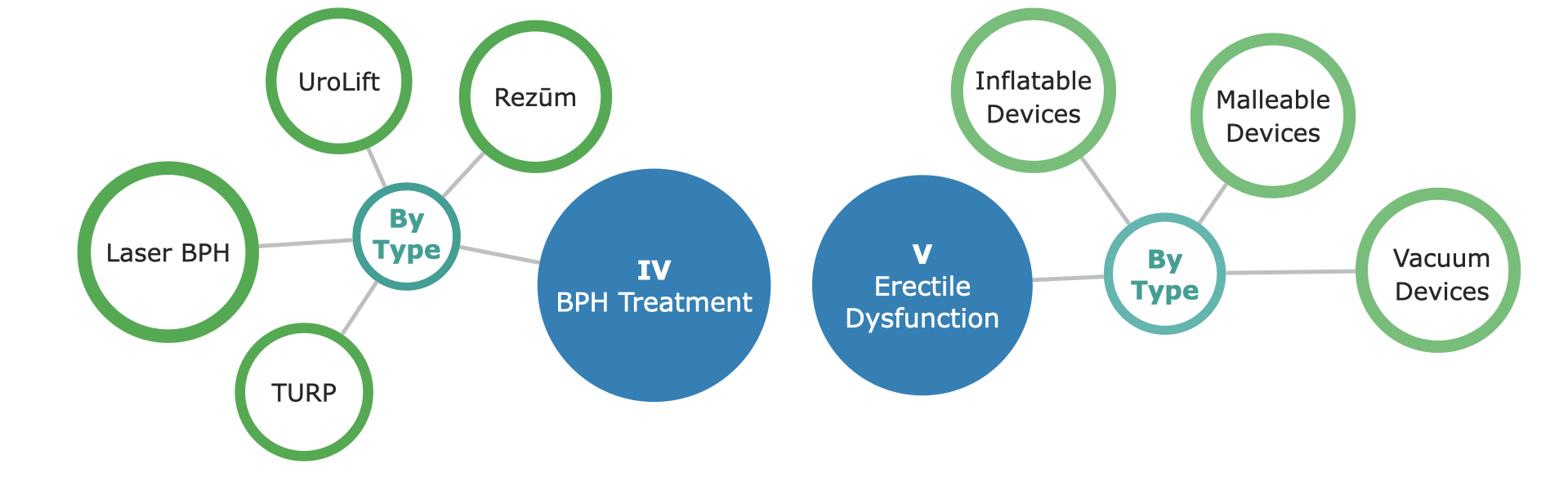

- Benign Prostatic Hyperplasia (BPH) Treatment Market – MedCore – This market is segmented by Device Type, including Transurethral Resection of Prostate, Laser BPH, UroLift, and Rezūm device market segments.

- Erectile Dysfunction Market – MedCore – The market is comprised of the segments for Inflatable, Malleable and Vacuum devices.

Detailed Market Segmentation

DON’T SEE THE SEGMENT OR DATA YOU NEED?

Feel free to contact us or send a request by pressing one of the buttons below.