Product Description

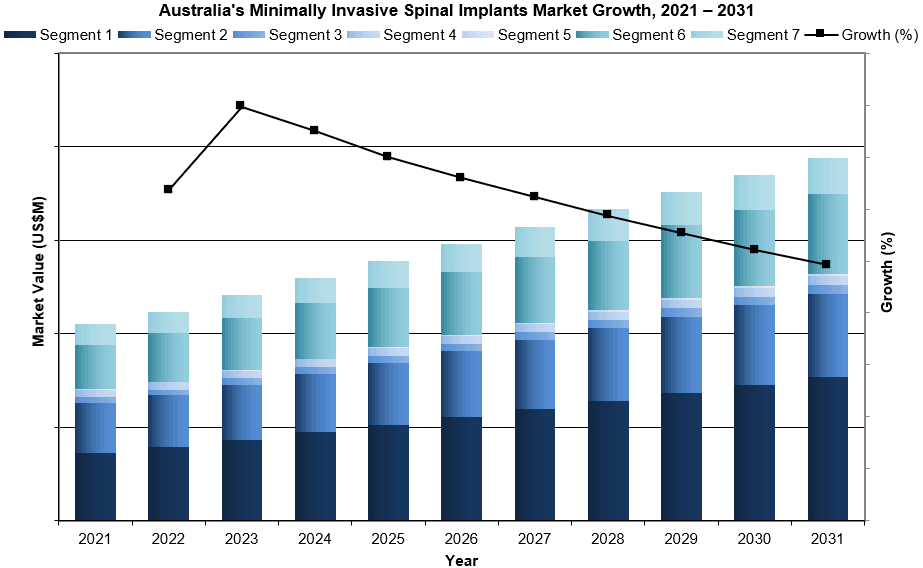

The Australian MIS implant market was valued at nearly $130 million in 2024. This is expected to increase over the forecast period at a CAGR of 5.9% to reach $194 million in 2031.

The 2025 report on the Australian market for minimally invasive spinal (MIS) implants provides a comprehensive analysis of the sector, including segments such as MIS interbody (IB) devices, MIS pedicle screws, spinous process fixation, facet fixation, SI joint devices, spine endoscopes, and MIS surgical instrumentation. Emerging trends and technological advancements in each category are explored.

MARKET REPORT DATA TYPES INCLUDED

- Unit Sales, Average Selling Prices, Market Value & Growth Trends

- Procedure Numbers

- Forecasts Until 2031, and Historical Data to 2021

- Market Drivers & Limiters for Each Segment

- Competitive Analysis with Market Shares for Each Segment

- Recent Mergers & Acquisitions

- Company Profiles and Product Portfolios

- Leading Competitors

AUSTRALIA’S MINIMALLY INVASIVE SPINAL PLANT MARKET TRENDS

Patient preference for minimally invasive procedures remains a key driver in the Australian MIS market. MIS procedures are increasingly favored due to their ability to minimize muscle and tissue damage, reduce complication rates and shorten recovery periods. These factors continue to attract patients who are increasingly well informed and seeking alternatives to traditional open surgeries. Recent developments in robotic-assisted MIS technologies and AI-guided surgical planning in 2024 have further cemented the popularity of MIS techniques, offering greater precision and improving clinical outcomes.

AUSTRALIA’S MINIMALLY INVASIVE SPINAL IMPLANT MARKET SHARE INSIGHTS

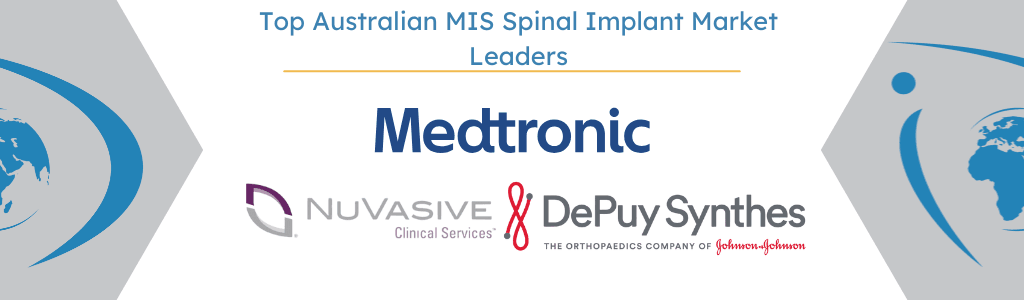

- Medtronic was the leading competitor in the overall MIS market in 2024. The company was the leading competitor in the pedicle screw market, the second-leading competitor in the facet fixation and MIS interbody device markets and a major competitor in the spinous process and MIS sacroiliac joint fusion markets.

- Globus Medical/NuVasive was the second-leading competitor in the overall MIS market in 2024. The company merged in 2023, and the combined entity has gained market share globally. The combined entity is the leading competitor in the MIS interbody device market. Globus Medical/NuVasive also had large shares in the MIS pedicle screw, spinous process, facet fixation and MIS sacroiliac joint fusion markets.

- DePuy Synthes was the third-leading competitor in 2024. DePuy Synthes led the facet fixation market, but the company’s overall share is due to major shares in the MIS interbody device and MIS pedicle screw markets.

MARKET SEGMENTATION SUMMARY

- MIS Interbody Device Market – Further Segmented Into:

- Device Type: Minimally Invasive Posterior Lumbar Interbody Fusion (MIPLIF), Minimally Invasive Transforaminal Lumbar Interbody Fusion (MITLIF), Lateral Lumbar Interbody Fusion (LLIF), and Oblique Lumbar Interbody Fusions (OLIF).

- MIS Pedicle Screw Market – Further Segmented Into:

- Device Type: Percutaneous Cannulated, Retractor Cannulated, and Retractor Non-Cannulated.

- Spinous Process Fixation Market

- Facet Fixation Market

- MIS SI Joint Fusion Market

- Spine Endoscope Market

Research Scope Summary

| Report Attribute | Details |

|---|---|

| Regions | Australia |

| Base Year | 2024 |

| Forecast | 2025-2031 |

| Historical Data | 2021-2023 |

| Quantitative Coverage | Procedure Numbers, Market Size, Market Shares, Market Forecasts, Market Growth Rates, Units Sold, and Average Selling Prices. |

| Qualitative Coverage | Market Growth Trends, Market Limiters, Competitive Analysis & SWOT for Top Competitors, Mergers & Acquisitions, Company Profiles, Product Portfolios, FDA Recalls, Disruptive Technologies, Disease Overviews. |

| Data Sources | Primary Interviews with Industry Leaders, Government Physician Data, Regulatory Data, Hospital Private Data, Import & Export Data, iData Research Internal Database. |