Product Description

Industry Trends

One impactful factor limiting growth of the implant-supported overdentures market was the ongoing improvement of dental health in the United States. Better dental health will equate to more partially, rather than fully, edentulous patients. As such, partial restorations will grow at the expense of full arch overdenture products, which are the focus of this report.

The overdentures market will be driven by patient awareness and favorable demographic factors throughout the forecast period. As national organizations and manufacturers consolidate the market, pushing out smaller competitors, their marketing efforts will improve patient education and awareness. Individuals with poor dental health are retiring or reaching old age with more

discretionary income and knowledge of the various restoration options available.

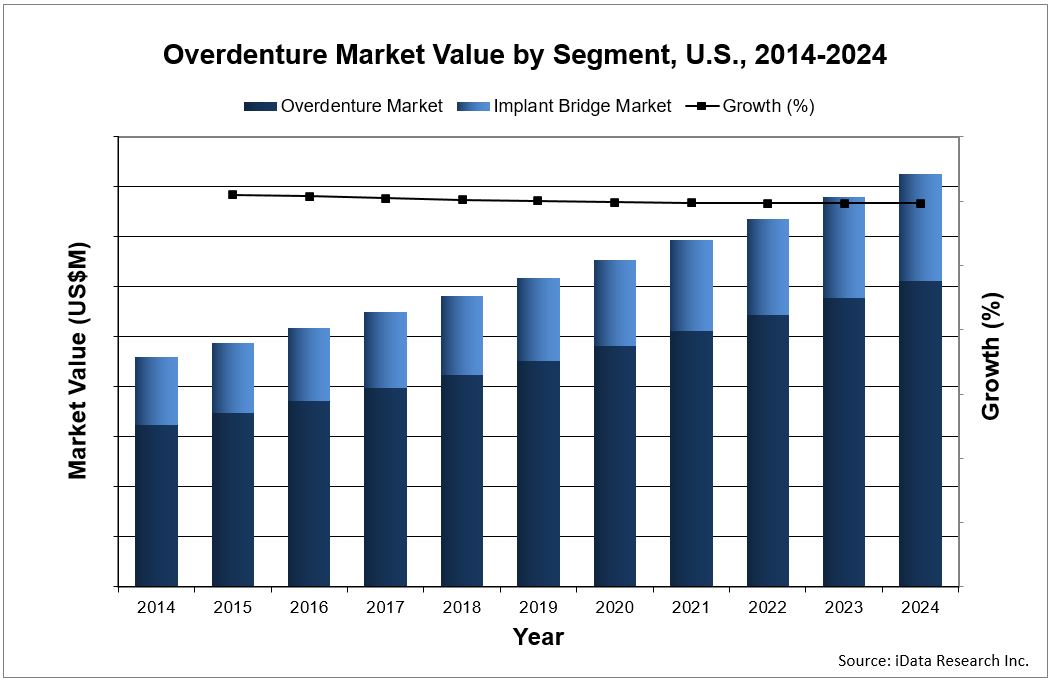

Overall the overdenture market is expected to reach $826 million by 2024 in the United States, and $1.2 billion in Europe.

Report Regional Coverage

Throughout this research series, iData has covered several countries in great detail. Each country may be purchased as a stand-alone report, tailoring the data to your needs. The covered countries are:

- United States

- Europe (15 countries including: Germany, France, U.K., Italy, Spain, Benelux (Belgium, Netherlands and Luxembourg), Scandinavia (Denmark, Finland, Norway and Sweden) Austria, Switzerland and Portugal)

The Only Medical Device Market Research With: |

||||

|---|---|---|---|---|

| ✔ Unit Sales Growth Analysis ✔ Average Selling Prices ✔ Competitor Shares by Segment & Country ✔ Interview-Based Research Methods ✔ The Lowest Acquisition Cost |

||||

Highly Detailed Segmentation

While this report suite contains all market data, each of the market segments are also available as stand alone MedCore reports. This allows you to get access to only the market research that you need. You can view all these included reports and segmentation here:

- Product Portfolio for Dental Overdentures – MedFolio

- Dental Overdenture Market – MedCore

- Implant Bar Market – MedCore

- Attachment Market – MedCore

- Implant Bridge Market – MedCore

Buying all of these reports together in this suite package will provide you with substantial discounts from the separate prices. Request Pricing to Learn More

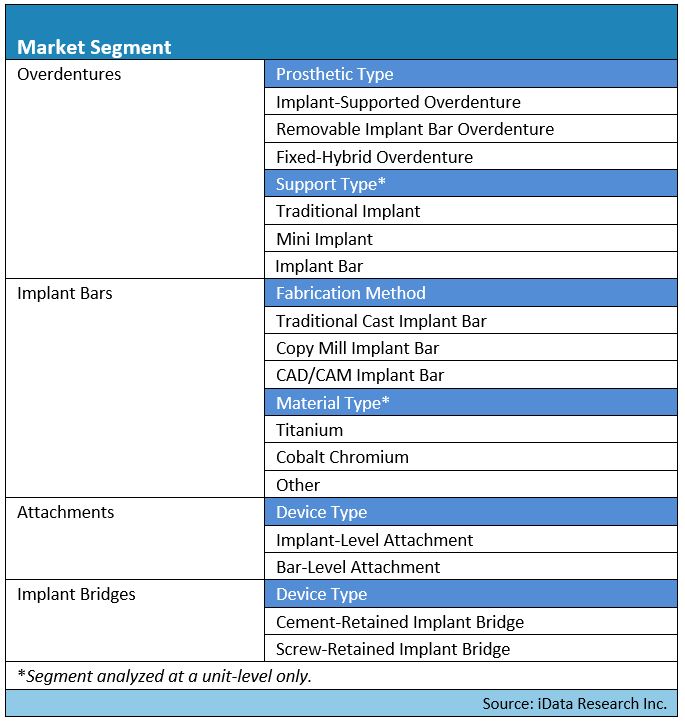

Full Segmentation Map for the United States

Data Types Included

- Unit Sales, Average Selling Prices, Market Value & Growth Trends

- Forecasts Until 2024, and Historical Data to 2014

- Market Drivers & Limiters for Each Overdenture and Implant Bridge Segment

- Competitive Analysis with Market Shares for Each Segment

- Recent Mergers & Acquisitions

- Disease Overviews and Demographic Information

- Company Profiles, Product Portfolios and SWOT for Top Competitors

- Related Press Releases from Top Competitors

Overdenture Market Share Insights

The United States overdenture market is dominated by dental laboratories and CAD/CAM milling facilities, making up more than half the market. These laboratories produced the majority of traditional cast implant bars in the United States. However, as mentioned previously, dental laboratories are rapidly switching to CAD/CAM technology to fabricate their restorations. The increasing affordability of CAD/CAM systems has allowed laboratories to compete with the milling capabilities of CAD/CAM manufacturers. As a result, laboratories will continue to hold a significant share of the implant bridge and bar markets over the forecast period.

This trend is even more prominent in Europe, where Labs and milling facilities consume an even greater share of the market.

The leading company in these markets is Locator (manufactured by Zest Anchors), followed by O-Ring in the U.S., and Dalbo in Europe. Locator® attachments are compatible with more than 350 different implant products, spanning over 70 manufacturers. These attachments offer a pivoting and self-aligning design with greater resiliency and a maximum implant divergence of 40 degrees. With a total attachment height of 3.17 mm for an externally hexed implant, the Locator® attachment offers the lowest vertical height available in the market. Nylon male pieces are available in three different colors, each one offering a different level of retention.

Throughout this series of reports, iData’s analysts have studied over 50 companies closely. For a full list of companies mentioned in this series of research see the table below.

All Companies Analyzed in this Study |

||||

|---|---|---|---|---|

|

|

|||

Latest Developments in this Market

February 2018 – BC Partners to acquire Zest Dental Solutions from Avista Capital Partners

February 2018 – EnvisionTEC and AvaDent enter partnership for digital denture solution

February 2018 – EnvisionTEC launches new printer Vida cDLM and new materials